China Bondholders Set to Learn How Much a Promise Is Worth

China Bondholders Set to Learn How Much a Promise Is Worth

(Bloomberg) -- China’s fast-growing dollar-bond market is facing a fresh test as investors that counted on a type of credit-protection pledge seldom seen elsewhere find out just what those promises actually mean.

So-called keepwell provisions, disproportionately seen in the offshore Chinese debt market the past several years, are a sort of gentleman’s agreement - a commitment to maintain an issuer’s solvency which stops short of a payment guarantee from the parent company.

Now, two issuers of debt with keepwell provisions, China Energy Reserve & Chemicals Group Co. and CEFC Shanghai International Group Ltd. have defaulted on their dollar notes in May. They are among the region’s first defaults to carry such agreements, according to Goldman Sachs Group Inc., and investors are about to discover whether they provide the benefit that was promised.

“It would be a good test and may provide a precedent for offshore investors," said Steve Wang, deputy head of research, BOC International Holdings Ltd. He expects guarantees to be a more standard choice with the further opening of the Chinese capital market.

A failed keepwell deed would be a further blow to China’s dollar bond market, where sentiment is already fragile with prices on junk debt plunging to a three-year low in May. Debt failures have spread after the government’s deleveraging campaign choked off some financing and the surge in Treasury yields raised cost of offshore funding, prompting some issuers to either shorten tenors or resort to floating-rate notes to pull in buyers.

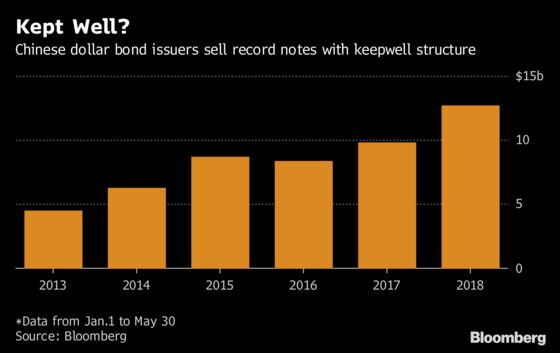

Chinese issuers have total about $100 billion of notes outstanding with keepwell agreements, accounting for about 80 percent of such dollar issued bonds globally, according to data compiled by Bloomberg.

Unlike guarantees, keepwell arrangements aren’t necessarily enforceable as a legal obligation, according to David Kidd, a partner at Linklaters, who focuses on restructuring and insolvency. “It offers some support, but when it comes to a default, the real question is whether there is an enforceable obligation.”

Keepwell Premium

Chinese issuers began using the keepwell structure about five years ago, as a means of assuaging concerns of risk-conscious overseas investors, by offering pledges from the parent of an issuer alongside bonds to enhance their creditworthiness. Investors initially distinguished the format, and required a risk premium of about 30-50 basis points over an actual guarantee, according to Jimond Wong, senior portfolio manager at Manulife Asset Management in Hong Kong.

Eventually that premium was whittled down to almost nothing as the market grew more comfortable with the structure, Wong said. Chinese borrowers have been using these credit boosters at a record pace this year, up 32 percent from $9.8 billion sold in the same period last year, according to data compiled by Bloomberg.

Never Enforced

In August 2016, China City Construction International Co., failed to make full payment on its 2.5 billion yuan Dim Sum notes with a keepwell agreement. Its parent, China City Construction Holding Group Co., said in a statement in July last year that the unit that issued the bond should repay the debt itself as it should have enough assets to cover both principal and interest payments.

China Energy said it is considering asset sales as it seeks to restructure its debt, and is working with all relevant stakeholders to remedy its default as soon as possible, in a filing that appeared on the Hong Kong exchange on May 27.

"These defaults will only help set a precedent for the market if bondholders go to court with China Energy and CEFC and if the court makes a ruling on how these need to be resolved,” said Anthony Leung, a Hong Kong-based senior analyst at Wells Fargo & Co.

--With assistance from Allen Yan, Carrie Hong, Annie Lee, William Hau, Yuling Yang and Denise Wee.

To contact the reporters on this story: Narae Kim in Hong Kong at nkim132@bloomberg.net;Lianting Tu in Hong Kong at ltu4@bloomberg.net

To contact the editor responsible for this story: Neha D'silva at ndsilva1@bloomberg.net

©2018 Bloomberg L.P.