China Inc. to Suffer More Defaults in 2019 as Profits Stall

China Inc. to Suffer More Debt Defaults in 2019 as Profits Stall

(Bloomberg) -- China’s stimulus policies may not be enough to jump-start profit growth at the nation’s corporations, raising the prospects of more debt defaults next year, analysts say.

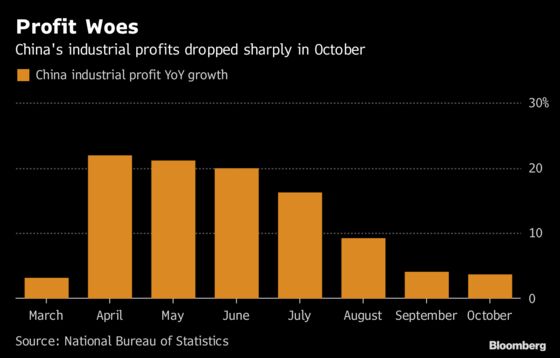

The world’s second-largest economy is expected to expand 6.2 percent in 2019 from 6.6 percent this year. Profits among industrial companies grew the least in seven months in October. The data don’t bode well for corporations’ ability to service their debts in 2019 after a record year of local bond failures in 2018.

“As credit lending and property sales are slowing down, private firms will face increasing liquidity pressure if their ability to make a profit worsens,” said Cindy Huang, analyst from S&P Global Ratings. “Supportive measures since the third quarter did not reverse the rising default trend in November, meaning such easing policies may only benefit publicly traded companies or industrial champions.”

What’s adding to the cash strains is a bond maturity wall of 3.5 trillion yuan ($507 billion) faced by China’s non-financial companies in the coming year. The number will grow by 36 percent if put options are exercised, further putting pressure to companies’ cash flow. Chinese firms have defaulted on 108 billion yuan of local notes in 2018, more than triple the tally last year.

Chinese President Xi Jinping in November repeated "unwavering" support for the private economy and pledged more measures such as tax cuts and financial support. The central bank in October announced a 150 billion-yuan increase in financing as part of its plans to support private firms.

Below are analyst views on China’s default outlook in 2019

Cindy Huang, analyst from S&P Global Ratings

- Upstream companies in the commodity sector may face liquidity pressure as oil and commodity prices drop; investors should also be cautious about small property developers due to a sales slowdown and refinancing difficulties

Mo Qian, head of fixed income research from HFT Investment Management Co.

- Credit risks in China will likely diverge in 2019, because weaker firms will continue to generate lower profits while easing measures can alleviate refinancing difficulties for stronger ones

- Defaults on publicly sold bonds from local government financing vehicles are less likely, as infrastructure investments are booming, but investors should pay heed to those that may have engaged in illegal financing in places such as the northeastern region and Guizhou Province

Chen Su, bond portfolio manager at Qingdao Rural Commercial Bank Co.

- Default risks have not shown signs of abating, and it takes time for market sentiment to improve further as some investors still only prefer bonds sold by companies that have already secured bank support

- Small property builders and "zombie LGFVs" that have loose business connections with public utility sector may face more credit risks

Here is a look at what happened in 2018

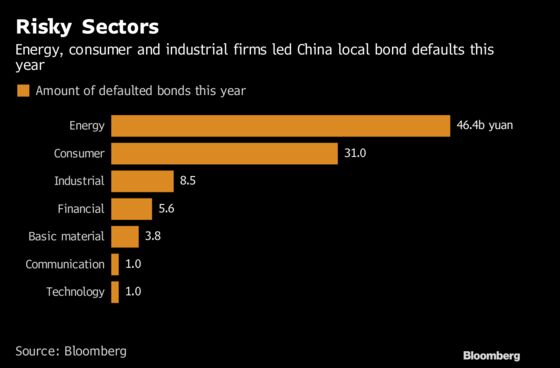

China’s energy firms have contributed the most to a record run in domestic bond delinquencies so far this year, with oil firm CEFC Shanghai International and coal miner Wintime Energy Co. being the top defaulters, according to data compiled by Bloomberg.

- Energy sector has defaulted on 46.4 billion yuan of local notes, followed by consumer companies that missed 31 billion yuan of bond repayment

- NOTE: CHINA DEFAULT WATCH: Local Failures Almost Quadruple 2017 Tally

- By regions, Shanghai witnessed the most defaults with 29.7 billion yuan of bond failures

- CEFC Shanghai missed repayments on 25.1 billion yuan of bonds, accounting for 84.5 percent of total defaults in Shanghai

- Shanxi (16.5 billion yuan) and Zhejiang (10.3 billion yuan) Province took the second and third spot

- Wintime Energy is headquartered in the coal-rich Shanxi province, and defaulter Neoglory Holding, which trades accessories and furniture, is based in Zhejiang

- In 2017, the top two regions with corporate defaults were Beijing and Inner Mongolia

- China’s credit market performance has been diverging for the most part of 2018, as spreads between three-year AAA and AA- rated corporate notes widened from 150 basis points at the end of 2017 to 260 basis points on Monday: Bloomberg-compiled data

--With assistance from Hannah Dormido.

To contact Bloomberg News staff for this story: Tongjian Dong in Shanghai at tdong28@bloomberg.net;Yuling Yang in Beijing at yyang329@bloomberg.net;Molly Dai in Singapore at bdai13@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Lianting Tu, Chan Tien Hin

©2018 Bloomberg L.P.

With assistance from Bloomberg