Five Key Things We Learned at Xi’s Annual Policy Summit

China’s annual gathering of leaders in Beijing ended Friday after eleven days of meetings.

(Bloomberg) -- China’s annual gathering of leaders in Beijing ended Friday after eleven days of meetings that unveiled a lower annual growth target, sweeping tax cuts, and a new foreign investment law.

There also were new insights on the government’s strategy to rein in debt, its efforts to funnel more credit to private companies and improve the business environment, and the trade negotiations with the U.S. There were even some rare comments on the Xinjiang region’s controversial mass detention camps.

“Maintaining overall stability seems to have become the paramount objective,” said Chen Xingdong, chief China economist at BNP Paribas SA in Beijing. “Policymakers seem to feel that implementing the China-U.S. trade deal will create pressure.”

Here are five takeaways:

The Economy

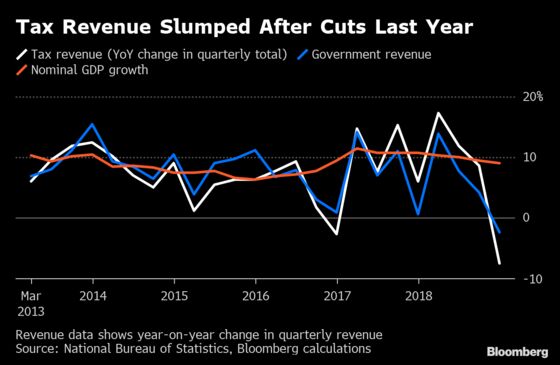

The message on the economy was clear: China won’t resort to debt-fueled stimulus, is doubling down on efforts to get more credit to efficient private companies, and is striving to improve the business environment for them and foreign companies. It lowered the annual growth target to 6 to 6.5 percent from about 6 percent last year, creating the wiggle room to shift away from credit-fueled expansion while avoiding past credit blowouts.

The almost 2 trillion yuan of tax cuts announced is unprecedented and Finance Minister Liu Kun said the actual amount may be higher. To help pay for it while raising the budget deficit target only 0.2 percentage point to 2.8 percent of gross domestic product, Premier Li Keqiang said at his annual press conference Friday that the “blade of the knife” will be turned on the government itself. About 1 trillion yuan will be utilized from the profits of central state enterprises and financial institutions as well as by mobilizing existing idle funds, Li said.

“The lowering of the growth target reflects that policymakers have come to accept the reality of lower growth in exchange for long-term sustainability,” said Michelle Lam, a greater China economist at Societe Generale SA in Hong Kong.

Hidden Debt

The campaign to rein in leverage is shifting to so-called hidden debt, referring to off-balance-sheet loans or borrowings of local government entities. Across the country, provinces and cities are looking for ways to reduce their implicit borrowings. Some are seeking cheap refinancing from the nation’s largest policy lender, the China Development Bank, and others are selling off state-owned assets such as office buildings and housing.

Hidden debt in some places exceeds the on-book borrowing, said Zhu Mingchun, a lawmaker of the National People’s Congress, without naming places directly. Payments due for local-government financing vehicle debt, just part of the off-book borrowing, could reach 2.3 trillion yuan this year, according to estimates by Industrial Securities Co. in Hong Kong. The fact that there is no official estimate of the size of the implicit debt, which usually carries higher rates than on-book ones, makes the issue even trickier. S&P Global Inc. estimated in October that hidden debt totals about 40 trillion yuan.

“The problem can’t be delayed anymore,” as in many places fiscal revenues and gross domestic product aren’t enough to cover the interest and principal, said Lu Ting, chief China economist at Nomura Holdings Inc.

Foreign Investment Law

The passage of a new foreign investment law Friday allows, on paper at least, for all companies registered in China to compete on equal terms from Jan 1, 2020. Forced technology transfers are banned, applications for operating licenses will be treated equally, and government support will apply equally to foreign firms. All are controversial issues that helped trigger the trade war with the U.S.

While Societe Generale SA says the new law, passed with unusual speed, is symbolically important and marks a further opening up step, foreign companies complain that China has for years been long on promises and short on their delivery. They’ll wait to see if the law will be forcefully executed.

“Implementation and enforcement has long been the missing ingredient in China,” said Katrina Ell, an economist with Moody’s Analytics in Sydney. “Enforcement is critical for it to be effective.”

Trade Talks

It wasn’t on the agenda but there was no way the ongoing trade negotiations with the U.S. could be ignored. China kept its cards close to its chest while pushing back a tad against U.S. demands, notably when vice commerce minister Wang Shouwen said any mechanism to enforce an agreement must be two-way. That “suggests difficulties in how to word the implementation mechanism,” said BNP Paribas’ Chen. Former finance minister Lou Jiwei was more blunt, saying China won’t make big concessions and that some U.S. demands are “just nitpicking.”

Xinjiang

The meeting created a rare opportunity for officials to respond to international criticism about the Xinjiang region’s notorious mass detention camps. They were unequivocal. The Muslim region will maintain them for a “long time,” said government chief Shohrat Zakir, at a meeting packed with reporters, reflecting the intense scrutiny on the region.

An ethnic Uighur, Zakir disputed the term “re-education centers,” likening the camps instead to vocational training centers that are similar to boarding schools. “The fight against instability, extremism and secessionism is long, complex and intense,” Zakir told a public question session. “We can’t relax for a moment at any time.”

To contact Bloomberg News staff for this story: Kevin Hamlin in Beijing at khamlin@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, Sharon Chen

©2019 Bloomberg L.P.

With assistance from Bloomberg