China Buyers Return to $1.1 Trillion Local Unit Debt Party

China Buyers Return to $1.1 Trillion Local Vehicle Debt Party

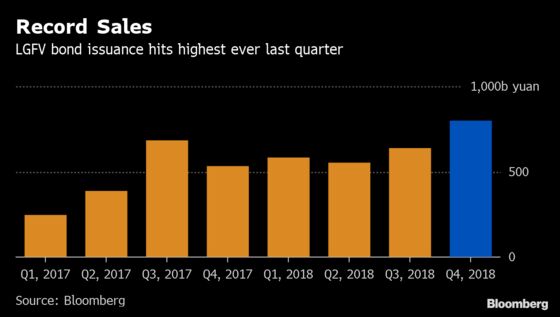

(Bloomberg) -- China’s sputtering growth has turned cash-strapped local government financing vehicles into darlings of the bond market.

Just a couple of years ago, local government borrowing units’ debt was on everyone’s top worry list as authorities vowed to cut state backing for those platforms. Now, policy makers have again turned to them to carry out infrastructure projects to resuscitate the sluggish economy. Their resurgence to national importance status has underpinned the big rush into LGFV bonds.

The bullish wave has pushed down yields on LGFVs’ debentures to below those of similarly rated corporate bonds, with the negative spread now just shy of the record reached in August 2016. Riskier notes with higher returns from the sector are much sought after in China as yields on yuan bonds have retreated overall amid a flurry of easing measures since the second half of last year.

“Falling risk-free interests and rising defaults in the private sector have prompted investors to add more lower-rated LGFV notes to their portfolios,” said Lv Pin, fixed income analyst at Citic Securities Co. in Beijing. “There are few high-yield assets in China right now.”

Investor ardor for the securities isn’t unfounded. Policies from a State Council meeting in July encouraged financial institutions to meet local borrowing units’ "reasonable" funding demand. China’s eastern province of Jiangsu is experimenting ways to fix Zhenjiang City’s debt problems by having lenders provide cheaper funding to it, Bloomberg reported last month.

Zhenjiang City Construction Industry Group Co., an LGFV, sold a one-year yuan note at a coupon of 4.5 percent on Feb. 25, nearly as low as China’s benchmark lending rate. In January, the AA+ rated firm issued a 270-day bond at 6.7 percent.

Not everyone is bullish because of the risk to how much longer government support can last.

LGFVs defaulted on about 15 loan products such as trust financing last year, a record increase, said Xu Hanfei, chief fixed income analyst at Industrial Economics Research & Consulting Co. in Shanghai. “If government bailout continues to be the solution to their existing debt problems, then it will lead to significant moral hazard," Xu wrote.

LGFV notes have also rallied so much that any further gains will be limited and will remain volatile in the short run, said Yang Yewei, a fixed income analyst at Southwest Securities Co.

LGFVs, set up during the global financial crisis, have accumulated much of the 40 trillion yuan ($6 trillion) hidden debt that Chinese municipal government kept off their balance sheet, S&P Global Ratings said in an October note. There are currently 7.6 trillion yuan of LGFV notes outstanding, according to Bloomberg-compiled data. Premier Li Keqiang said in annual report to the National People’s Congress on Tuesday that LGFVs’ debt problems should be addressed appropriately with market-based methods.

For now, there are still plenty of signs the government backstop is very much behind those platforms. For one, there has been no LGFV bond default so far when a record amount of corporate notes failed last year. Qinghai Provincial Investment Group Co., considered by some to have LGFV features, paid a missed coupon on its dollar bond last week, and narrowly avoided defaulting on its notes in September after being bailed out by the government.

“There are many ways local governments can resolve LGFVs’ debt problems and they will continue to be very cautious on public bond defaults by those units due to the negative implications on the regional financing activities,” Guotai Junan Securities Co. said in a report last month.

--With assistance from Ling Zeng.

To contact Bloomberg News staff for this story: Tongjian Dong in Shanghai at tdong28@bloomberg.net;Xize Kang in Beijing at xkang7@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Lianting Tu, Chan Tien Hin

©2019 Bloomberg L.P.

With assistance from Bloomberg