China Factory Rebound Hints Worst Is Over as Stimulus Lies Ahead

China Factory Rebound Hints Worst Is Over as Stimulus Lies Ahead

(Bloomberg) --

A rebound in China’s manufacturing sector and a shift by government leaders to loosen the reins on borrowing suggest the worst may be over for an economy suffering its biggest slump in decades.

While a bounce in the official purchasing managers’ index from a record low in February was inevitable as workers returned to factories after an unprecedented shutdown, the scale of the rebound -- to 52 in March from 35.7 -- exceeded most economists’ expectations.

“The positive surprise in China’s PMI headline reading offers hope that if virus containment becomes more effective in a country, then economic activity can quickly resume,” said Helen Qiao, chief Greater China economist at Bank of America Merrill Lynch.

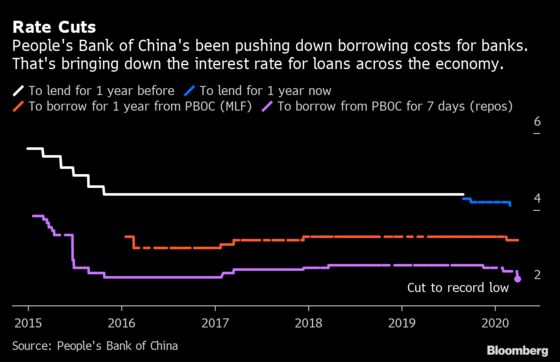

Recovery prospects have also been bolstered by the recent ratcheting up of the stimulus response -- though Beijing is still holding back from the pledges of unlimited support made in some developed economies. The People’s Bank of China on Monday cut interest rates for banks just days after the Politburo approved more borrowing.

The PMI is just one reading, and the economy remains on track for its worst slump since 1976. Even officials in Beijing were quick to say that the road back will be a long one. There’s also concern that any domestic rebound will be quickly snuffed out by the global slump.

What Bloomberg’s Economists Say...

“The improvement also offers a glimpse of hope that the virus hit -- as bad as it may be -- could be short lived, giving some solace to countries going through intense periods of virus infection. Yet despite improving conditions, the Chinese economy has not returned to normal, and faces challenges unseen for decades on both domestic and external fronts. Policy support is likely to be stepped up, especially fiscal measures. We also expect more monetary policy easing.”

--Chang Shu and David Qu

Some stimulus is already in the pipe: In its fiscal push, the government plans to increase the fiscal deficit, issue special sovereign debt and allow local governments to sell more infrastructure bonds -- though it hasn’t specified amounts. The central bank has steered some borrowing costs lower, but so far held the key deposit rate unchanged.

But it remains a relatively subdued stimulus response -- a role reversal from the 2008 global financial crisis when it led the world with a massive 4 trillion yuan stimulus. Economists say there are three main reasons for the policy restraint this time around:

- A perceived lack of policy room given already stretched budgets and dangerous debt levels

- The virus has interrupted the political calendar and delayed the annual meeting of the nation’s legislature where policy goals are signed off

- The command-style economy gives policymakers space to lean on banks and state-owned companies to keep things from falling apart

“It seems like some of China’s biggest weaknesses can be strengths in a crisis like this,” said David Loevinger, a former China specialist at the U.S. Treasury and now an analyst at fund manager TCW Group Inc. in Los Angeles. “The implicit guarantees that pervade China’s financial system and have distorted investment for years makes banks more willing to lend even in the face of rising credit risks, particularly if they are pushed by the Party.”

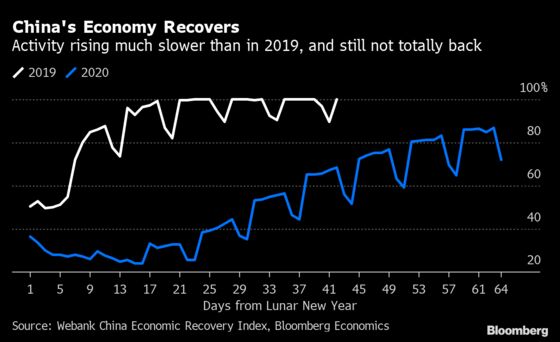

The sequence of the coronavirus outbreak puts China is a different position to peers amid government claims the deadly disease is under control. That has spurred the re-opening of factories, schools and shopping malls, getting the economy back to about 90% of its capacity, according to Bloomberg Economics.

Much now relies on demand from abroad, given China’s role as the world’s largest exporter. The outlook for the domestic economy hangs not just on stimulus from Beijing, but also the effectiveness of programs like the $2 trillion in aid announced by the Trump administration or almost unlimited bond buying by the European Central Bank.

The gradual return of normal activity will soothe officials, who remain haunted by the huge debt overhang left by the 2008 stimulus.

A recent paper by the Rhodium Group’s Daniel Rosen and Logan Wright argues that China’s disciplined policy approach reflects their limited options. Delays to promised reforms have left policy makers with an ugly choice: act less heroically on the stimulus front today or walk deeper into a debt trap tomorrow.

“Even Beijing’s ‘bazooka’ options to boost the economy face difficulties supporting an impaired financial system and indebted state-owned and local government firms,” they wrote.

China is still expected to have an unprecedented economic contraction this quarter, something that would have been unthinkable before the viral outbreak.

If the recovery hinted at in Tuesday’s PMI reading can be sustained in the coming months, the targeted stimulus approach may prove to have been enough to support the economy through the worst of the virus shock.

“The mechanisms for government support of specific industries and financial institutions are baked into China’s economic system, which breeds inefficiencies in good times but serves as an effective backstop when faced with potential crises,” said Eswar Prasad, who once led the International Monetary Fund’s China team, and is now at Cornell University.

©2020 Bloomberg L.P.

With assistance from Bloomberg