China’s Feud With Bondholders Could Reset Debt Workout Rules

China’s Feud With Bondholders Could Reset Debt Workout Rules

(Bloomberg) -- The last time Zambia renegotiated its external debt, the well-oiled machine established by institutional lenders and western governments handled it with little trouble.

But 15 years later, with the southern African nation in the throes of a $12 billion debt overhaul, China and bondholders have emerged as powerful new players to upend the choreography.

Beijing is embroiled in a feud with money managers in New York and London, putting the impoverished nation in the middle. The outcome of the dispute over the billions Zambia borrowed from both sides could define how developing countries address debt crises from now on.

“The precedent set in Zambia is likely to be the one that everyone points to in the next couple of years as we have multiple sovereign debt workouts,” said Lee Buchheit, one of the world’s most prominent debt-restructuring lawyers. “This is the beginning of a new era.”

Mutual Suspicion

Ethiopia, Kenya and the Republic of Congo are among fiscally challenged African nations with high levels of Chinese debt. But with the coronavirus pandemic punishing economies around the world, the problem is wider than just Africa: the Maldives, Kyrgyz Republic and Venezuela are among the largest recipients of largesse from the world’s newest financial powerhouse, according to a study co-authored by the World Bank’s chief economist, Carmen Reinhart.

At the heart of the battle in Zambia is the suspicion from both sides that any relief granted to one would be used to repay the other. The players don’t trust each other and are barely on speaking terms. Bondholders delayed a key vote on Tuesday to defer coupon payments, with the next meeting set for Nov. 13.

In previous debt crises of the 1980s and 1990s, rich western governments grouped in the so-called Paris Club and commercial banks mostly from the same countries worked together to write off loans in exchange for budget cuts and promises to curb corruption. That world has changed dramatically.

China has become the world’s largest non-commercial lender, surpassing the International Monetary Fund and World Bank. In the past two decades, financing roads, airports and hospitals across Africa, Asia and Latin America has driven China’s loans and trade credits to the rest of the world to $1.6 trillion, or close to 2% of global gross domestic product, in 2018, from near-zero in 1998, according to the Reinhart study.

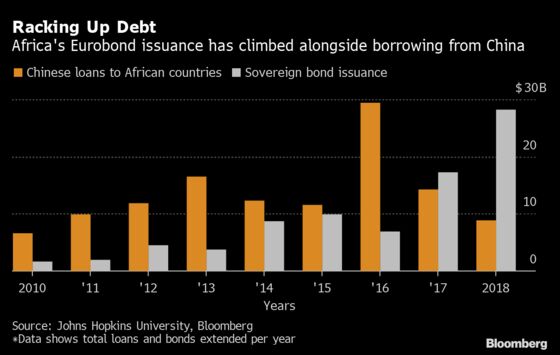

In just eight years since 2010, China extended $121 billion in loans to African nations. In addition, bondholders interested in the relatively high returns have provided $83 billion of risky debt in the same period, according to data compiled by Bloomberg.

“As a rising power, China has very different objectives in Africa than the private bondholders,” said Martyn Davies, Deloitte’s managing director for emerging markets and Africa. “I just can’t see how these interests can reconcile.”

Not only are their objectives different, but communication between them is almost nonexistent.

‘Tried Hard’

“We and other bondholders have tried very hard to engage with China,” said Lars Bane, a partner at London-based Farallon Capital Europe LLP and member of a group of private creditors holding regular talks with African borrowers. “It would certainly be beneficial for everyone to have better lines of communication so that we can all collaborate to work toward solutions, rather than the current silence.”

China has called on bondholders to follow its lead in granting relief to poor countries. Its official credit agency, the Export-Import Bank of China, has signed deals with 11 African countries to ease payment terms, Chinese foreign ministry spokesman Zhao Lijian said on Oct. 12. China would support equal treatment of all creditors, Wu Peng, head of the Africa department at the foreign ministry, said in a tweet on Oct. 20.

As a member of the Group of 20 leading economies, China earlier this month backed the renewal of a debt-relief initiative for the poorest countries through at least the first half of 2021. After some initial opposition, China also agreed to coordinate debt negotiations with the Paris Club, a move which could increase transparency.

But increasing tensions between the U.S. and China could undermine any rapprochement between Beijing and bondholders, said Ye Yu, an associate research fellow at the Shanghai Institutes for International Studies.

“High-level dialogue between the two could have provided a channel for China to communicate with private investors,” Ye said. “China feels that it’s contributing the most to the debt-relief initiative, but it’s still getting blamed for the debt problems abroad.”

Chinese lenders have so far been more lenient with African borrowers than private creditors. Over the past decade, China has restructured and refinanced about $15 billion of debt in Africa without slapping penalties or seizing assets from borrowers, according to a Johns Hopkins University study.

“China has been used a lender of last resort by countries like Zambia,” said Irmgard Erasmus, a Paarl, South Africa-based economist at NKC African Economics. “It’s a delicate game of theory for borrowers because China is a creditor that could help out after the crisis even if you have a bad credit record.”

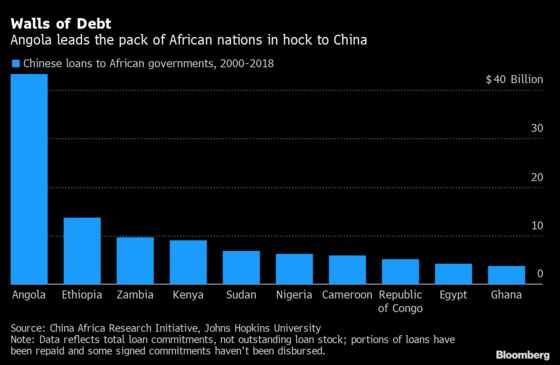

These Are the African Nations Most Indebted to China: Chart

Angering bondholders could lock governments out of debt markets for years, while irritating China would risk losing a reliable financier, making the IMF a potential mediator.

The renegotiation strategy may depend on the nature of a country’s exposure. Earlier this year Ecuador, which owes most of its debt to bondholders, first clinched a deal to reschedule payments to private creditors before agreeing to delay payments to Chinese banks. With the vast majority of its debt owed to China, Angola reached an agreement with Chinese lenders while it vowed to keep paying interest to bondholders.

In both cases, the IMF played a role with fresh credit, raising hopes that the global lender could serve as mediator to bring China and bondholders to the table. The lender also named a new representative to Zambia, two years after the post was vacated.

It could exert pressure on debtor countries by making funding contingent on restructuring, but its influence on creditors is limited.

“The agendas are not necessarily aligned, and IMF does not have the legitimacy necessary to be the arbiter,” said Agatha Kratz, associate director at Rhodium Group. “At the end of the day, Chinese banks and private creditors don’t want to be told what to do.”

©2020 Bloomberg L.P.