China Default Risks Hit Bid for Debut Dollar Bond Issuers

China Default Risks Hit Bid for Debut Dollar Bond Issuers

(Bloomberg) -- Chinese companies trying to sell dollar bonds for the first time have been finding it a whole lot tougher lately. So tough that the number of debut issuers is down by almost half this quarter compared with the last one.

And that’s while sales in the broader market are holding up amid China’s economic slowdown and the trade war. The issue: buyers are putting more scrutiny on borrowers now, thanks to a record pace of defaults.

“Issuers will have to do more to convince investors than before,” said Roy Kwok, a partner and senior portfolio manager at DeepBlue Global Investment in Hong Kong. First-time borrowers are usually second or third-tier companies in their sector, adding to credit-profile concerns, he said.

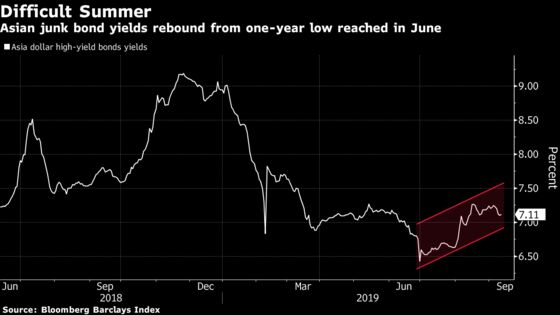

Buyers in the secondary market, too, are pressing for more, with yields on junk-rated Asian dollar bonds climbing since June.

Much of the Asian junk market is accounted for by developers from China. Chinese borrowers make up about 60% of issuance in dollar debt from Asia excluding Japan, which has raced to $244 billion so far this year, compared with just $61 billion back in 2009.

First-time issuers were a big source of that growth in sales. But now investors including DeepBlue, Pictet Wealth Management and Matthews Asia say they’re either avoiding those deals or asking for bigger pricing concessions.

That helps explain why there have been only 13 debut sellers so far this quarter, against 22 in April-to-June.

Investors are weighing the relatively poor performance of Chinese new issues and high-yield notes over the past two months, according to Thomas Wu, head of Asia fixed income at Pictet Wealth Management. “Debut names would need a meaningful first-time issuance premium,” he said.

Some 8% of Chinese debut issuers since 2016 have seen their ratings cut after selling their securities, according to data compiled by Bloomberg. That’s double the rate in the rest of Asia.

High-yield bonds in August handed investors their first loss this year, reinforcing the preference for safer credits. And there’s been a strong bias toward investment-grade sales as issuance rebounded this month after a slowdown in August.

Even so, the depressed levels of global bond yields are bound to leave some funds eager, and a Federal Reserve interest-rate cut next week could help open the door for greater risk taking.

“There are definitely opportunities in these new names, but the investor has to spend more effort understanding the company,” and why the issuer didn’t raise funds in the offshore market earlier, said Kwok at DeepBlue.

Many debut bonds are from China’s state-owned companies and local government financing vehicles that don’t have publicly traded equities. Their disclosures “can often be spotty,” according to Teresa Kong, a San Francisco-based portfolio manager at Matthews Asia.

“Even if we have sufficient info to form an initial investment opinion, we typically do not have timely or sufficient access to financial, disclosures, and the management team over the long term,” she said.

--With assistance from Adrian Yim.

To contact the reporters on this story: Rebecca Choong Wilkins in Hong Kong at rchoongwilki@bloomberg.net;Annie Lee in Hong Kong at olee42@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Christopher Anstey

©2019 Bloomberg L.P.