PBOC Ratchets Up Monetary Support With `Low-Profile' Rate Cut

The People’s Bank of China said it would supply lower-cost liquidity for as long as three years to banks

(Bloomberg) -- The People’s Bank of China said it would supply lower-cost liquidity for as long as three years to banks willing to lend more to smaller companies, as policy makers roll out targeted measures aimed at shoring up the flagging economy.

The central bank will create a “targeted” version of its Medium Term Lending Facility, and take applications from banks that meet regulatory requirements and have potential to increase credit supply to smaller companies, the PBOC said in a statement late Wednesday. The funds will be at a rate of 3.15 percent, lower than current facilities which have shorter maturities.

In addition to four cuts to reserve requirements so far this year, the new funding tool signals that policy makers remain concerned about the threat to economic growth posed by a clampdown on shadow banking that has gripped hard in recent months. Even so, the PBOC is stopping short, for now, of cutting borrowing costs across the board, a move that would pressure the fragile currency.

“This is a low-profile rate cut to bolster private and smaller companies," said Larry Hu, a Hong Kong-based economist at Macquarie Securities Ltd. "China is clearly gradually escalating the easing measures."

In a separate operation on Thursday, the bank kept short-term borrowing costs unchanged despite the rate hike in the U.S., another signal that policy makers intend to focus more on reinvigorating domestic demand. The yield of 7-day and 14-day reverse-repurchase agreements was kept the same in open market operations on Thursday.

| What our economists say... |

|---|

| "These easing measures are in line with our expectations the PBOC would combine measures that affect the economy as a whole as well as targeted policies in order to ease monetary conditions. They are positive in that they balance the easing with the need to contain financial risks" -- Chang Shu and David Qu Bloomberg Terminal clients can read the research HERE |

In tying longer-term liquidity to banks’ performance in lending to the real economy, China is further adapting an approach taken previously by central banks including the Bank of England and the European Central Bank. China’s major lenders have long had little incentive to lend to private companies -- the majority of which are small firms -- compared with safer bets funding state-owned enterprises.

Qualifying large commercial banks, joint-stock banks and city commercial banks can apply for the funding; the central bank will decide on the amount of funds to be provided depending on the growth of their lending to small and micro-sized enterprises and private companies, the central bank said in a separate statement.

Still, who’ll qualify isn’t clear. It could be a much larger group than those currently eligible for regular MLF loans, based on what the PBOC said in the statements. The central bank also needs to clarify what collateral will be required for the operation, the weighting ratio for each kind of collateral, how frequently the new tool will be used and whether it’ll be used simultaneously with the pre-existing MLF. If both are used at the same time, it may disturb the longer end of the yield curve as the central bank would be providing funds at two different prices.

In continuing to ease policy by increments, China is moving in the opposite direction to the U.S. Federal Reserve, which raised borrowing costs for the fourth time this year on Wednesday.

China’s large commercial lenders have lagged in increasing lending to the smaller firms this year, even amid an official campaign to shore up the private sector. The PBOC also expanded the quota through which banks can borrow to support specific sectors, known as the re-lending tool. That quota was increased by 100 billion yuan ($14.5 billion).

Economic policy makers gather this week in Beijing for an annual conclave that sets the priorities for monetary and fiscal policy for the coming year. The economy slowed again in November as retail sales and industrial production weakened, creating a challenging backdrop for that meeting.

PBOC Governor Yi Gang last week signaled that further policy moves were in the offing, saying that the central bank would remain supportive. Economists expect such support to involve another 200 basis points of reduction to the required reserve ratio for major bank, though most don’t currently forecast a cut to the benchmark 1-year lending rate.

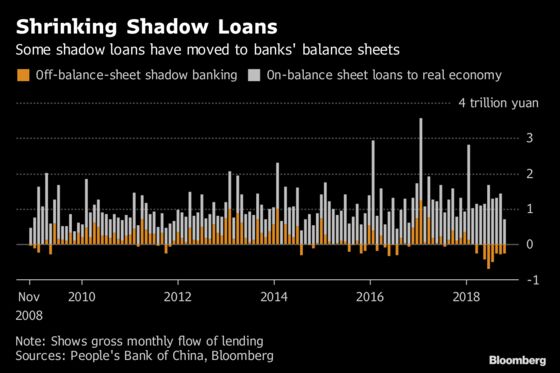

There are signs that credit-focused policy measures rolled out since mid-2018 are already helping to restart lending. The broadest measure of new credit exceeded estimates in November, as unofficial credit channels that the government wants to stem continued to contract.

Wednesday’s move can be seen as a “structural, targeted interest rate cut,” said Lu Zhengwei, chief economist at Industrial Bank Co. in Shanghai. Lowering the cost of the central bank’s loans to commercial lenders, rather than cutting benchmark lending rate, can avoid a leverage-ratio rebound and help stabilize market expectations on the currency, he said.

--With assistance from Crystal Chui, Xiaoqing Pi and Paul Gordon.

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, ;Malcolm Scott at mscott23@bloomberg.net, James Mayger

©2018 Bloomberg L.P.

With assistance from Bloomberg