China Is Missing Out on Huge Bond Rally Taking Off Globally

China’s bonds have dropped 0.02% since April, the worst performance among the world’s biggest debt markets.

(Bloomberg) --

China is the one place with a dovish central bank that’s yet to see a spectacular rally in government debt.

Including interest payments, the country’s bonds have dropped 0.02% since April, the worst performance among the world’s biggest debt markets. That’s even as the People’s Bank of China signaled its readiness to support the economy, with Governor Yi Gang saying he sees “tremendous” room to adjust policy. Authorities have also repeatedly injected cash into the financial system, boosted liquidity to support smaller banks and ramped up aid to small firms.

What gives? Theories include the protracted trade dispute with the U.S., concerns about credit risks after the surprise seizure of a local lender, a flurry of issuance in municipal bonds and a volatile yuan. While the European Central Bank and the Federal Reserve helped send more bonds than ever into negative-yielding territory this week, China’s benchmark 10-year yield hovers stubbornly around 3.3%.

“Expectations for PBOC easing aren’t as strong,” said David Qu, who covers China at Bloomberg Economics. “The market has also been waiting for the central bank to accommodate the surge in supply of municipal bonds with more liquidity, but that’s not fully in place yet.”

Read more about the world’s negative-yielding debt

The shock over the government’s seizure of Baoshang Bank to address its credit risks in late May is still rippling through the financial system. Bond traders now reluctant to accept riskier notes as security have clogged up funding among financial institutions, in turn pushing up borrowing costs for brokerages and smaller banks.

China also hasn’t actually cut benchmark interest rates since 2015, although it has taken other easing measures, including lowering the amount of money that banks have to put into reserves.

A surge in supply of municipal debt isn’t helping either: some 328 billion yuan ($47 billion) of local government bonds will be issued this week, the most this year, data compiled by Bloomberg showed. China’s 10-year government bond yield continues to trade within a narrow 10-basis-point band, and hasn’t dropped below 3% since 2016.

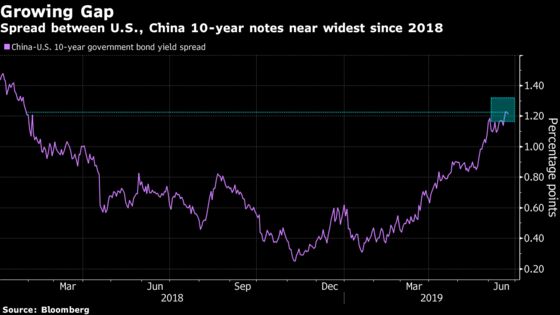

Not all is lost for Chinese bonds, though. Global investors may buy into the market now that yields are more attractive than those overseas, according to Kiyong Seong, an Asia rates strategist at Societe Generale SA in Hong Kong. The widening gap between U.S. and Chinese sovereign yields has enticed buyers before.

Chinese bonds also tend to be less correlated with shifts in global sentiment, making them a good option for investors looking to diversify, said Charles Chang, Hong Kong-based head of Asia credit strategy at BNP Paribas SA.

For now, the many domestic headwinds in China are keeping it from joining in the global bond rally, outweighing signs of support from the PBOC.

“Investors have been concerned about the risk of a weaker yuan and the long-term prospects of China assets,” said Seong. “An acceleration in local government bond issuance and sporadic noise in China’s financial market such as the Baoshang case have made investors more cautious.”

The yield on the most actively traded contract of 10-year government bonds was little changed at 3.26% as of 3:51 p.m. on Friday.

--With assistance from Yuling Yang.

To contact Bloomberg News staff for this story: Livia Yap in Singapore at lyap14@bloomberg.net;Claire Che in Beijing at yche16@bloomberg.net;Jing Zhao in Beijing at jzhao231@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, Magdalene Fung

©2019 Bloomberg L.P.

With assistance from Bloomberg