China Bonds Face Week of Reckoning as Loans, Key Data Come Due

China Bonds Face Week of Reckoning as Loans, Key Data Come Due

(Bloomberg) -- The rally in China’s government bonds has cooled as traders pared bets for further policy easing. Data in the coming days may help determine if the gains are revived.

The first clue on the rate outlook could come from liquidity operations on Monday before 700 billion yuan ($108 billion) of medium-term policy loans fall due. Reports on retail sales and factory output expected the same day are forecast to show growth slowed in July, bolstering the case for the People’s Bank of China to lower borrowing costs.

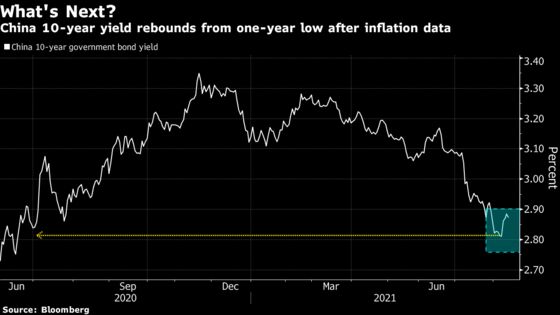

Asia’s second-biggest government bond market has been on a bull run, thanks in part to speculation that the PBOC could unleash more easing after reducing the reserve requirement ratio last month. But an unexpected acceleration in inflation is complicating the picture even as regulatory crackdowns and the virus outbreak threaten to derail the economic recovery.

China’s benchmark 10-year government bonds have halted an eight-week rally, in a possible sign that traders could be recalibrating wagers for further easing. The yield had earlier fallen to the lowest level since June 2020.

The liquidity operations on Monday are in focus, with 11 of 13 analysts in a Bloomberg survey expecting the PBOC to reduce the amount of funding. Bloomberg Intelligence and Commerzbank AG see the central bank adding about 500 billion yuan via the medium-term lending facility, while Mizuho Bank Ltd. and Huatai Securities Co. say the authorities will roll over all the loans falling due Tuesday.

All but one of those polled say policy makers will keep the MLF rate unchanged, while StanChart’s head of China macro strategy Becky Liu sees a slim chance of a rate cut.

“The key will be MLF rate and size,” said Stephen Chiu, Asia currency and rates strategist at Bloomberg Intelligence in Hong Kong. “It will send a policy signal to the market if there is any change in the operation rate. Size may be less important but anything less than the full rollover of 700 billion yuan may also dampen bonds.”

The focus on Chinese bonds has intensified after global funds boosted holdings to a record 2.18 trillion yuan on bets the PBOC may turn more dovish while other central banks prepare to withdraw stimulus. A long-awaited surge in the supply of local government bonds has yet to materialize, providing additional support for sovereign notes.

Maturing Loans

The rally in bonds could resume with more evidence expected to emerge that the recovery is slowing. Retail sales probably grew 10.9% in July year-on-year after increasing 12.1% the previous month, according to a Bloomberg survey of economists. Industrial production likely expanded 7.9% following an 8.3% advance in June, another survey showed.

Other reports due Monday are expected to indicate the pace of gains in fixed assets and property investments cooled in the first seven months, separate surveys showed. The benchmark one-year loan prime rate, which will be announced on Friday, is likely to be kept at 3.85%.

Below are the key Asian data and events due this week:

- Monday, Aug. 16: Japan 2Q GDP and June industrial production, China liquidity operations, July retail sales and industrial production, Thailand 2Q GDP

- Tuesday, Aug. 17: Singapore non-oil domestic exports for July, RBA minutes of August policy meeting

- Wednesday, Aug. 18: RBNZ rate decision, Japan June core machine orders, Indonesia July trade

- Thursday, Aug. 19: Australia July unemployment rate, Indonesia rate decision

- Friday, Aug. 20: South Korea July PPI, Japan July national CPI, China loan prime rates, Thailand foreign reserves, Taiwan July export orders

©2021 Bloomberg L.P.

With assistance from Bloomberg