Debt Is Roaring Back in China

China Deleveraging Is Dead as $34 Trillion Debt Habit Roars Back

(Bloomberg) -- For almost two years, the question has lingered over China’s market-roiling crackdown on financial leverage: How much pain can the country’s policy makers stomach?

Evidence is mounting that their limit has been reached. From bank loans to trust-product issuance to margin-trading accounts at stock brokerages, leverage in China is rising nearly everywhere you look.

While seasonal effects explain some of the gains, analysts say the trend has staying power as authorities shift their focus from containing the nation’s $34 trillion debt pile to shoring up the weakest economic expansion since 2009.

“Deleveraging is dead,” said Alicia Garcia Herrero, chief Asia Pacific economist at Natixis SA in Hong Kong.

The question now is whether China’s attempt to create a healthier mix of financing -- fewer shadow banks, longer debt maturities -- will prove successful. Premier Li Keqiang underscored the challenge last week, warning of risks from sharp increases in short-term debt after China’s credit growth surged to a record in January.

“Chinese regulators are now trying to walk a fine line by allowing credit to flow back into the private sector without returning to the old pattern of rapid and unsustainable credit growth,” said Nicholas Borst, a China research director at Seafarer Capital Partners LLC in Larkspur, California.

Even after accounting for seasonal distortions, China’s leverage indicators have been surprisingly strong in 2019:

- New yuan loans jumped by a record 3.23 trillion yuan ($481 billion) in January, exceeding estimates

- Shadow financing rose for the first time in 11 months; interbank borrowing climbed to a six-month high

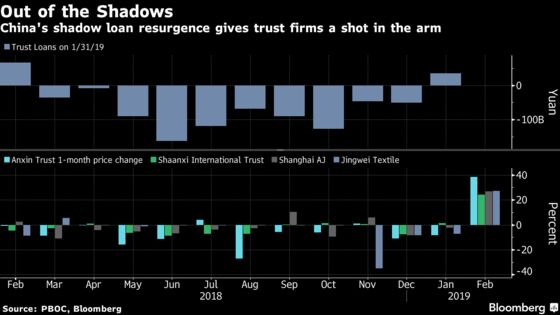

- More than 1,800 new trust products have been sold so far this year, the fastest start since at least 2008, according to Use Trust

- Banks issued 22 percent more wealth-management products in January than the year-earlier period, according to PY Standard

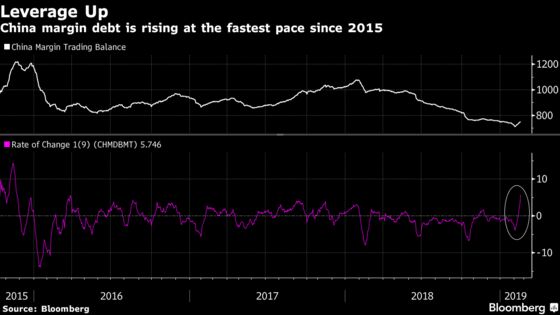

- Margin debt in China’s stock market surged over the past two weeks at the fastest pace since 2015

In the latest sign of the government’s evolving stance, a quarterly policy report published by the People’s Bank of China on Thursday watered down language on the campaign to curb excess credit, removing a reference to deleveraging and adding wording on “stabilizing the macro leverage ratio.”

“China has shelved deleveraging activities almost entirely to support the economy,” said Iris Pang, a Hong Kong-based economist at ING Bank NV.

The PBOC and the China Banking and Insurance Regulatory Commission didn’t respond to faxed requests for comment.

Read more: China’s stimulus measures, from reserve-ratio cuts to lower tariffs

China’s total debt will rise relative to gross domestic product this year, after a flat 2017 and a decline in 2018, Wang Tao, head of China economic research at UBS Group AG in Hong Kong, predicted in a report this month.

While Wang cautioned that “re-leveraging” may increase concerns about China’s commitment to ensuring financial stability, investors have so far cheered the prospect of easier credit conditions.

Yields on lower-rated Chinese corporate bonds have dropped in 2019 and the nation’s stock market -- one of the world’s worst performers last year -- has soared (thanks also to signs of progress in trade negotiations with the U.S.). The small-cap ChiNext Index entered a bull market on Friday.

“In 2018, it was the double whammy from the deleveraging campaign and the trade war,” said Larry Hu, head of China economics at Macquarie Securities Ltd. in Hong Kong. “In 2019, it could be the interplay between softening growth and more supportive policy.”

--With assistance from Amy Li and Qingqi She.

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Miao Han in Beijing at mhan22@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, ;Jeffrey Black at jblack25@bloomberg.net, Michael Patterson

©2019 Bloomberg L.P.

With assistance from Bloomberg