China Muni Bond Sales Start Sooner Than Ever as Growth Slows

Local governments in China are selling debt to raise cash earlier than ever to help shore up a slowing economy.

(Bloomberg) -- Local governments in China are selling debt to raise cash earlier than ever to help shore up a slowing economy.

Authorities in Sichuan and Henan provinces offered a combined 87.6 billion yuan ($12.6 billion) of so-called special bonds on Thursday in the earliest such issuance since nationwide sales began in 2015. Through 2018, sales began in March after the legislature formally approved the annual budget. But China has for a second year ordered local governments to move the timetable forward to speed up spending in areas like transport and energy infrastructure.

The acceleration comes as policy makers seek to manage the pace of a long-term slowdown, even though China’s economy is showing signs of stabilizing at a time an initial trade deal has been reached with the U.S. Analysts predict the debt will be well received by investors seeking lower-risk alternatives to corporate bonds, which are seeing rising defaults. The central bank’s liquidity injections should also help -- it said Wednesday it will cut the amount of cash lenders need to hold as reserves from Jan. 6, unleashing about 800 billion yuan in funds.

“Demand will be high because local-government bond yields are higher than central-government bonds but of the same sovereign ratings,” said Xing Zhaopeng, a markets economist at Australia & New Zealand Banking Group Ltd. “Banks will prefer local government bonds for both safety and return.”

Henan province sold 5-year, 7-year, 10-year, 15-year and 30-year special bonds at 3.14%, 3.31%, 3.38%, 3.67% and 3.97% respectively, according to a statement. Sichuan province issued 7-year, 10-year, 15-year, 30-year notes at the same costs and 20-year bonds at 3.71%.

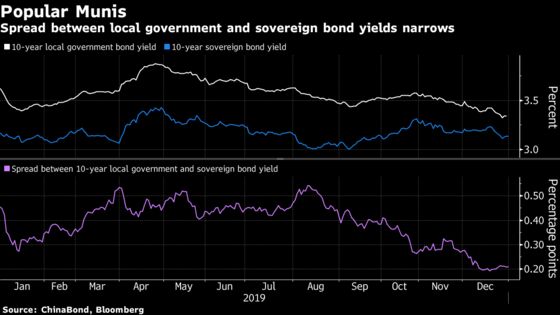

The spread between 10-year municipal and sovereign bond yields has narrowed to 20 basis points, indicating the rising demand for local-government notes.

The Ministry of Finance allocated a special-bond quota of 1 trillion yuan in November so that proceeds can be put to work early this year. The total quota for 2020 could ultimately reach 3 trillion yuan, said Becky Liu, Standard Chartered Bank (HK) Ltd.’s head of China macro strategy. With another 2 trillion yuan in general bonds likely to be rolled over, overall supply of local-government notes could top 2019’s around 4.4 trillion yuan, which was the most since 2016.

“We expect more local governments to announce bond-issuance programs in early January to lead to a strong start of LGB issuance in 2020,” said Liu. While this is within market expectations, “it will likely contribute to a slower decline or even marginal rebound of bond yields in early 2020, together with other factors including a likely stabilisation of growth.”

Thirteen provinces and cities have already disclosed plans to sell more than 480 billion yuan combined of special bonds plans in the first quarter. Zhong Linnan, a fixed income analyst at Yuekai Securities Co., forecasts 1.7 trillion yuan to 2 trillion yuan of muni bonds will be sold through March; the total was 1.4 trillion in the first three months of 2019.

--With assistance from Yinan Zhao and Helen Sun.

To contact Bloomberg News staff for this story: Livia Yap in Shanghai at lyap14@bloomberg.net;Wenjin Lv in Shanghai at wlv8@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, Fran Wang, Kevin Kingsbury

©2020 Bloomberg L.P.

With assistance from Bloomberg