China's High-Yield Bond Market Has Ballooned to $159 Billion

China's High-Yield Bond Market Has Ballooned to $159 Billion

(Bloomberg) --

China’s credit investors are demanding to be paid for risk - and that’s leading to explosive growth in the nation’s high-yield bond market.

There are about 1.1 trillion yuan ($159 billion) of local company bonds outstanding that offer investors more than 8%, the local cutoff for what’s considered high-yield, according to AJ Securities Co. By late last year, the market was seven times larger than it was at the start of 2015, Guosen Securities Co. data show.

A record wave of company defaults is forcing asset managers to spend more time doing due diligence on issuers, and account for those risks in bond-market pricing. As China’s pile of high-yield debt grows, it’s drawing a new breed of investors who had previously focused on other risky investments, such as non-performing loans.

“China’s high-yield bond market is deepening this year as the pace of credit default continues and as institutional investors’ pricing power grows,” said Zhao Xue, head of fixed income department at Shanxi Securities Co.

Lakeshore Capital Co., a Chinese special situations asset manager which has favored NPLs, plans a $1 billion fund this year to invest in high-yield bonds of private sector firms. DCL Investments, a Chinese distressed asset fund, has started screening junk bonds for potential purchases.

A manager who oversees 1 billion yuan of junk bonds at a large Chinese private fund said the company won its first mandate from foreign investors this year to invest in high-yield debt. The fund manager asked not to be named as they’re not authorized to talk to media.

Shanxi Securities’ Zhao said some good investment opportunities emerged in China’s high-yield bond market last year, including one where some investors reaped fat returns from price volatility of a listed private firm, whose large cash holdings came under criticism.

More Active

“Private funds are still the main players,” said Zhang Yihan, deputy chief of financial market department at AJ Securities. “Yet we are seeing large securities houses and bad asset managers getting more active in this market.” The broker launched the first onshore high-yield bond index with China Central Depository & Clearing Co. in September.

Developing risk pricing is a priority for Chinese officials, who want capital to flow to promising firms while avoiding unsustainable debt pile-ups at struggling companies. It’s all part of reforms that also involve opening up the $13 trillion bond market to foreign money, and shutting down some of the shadow-financing channels that make borrowing more opaque.

Read: China Regulators Take Steps to Boost Trading of Defaulted Bonds

Regulators took a fresh step last week to encourage trading of defaulted bonds. When companies miss a principal payment, those securities will now be allowed to trade on the fixed-income trading platform of the Shanghai and Shenzhen exchanges for the first time. Guosheng Securities Co. expects the move to boost liquidity and enhance price discovery.

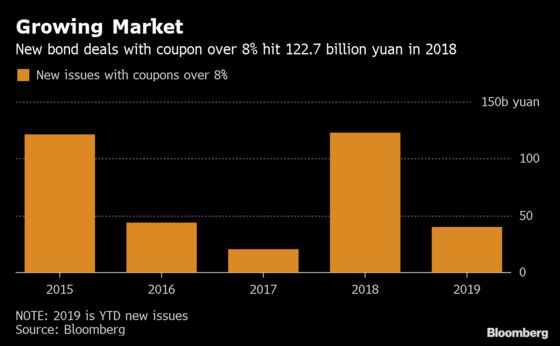

New onshore bond defaults have reached 40.3 billion yuan so far in 2019, about three times the tally in the year-earlier period, Bloomberg-compiled data show. In the primary market, some 39.7 billion yuan of securities have been sold in 2019 with coupons exceeding 8%. That followed 122.7 billion yuan last year, the highest total in four years.

Different Strategies

Lakeshore will focus on private sector firm issuers that are operating as normal but face temporary liquidity difficulties and are willing to provide assets as collateral for refinancing, according to chairman Zhang Zheng.

DCL Investments has a similar focus as Lakeshore but it will look for opportunities to buy distressed bonds, along with non-performing loans and equity stakes, in order to restructure companies, said Zheng Hualing, president of DCL Investments.

AJ Securities’ Zhang said she focuses on an event-driven strategy that seeks to take advantage of mispricing in the secondary market.

“Some good companies may be hit hard by negative factors such as industry swings, resulting in a sell-off in their bonds that can provide an investment opportunity,” she said.

--With assistance from Yuling Yang.

To contact Bloomberg News staff for this story: Ina Zhou in Hong Kong at hzhou179@bloomberg.net;Xize Kang in Beijing at xkang7@bloomberg.net;Tongjian Dong in Shanghai at tdong28@bloomberg.net;Molly Dai in Singapore at bdai13@bloomberg.net;Qingqi She in Shanghai at qshe@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Chan Tien Hin

©2019 Bloomberg L.P.

With assistance from Bloomberg