Here's Where China's Debt Iceberg Shows the Biggest Risk

Here’s Where China's Debt Iceberg Shows the Biggest Risk

(Bloomberg) -- In China’s financial system, the bigger the role of the state, the cheaper the funding costs. As a rule. But in one corner of the country’s $13 trillion bond market, something different has happened.

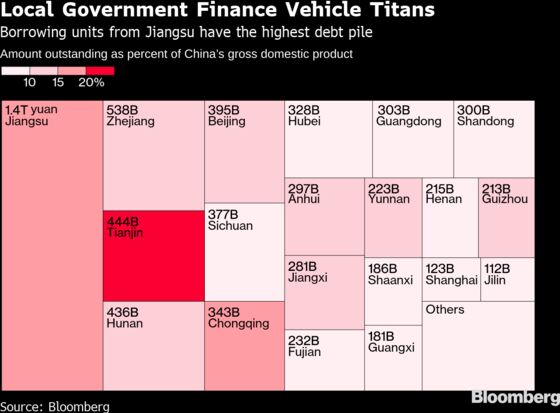

The highest yields in the 7.5 trillion yuan ($1.1 trillion) worth of debt sold by local government financing vehicles are found on the securities sold in regions where the public sector dominates the economy.

That analysis, conducted by Bloomberg on data as of April, showcases both the productivity gap between state-owned and private industries, and the increasing differentiation between weaker and stronger borrowers in Chinese bonds. As China’s economic growth slows, the pressure is set to grow for policy makers in Beijing to ensure against mass defaults.

“Places with the most noticeable debt risks, such as the northeast area, Tianjin, Guizhou, Yunnan and Chongqing, all have a bigger state-driven economy," said Wan Qian, China economist at Bloomberg Economics in Hong Kong. “Such a state-led model is less sustainable, and the debt may damage economic growth in the future,” she said.

As it gets easier for global investors to access China’s bond market, the world’s third largest, LGFV securities are potentially appealing. They enjoy both higher yields and a record -- up to now -- of implicit official backing. But as authorities crack down on the borrowing local governments have built up off of their balance sheets, refinancing risks are set to climb for some of the most indebted regions.

Among the takeaways from a Bloomberg analysis of LGFV bonds:

- In all but one of the provinces where LGFV debt yields on average 5% or above, state-owned enterprises hold more than half of industrial assets, according to data compiled using the China Statistical Yearbook 2018

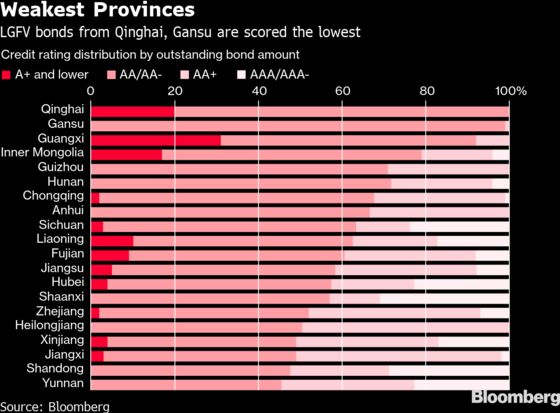

- In eight of the 10 provinces with the lowest ratings for LGFV debt, SOEs hold an above-average share of industrial assets

And here’s a look at some of the particularly weak provinces when it comes to LGFV debt:

Guizhou

One of China’s poorest provinces, Guizhou in the southwest of the country has been ramping up spending on infrastructure, with the fastest expansion in fixed-asset investment in 2018. Its LGFVs also pay the highest yields, at 6.14%.

High interest costs prompted local officials to seek cheaper refinancing from China Development Bank, the biggest so-called policy bank, which has been involved in some cases to ease LGFV debt risks.

Tianjin

This port city near Beijing is flashing warning signs, with the highest ratio of LGFV bonds to GDP in the country. It has seen several high-profile distressed cases from local state-owned companies in recent years. Among them: commodities trader Tewoo Group Co., a Fortune Global 500 company that saw its credit rating slashed six levels by Fitch Ratings last month. Bloomberg reported in April that the firm sought support from creditors including Export–Import Bank of China, another key policy bank, to extend its debt maturities.

Fitch has also downgraded several government-related entities in Tianjin to reflect its slowing growth and rising debt. The municipality, with about 16 million people, is expecting a third straight annual contraction in fiscal revenue this year.

Qinghai

This western province next to Tibet has lately been a focus for investors gauging the risk of an outright LGFV default, something credit analysts anticipate will occur at some point. Rating agencies have assigned junk-equivalent ratings to all the LGFV notes from Qinghai. After narrowly avoiding a default in September, Qinghai Provincial Investment Group Co. -- a state-backed aluminum maker with features similar to an LGFV -- missed a coupon payment in February, only to make good on the obligation within a few days. The mineral-rich province may continue to be scrutinized should demand for its natural resources ease alongside national growth rates.

The far northeast of China similarly has seen the twin pressures of managing debt as old-economy industries with heavy state involvement see revenues dwindle. Heilongjiang, Liaoning and Jilin are among those with weaker LGFVs, according to the Bloomberg analysis. Zheng Zhijie, China Development Bank’s president, said in March that CDB has been active in debt resolution cases in the northeast.

For now, LGFV securities are benefiting from policy makers’ shift to embrace credit expansion, said Gloria Lu, senior director of infrastructure ratings at S&P Global Ratings in Hong Kong. But without a clear LGFV debt-resolution strategy from the national government, the bonds pose credit risks over the long term, she said. Finance Minister Liu Kun wrote earlier this month that China will study measures to resolve local governments’ implicit debt.

The National Development and Reform Commission didn’t immediately reply to faxed questions about how concerned the regulator is about the refinancing pressure for LGFVs.

--With assistance from Vicky Wei, Shuqin Ding, Adrian Leung, Hannah Dormido, Ling Zeng and Mathieu Benhamou.

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net;Jing Zhao in Beijing at jzhao231@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, Christopher Anstey, Lianting Tu

©2019 Bloomberg L.P.

With assistance from Bloomberg