China Private Company Bonds Lure Investors Betting on Easing

China Private Company Bonds Lure Fund Managers Betting on Easing

(Bloomberg) -- After shunning bonds from China’s private companies for most of the year, fund managers are beginning to see value. They expect the recently announced easing measures to help these cash-strapped firms relieve their funding strains.

The indiscriminate selling in bonds from non-state companies has left notes from good-quality companies "oversold,” according to Schroder Investment Management. For Pacific Securities Co., the current quarter is the "best time" to buy private sector bonds from industry leaders because risk premiums on them may “fall considerably by year-end against the backdrop of supportive policies.”

China’s privately owned firms were hit hard by the nation’s deleveraging drive. Tight funding conditions in the local bond market prompted investors to flock to debt issued by state-owned companies on assumption of government support. Private companies defaulted on 67.4 billion yuan of local bonds this year, 4.2 times that of 2017, Bloomberg-compiled data show, driving investors further away from this sector.

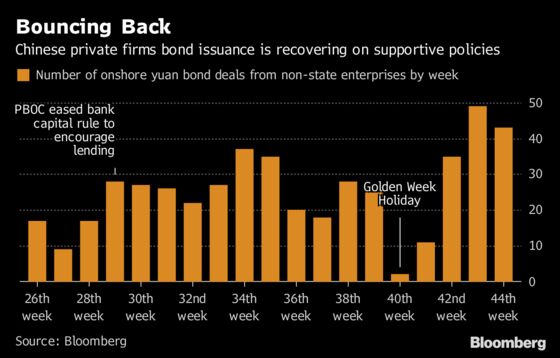

Policy makers have been forthcoming in lending support to the country’s private companies in recent weeks. Chinese President Xi Jinping last week repeated "unwavering" support for the private economy and pledged more measures such as tax cuts and financial support. The central bank last month announced a 150 billion-yuan ($21.7 billion) increase in financing as part of its plans to support private firms.

“The government has sent out clear signals to help private firms, which will lower short-term credit risk for the sector,” said Zhang Rui, chief fixed income investment manager at Changjiang Securities Co. Zhang plans to stick to private sector companies which are industry champions with a focus on short duration notes.

The improved sentiment has boosted demand for private company bonds with new issues rebounding in recent weeks, data compiled by Bloomberg show. There is optimism for private company bonds to perform after government-backed firms bought stakes in a rising number of private firms lately and the use of credit risk mitigation tools bolstered buyer confidence. Here are some examples:

- Beijing Orient Landscape & Environment Co.’s ability to access the bond market improved after it announced cooperation with several banks in August and introduced a state-backed firm as strategic investor. It successfully sold two notes since August after struggling to issue a bond in May.

- Chemical producer Zhejiang Hengyi Group Co.’s sold three-year notes at a coupon of 6.9 percent this month, 45 basis points lower than the similar-tenor bonds it sold last month. This was largely because credit-default swaps were sold on its November issuance.

- Shenwan Hongyuan Securities Co. expects the yield on chemical maker Hengli Group Co.’s 2 billion yuan 6.48 percent note, which was at 8.42 percent on Monday, to drop given its dominant market position and capacity advantages.

| Earlier stories about private sector funding pain in China: |

|---|

|

The revived interest in private sector bonds is not broad based and some investors remain on the sidelines. "Recent policies are definitely helpful but we want to see the effect of such policies before putting the money in," said Pillip Chen, a fund manager at HFT Investment Management Co. The yield on three-year AA- rated bonds, considered junk score in China, is still 33 basis points higher than at the beginning of the year, according to ChinaBond data.

For money managers such as Shi Min of Beijing Lerui Asset Management, it’s key to be selective. “Investors should single out these privately owned companies from promising industries that have sustainable competitive edge and sound levels of profitability and cash flow,” he said in an interview.

To contact Bloomberg News staff for this story: Jing Zhao in Beijing at jzhao231@bloomberg.net;Yuling Yang in Beijing at yyang329@bloomberg.net;Ina Zhou in Hong Kong at hzhou179@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Lianting Tu

©2018 Bloomberg L.P.

With assistance from Editorial Board