(Bloomberg Opinion) -- There’s been much discussion lately over whether global markets have reached some sort of inflection point, with stocks tumbling and bond yields settling into a new, higher range. There’s still seven trading days left in October, but already this month is the worst for global equity markets since January 2016, with the MSCI All Country World Index dropping 6 percent. Monday’s action should only stoke the debate.

Here’s why: China’s Shanghai Composite Index surged 4.1 percent, its biggest gain since March 2016, as President Xi Jinping vowed “unwavering” support for non-state firms and the government released a plan to cut personal income taxes. Good news, for sure, but what’s odd is that such moves like that in China’s stock market in the past would have triggered a global rally in equities. Not this time, however. The MSCI All-Country World Index fell as European equities declined and major U.S. indexes were mostly flat to lower. The response suggests that investors view China’s efforts at shoring up its slowing economy and faltering stocks, which recently entered a bear market, more like an act of desperation than one that comes from a position of strength as the nation seeks to respond to the Trump administration’s escalating tariffs in a trade war that no one is likely to win. Weak industrial output and what the government called the “severe international situation” were key factors behind the third-quarter slowdown in China’s economy, with domestic product growth slowing to 6.5 percent from a year earlier, from 6.7 percent during the previous three months. “China is under pressure on multiple fronts,” Michael Every, head of Asia financial markets research at Rabobank in Hong Kong, told Bloomberg News. “Logically, all this pushes China to make a deal, yet I don’t think there is a deal to be had.”

There’s plenty besides a U.S.-China trade war for investors to worry about, not the least of which is a general sense that major central banks no longer have the desire to prop up financial markets with extraordinarily accommodative monetary policies. Consider that the collective balance-sheet assets of the Federal Reserve, European Central Bank, Bank of Japan and Bank of England, which grew steadily to 37.2 percent of their countries’ total GDP at the end of 2017 from less than 20 percent in 2011, have shrunk to 36.6 percent this year, data compiled by Bloomberg show.

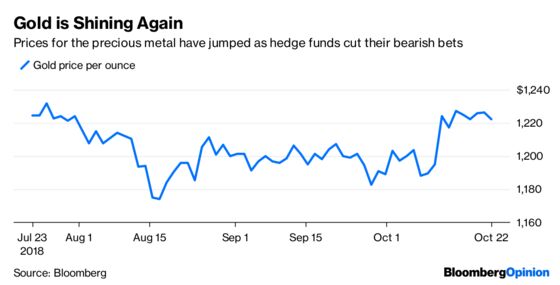

GOLD IS PRECIOUS AGAIN

It’s also notable that gold is starting to generate some interest again, which is almost never a good sign for markets. Hedge funds and other large speculators have cut their bearish bets on one of the market’s most well-known haven assets by the most since March, an indication that the precious metal is on the mend after prices fell for six straight months, according to Bloomberg News’s Susanne Barton. The short position in bullion futures and options slid by about 24 percent in the week ended Oct. 16, U.S. government data released Friday showed. “We’ve seen some capitulation by bears,” said Tai Wong, the head of base and precious metals trading at BMO Capital Markets. “The price action over the past week has significantly wounded them. We have more potential on the upside.” At the same time, Bank of America Merrill Lynch strategists are backing bullish options linked to the precious metal. A negative view on the dollar, large short positions in gold futures and investor demand for portfolio protection are some of the reasons behind the call, investment strategists including James Barty wrote in a note on Friday, reports Bloomberg News’s Cormac Mullen. “The current environment is one where the precious metal is regaining its prominence as a portfolio hedge and has value now,” the strategist wrote. “The market is currently very short gold futures and the likelihood of a relatively less hawkish Fed into year end and 2019” can boost the value of gold.

HIGHER BOND YIELDS ARE STICKING

Bonds have also turned into a warning sign for risk assets such as equities. What’s worrying is that despite evidence that the global economy may be slowing, trade wars are only getting worse and political risks in places such as Italy are intensifying, yields on benchmark 10-year Treasuries haven’t retreated. After rising from about 2.80 percent in late August to as high as 3.26 percent earlier this month, yields have settled around the 3.20 percent level. To many market participants who have become accustomed to yields comfortably below 3 percent in recent years, the move means that they must now reprice all risk assets off this higher, risk-free rate. That inevitably makes those risk assets such as stocks worth much less. A Bloomberg News survey this month of more than 50 economists and strategists found that the yield is likely to keep rising, reaching 3.30 percent by the end of the first quarter and about 3.50 percent by this time in 2019. Rising yields aren’t just a U.S. phenomenon. Yields as measured by the Bloomberg Barclays Global Aggregate Bond Index have jumped to 2.25 percent, the highest since 2013, amid signs that inflation is a bigger risk facing bond investors than disinflation. Core inflation in the so-called G-3 economies — the U.S., euro zone and Japan — has risen to a 1.4 percent annual pace from a post-crisis low of 1.1 percent, and is bound to float higher, according to a research note by Chetan Ahya, Morgan Stanley’s chief economist and global head of economics. The euro area and Japan should see a more “pronounced uptick” than the U.S., reports Bloomberg News’s Michelle Jamrisko, citing Ahya.

EM PROFIT ESTIMATES RISE

One area for optimism is in emerging markets, which did respond positively to the stimulus efforts in China. MSCI Emerging Markets Index of equities jumped as much as 1.33 percent Monday. For the first time since April, emerging-market earnings estimates have started to edge higher, according to the strategists at Bloomberg Intelligence. Earnings per share estimates for the MSCI Emerging Markets Index are 1.6 percent above the September low, led by accelerating expectations for commodity-sensitive Russia and Brazil. While forecasts for earnings in Turkey and China remain under pressure, Mexico’s have been on the rise since their June low, according to BI. There’s a “great opportunity” to buy emerging-market stocks, Kate Moore, the chief equity strategist at BlackRock Inc., said on Bloomberg TV Monday. Much of the weakness in emerging-market equities this year that was tied to negative sentiment over trade and policies is largely over, according to Moore. “We’re not actually seeing (those concerns) come through as far as their earnings or demand,” Moore said. At just under 12 times earnings, the more than 1,100 companies that make up the MSCI Emerging Markets Index trade at their lowest average multiple since 2015, according to data compiled by Bloomberg. As recently as January, the average price-earnings multiple was close to 17, just before the index began a long slide that saw it fall 23 percent from its peak that month through Monday.

INVESTORS FLEE SAUDI IN DROVES

The pressure on Saudi Arabia from the killing of journalist Jamal Khashoggi is getting stronger by the day — and not by other governments. Investors can’t get their money out of Saudi Arabia fast enough. Foreigners were net sellers of a total of 4 billion riyals ($1.1 billion) of stocks last week, more than any other since data was first made available in 2015, with the exception of a one-time outflow from a single transaction in September 2017, according to Bloomberg News’s Filipe Pacheco. Most of the sales came from qualified foreign institutional investors, which were first authorized to trade directly in the market three years ago. Local retail investors were also net sellers for the week, while Saudi institutions were net purchasers. The crisis comes as the kingdom’s market regulator and its stock exchange, known as Tadawul, proceed with reforms aimed at aligning the market with international standards as part of a broader plan to diversify the economy. “The record amount of the sell-off really shows the gravity of the situation,” said Naeem Aslam, chief market analyst at Think Markets UK in London. “The Saudis have suffered a major setback, and it is going to take a very long time and hard work for them to gain the same kind of confidence.” The Tadawul All Share Index has dropped 4.4 percent this month despite speculation that funds tied to the government could be propping up shares, a suggestion that hasn’t been confirmed.

TEA LEAVES

Many market participants say hawkish central banks are a big reason behind the weakness in equities and other risk assets. If you believe that, then this week shouldn’t offer any relief. The Bank of Canada is widely expected to raise its benchmark interest rate by 25 basis points to 1.75 percent on Wednesday. Tight labor market conditions and the recent trilateral trade agreement with the U.S. and Mexico give the central bank some cover as it moves to address firming inflationary pressures, according to Bloomberg Economics. Although Sweden’s Riksbank is poised to hold rates at minus 0.5 percent when policy makers meet, they strongly hint that they are close to raising rates for the first time in seven years. The European Central Bank meets on Thursday, and while it’s also not forecast to increase rates, it will likely reiterate that asset purchases are set to conclude as planned this year.

DON’T MISS

Emerging Markets Need Fixes to Stay Calm: Mohamed A. El-Erian

Netflix Can’t and Won’t Stop Selling Junk Bonds: Brian Chappatta

Only Bond Investors Can Put the Boot Into Italy: Marcus Ashworth

China’s National Team Is Saving the Wrong Targets: Shuli Ren

Democrats’ Attack on Tax Cuts Misses the Point: Stephanie Kelton

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.