China Posts Weakest Factory Activity on Record

Activity in China’s manufacturing sector contracted sharply in February, with the gauge hitting the lowest level on record.

(Bloomberg) --

Activity in China’s manufacturing sector contracted sharply in February, with the official gauge hitting the lowest level on record, highlighting the devastating impact of the coronavirus on the economy and raising the risk of a worsening global stock rout.

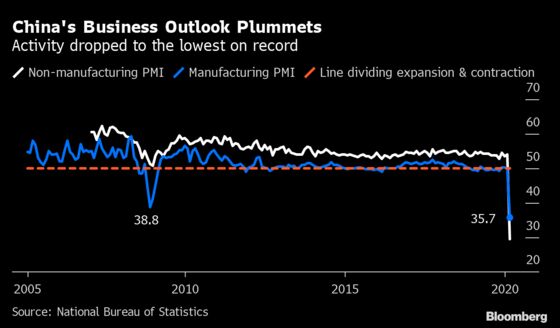

The manufacturing purchasing managers’ index plunged to 35.7 in February from 50 the previous month, according to data released by the National Bureau of Statistics on Saturday, much lower than the median estimate of economists. The non-manufacturing gauge also fell to its lowest ever, 29.6. Both were well below 50, which denotes contraction.

The coronavirus outbreak that started in China is spreading to multiple continents, with the threat of a pandemic tipping U.S. stocks Friday into the worst rout in any week since October 2008. With China, the world’s largest exporter already operating far below capacity as millions of workers and consumers remain quarantined, the data underline the scale of the task to return output to normal at a time when global growth is under threat.

“The sharp drop in China’s manufacturing PMI in February reinforces our view that the normalization in economic activity will be delayed,” as can be seen in high-frequency data, said Xing Zhaopeng, an economist at Australia & New Zealand Banking Group. “There’s scant chance for a V-shaped rebound -- the authorities are using targeted aids more than stimulus to stabilize the economy and that will lead to a gradual bounce.”

| Manufacturing Survey Details |

|---|

|

The result will shock markets on Monday, according to Iris Pang at ING Bank NV in Hong Kong, who said the yuan could weaken through 7 to the dollar. An index of the biggest 300 Chinese firms listed on the Shanghai and Shenzhen exchanges lost more than 5% in the trading week ended Friday, the most since April last year.

The collapse in economic activity seen in the data was largely due to virus control measures that have made it hard for workers to travel back after Lunar New Year, and left factory owners with limited raw materials to restart production. The key for any recovery this quarter will be how soon factories, companies and people can return to normal, but the government must balance that with the need to stop further infections.

Progress on that front has been made in recent weeks, with Bloomberg Economics estimating Chinese factories were operating at 60% to 70% of capacity this week. The statistics bureau said Saturday that as of Feb. 25, the work resumption rate at mid- and large-enterprises in the PMI survey was 78.9%, and will rise to 90.8% by the end of next month. At medium- and large-scale manufacturing companies, it was 85.6% and will rise to 94.7% by end-March, the NBS said.

However, even if companies have restarted that doesn’t mean that they are back at full capacity, or that the logistics systems in China are working normally. The services sector has taken a hard blow as most businesses rely on human interaction, which is constrained by tight control of people’s mobility within and across cities. The indexes for construction and services both plumbed record lows in data from 2012.

What Bloomberg’s Economists Say...

“The data confirm the worse fears about a juddering halt in China’s economy in the first quarter, with significant spillovers to the region and the world.”

The PMI should recover a little in March, but the damage will be far from being unwound and support from the government and central bank will strengthen, including more fiscal support, cuts to reserve requirement ratios for banks and lower borrowing costs.

-- Chang Shu, David Qu, Tom Orlik

See here for full note

“Most people were comparing the impact of the coronavirus with that of SARS, but I think it is on par with that of the financial crisis in 2008,” said Larry Hu, head of China economic research at Macquarie Securities Ltd. “The shock brought by the coronavirus is huge and the situation looks really bad in the short-term,” although there will be a rebound in March and a significant recovery in the second quarter, he said.

The virus outbreak has prompted economists to scale back their estimates for China’s expansion this quarter, with the median forecast at 4.3%. Analysts are split on whether the economy will suffer a short-term slide that’s swiftly reversed as the virus is brought under control, or a longer-lasting slump.

Zhou Hao, an economist at Commerzbank AG in Singapore, expects a rebound will start from March, but he said that what the market is concerned about is how significant the recovery will be, and 45 in the manufacturing gauge would be a key level to watch.

“It could be around that level but am uncertain that it will be higher. China now seems to stabilize, as it is widely expected that the manufacturing restart rate will be 80% by the end of March, but in other places, the outbreak is spreading, posing new risks,” he said.

In the last week there has been a jump in infections in Japan and South Korea, two countries whose economies and supply chains are intricately linked with China. If the outbreaks there lead to substantial shutdowns for businesses, the economic effects of the coronavirus will last even longer, even if China gets back to normal.

China’s manufacturing activity may be worse than the official data reflect, Lu Ting, chief China economist at Nomura Holdings Inc. in Hong Kong, wrote in a note to clients. The distortion is caused because lengthier delivery times due to the coronavirus are actually pushing up the headline number, Lu said.

Longer delivery times usually indicate higher demand but in this case it was “due to travel bans instead of good business,” according to Lu.

--With assistance from Miao Han and Tomoko Sato.

To contact Bloomberg News staff for this story: Lin Zhu in Beijing at lzhu243@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, James Mayger, Shamim Adam

©2020 Bloomberg L.P.

With assistance from Bloomberg