Chinese Borrowers Face Fresh Tests as Debt Reprieve Nears End

Chinese Borrowers Face Fresh Tests as Debt Reprieve Nears End

(Bloomberg) -- Chinese firms that delayed debt payments during the coronavirus crisis are about to get the check.

At least 10 companies will face fresh repayment tests on a combined 10.68 billion yuan ($1.5 billion) of bonds over the next two quarters or so, after they postponed maturities or swapped old debt for new notes to alleviate immediate pressure earlier this year.

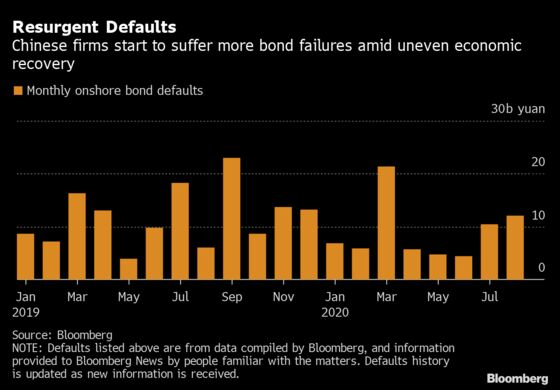

Beijing endorsed the use of such a reprieve by borrowers during the peak of the virus outbreak so as to maintain financial stability. But following a slowdown in the spring, bond defaults in China have started re-accelerating since July amid a surge in borrowing costs. Adding to the signs of stress, more have recently joined the group of companies seeking repayment delays.

“These tactics are merely optics and the companies are in reality in default, and we adjust our default data to include such extensions for both onshore and offshore bond issuers,” said Owen Gallimore, head of credit strategy at Australia & New Zealand Banking Group Ltd.

Signs of trouble are already emerging for some of these borrowers as they are unable to benefit from a still uneven economic recovery.

Beijing Sound Environmental Engineering Co., a waste management firm, failed in June to make partial principal payment on a bond issued in March to swap for an old note. Haikou Meilan International Airport Co., an affiliate of troubled conglomerate HNA Group, earlier this month revealed repayment uncertainties over a 1 billion yuan bond even after extending its maturity by 270 days to Sept. 9.

Unlike in developed debt markets, corporate bonds in China are actually more like a variation of bank loans, and maturity extensions stem from similar practices among Chinese commercial lenders, said Chen Su, a bond portfolio manager at Qingdao Rural Commercial Bank Co. Chinese banks, a major force of investors in corporate notes, often agree to receive interests first and delay principal payment by one year or so to cut the size of bad loans, he said.

| Read more: |

|---|

| Chinese Bond Defaults Swell in Sign of Enduring Economic Pain |

| China’s Growing Dollar Bond Defaults Reveal Depth of Stress |

| China Creditor Squeeze Prompts Drop in Record Bond Defaults |

| China Firms’ Bond Payment Plans Signal Shift In Policy Focus |

Among the companies facing renewed pressure is Shandong Ruyi Technology Group Co., a debt-saddled luxury clothing maker that once aspired to be China’s LVMH. After twice extending coupon payment on a 1 billion yuan bond from the original due date in mid March, it will need to deliver again in December.

In an ominous signal, the borrower is asking investors not to sell back early a 1.5 billion yuan bond via a put option scheduled next month, Bloomberg reported Thursday, according to people familiar with the matter.

The private garment maker is one of at least four companies that have recently sought to extend repayment deadlines in one way or another. They also include two firms under the umbrella of HNA Group and a cash-strapped media company.

“When investors of bonds issued by private firms encounter non-conventional situations including bond swaps, they may face relatively big uncertainties and default risk,” said Samuel Wong, Shanghai-based fixed-income fund manager at Neuberger Berman Investment Management. “This is because the possibility for such borrowers to secure refinancing is close to zero.”

©2020 Bloomberg L.P.

With assistance from Bloomberg