China’s Central Bank Pivots to Easing as Growth Risks Build

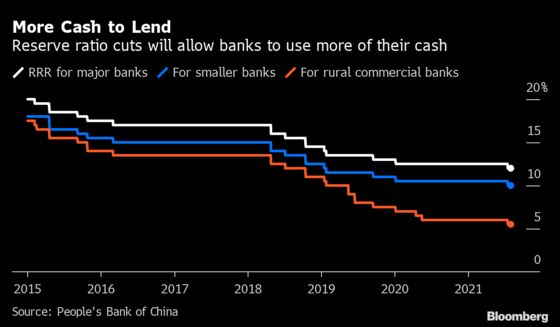

People’s Bank of China to reduce the reserve requirement ratio by 0.5 percentage point for most banks.

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

China’s central bank cut the amount of cash most banks must hold in reserve, a move that went further than many economists had expected and suggested growing concerns about the economy’s faltering recovery.

The People’s Bank of China will reduce the reserve requirement ratio by 0.5 percentage point for most banks, according to a statement published Friday. That will unleash about 1 trillion yuan ($154 billion) of long-term liquidity into the economy and will be effective on July 15, the central bank said.

The reduction was signaled earlier this week, when the State Council, China’s equivalent of a cabinet, hinted the central bank would make more liquidity available to banks so they could lend to smaller firms hurt by rising costs. The timing and magnitude of the move, coming a week before second-quarter growth data, suggests worries about the economy’s outlook and was a decisive shift away from policy tightening, economists said.

“The PBOC came in broader and sooner than expected, highlighting the policy urgency to support the China economy,” said Ken Cheung, chief Asian FX strategist at Mizuho Financial Group Inc. “Such firm easing measures could further fuel concern over China’s growth outlook in the second half as well as the upcoming second-quarter GDP figures in the coming week.”

| For more coverage |

|---|

|

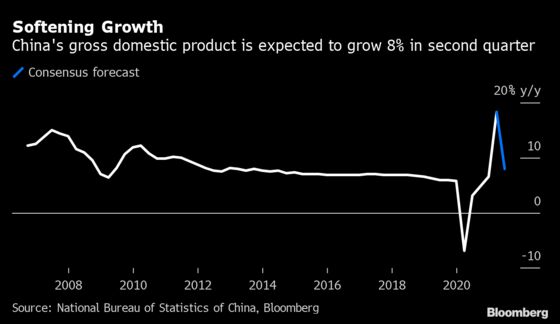

The last time the bank cut the main ratios was during the first wave of the pandemic in 2020, when it was trying to boost the economy after lockdowns to contain the Covid-19 outbreak. After a strong rebound, the economic recovery has shown signs of faltering recently, with soaring commodities hurting businesses and the services industry taking a knock because of subdued consumer spending and sporadic virus outbreaks.

Economists surveyed by Bloomberg expect next week’s data to show GDP growth slowed to 8% in the second quarter from record expansion of 18.3% in the previous three months, though the latter data were distorted by base effects.

China’s 10-year government bond yield pared gains of as much as four basis points after the RRR cut, standing little changed at 2.99% as of late Friday. FTSE China A50 futures rose as much as 1.1%.

The PBOC’s move puts it at odds with other central banks, like the U.S. Federal Reserve, which is discussing tapering its bond-buying program as it tries to exit from its pandemic stimulus. China’s central bank had been ahead of its peers in scaling back stimulus, and its about-turn now shows the difficulties policy makers will face in withdrawing support while the Covid-19 pandemic continues to rage.

China is wary of overstimulating the economy though, and the central bank said in a statement that the cut doesn’t mean there’s been a change to the “prudent monetary policy.” The PBOC will maintain the “stability and effectiveness of monetary policy, keep a normal monetary policy, and won’t flood the economy with stimulus,” it said.

What Bloomberg Economists Say...

The People’s Bank of China’s isn’t taking any chances with the recovery -- the surprise 0.5 percentage point cut to the required reserve ratio will inject 1 trillion yuan into the banking system, helping juice growth that’s poised to slow in the second half. The RRR cut and a larger-than-expected jump in June credit mark a decisive turn to an easing stance.

David Qu, China economist

For the full report, click here.

Overall liquidity in the economy will basically be stable, as the extra funds will be used to repay maturing medium-term loans, fill any liquidity gaps due to the tax season from mid to late July, and raise long-term capital, the bank said.

A reserve ratio cut, while not immediately lowering the cost of borrowing in China, is a rapid way of freeing up cheap funds for lending and has been a favored tool in the central bank’s efforts to control the economic slowdown in recent years.

“The magnitude of the RRR cut is more than expected. The RRR reduction paints quite a stark contrast to PBOC’s very cautious stance on its liquidity injections in the first half of the year,” said Ding Shuang, chief economist for Greater China and North Asia at Standard Chartered Plc in Hong Kong. “Even though the central bank said the cut shouldn’t be seen as a sign it’s shifting its policy stance, the market will interpret the move as a tilt toward looser monetary policy in the second half.”

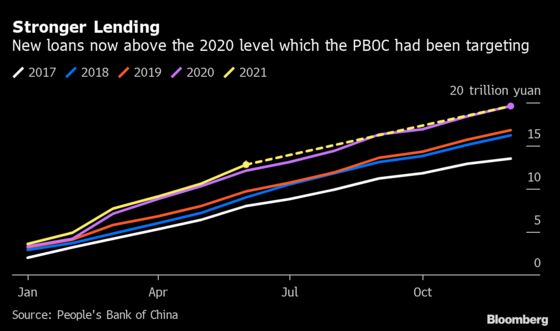

The announcement came just after the release of data showing that credit growth in June was much stronger than expected, with much of that expansion coming from bank loans.

The RRR cut comes against the backdrop of stable interest rates. The PBOC has refrained from changing its policy rates since cutting them early last year during the height of the pandemic in China. It gradually tightened monetary policy since late 2020 through guiding credit growth lower. The PBOC has also offered annual RRR discounts to qualified lenders since 2017 as part of an “inclusive financing” program to help guide funds to flow into corners of the economy where credit is traditionally scarce.

Tommy Wu, lead Economist with Oxford Economics, said he doesn’t expect broad-based easing from the PBOC as the recent waning in growth was likely due to temporary issues.

“The recent economic slowdown was caused largely by new Covid-19 related restrictions and supply chain hiccups, including the temporary closure of Shenzhen port after a local coronavirus outbreak,” he said. “Monetary easing won’t help much in such circumstances, and the downward pressures should be temporary.”

©2021 Bloomberg L.P.

With assistance from Bloomberg