China Bond Rout Worsens as Yield Jumps Most in Six Months

China Bond Selloff Worsens as Yield Jumps Most in Six Months

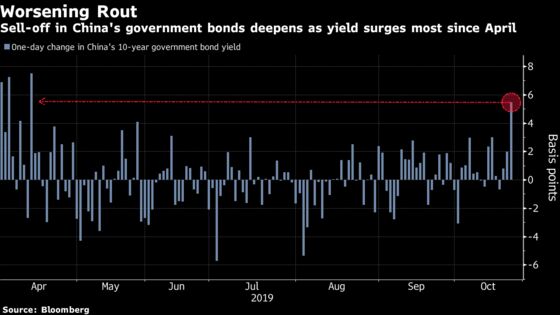

(Bloomberg) -- A sell-off in China’s government bonds is getting worse by the day.

The plunge in the sovereign notes accelerated on Monday, pushing the benchmark 10-year yield up by the most since April. Selling momentum surged to the strongest since late 2017, according to the 14-day relative strength index on the rate.

Risk appetite has returned as traders become increasingly optimistic that China and the U.S. will sign a partial trade deal next month. Meanwhile, bets for aggressive monetary easing have waned as the Asian nation’s inflation grew at a faster-than-expected pace in September.

The People’s Bank of China skipped open-market operations and refrained from using a targeted tool to add one-year cash on Monday, effectively draining a net 50 billion yuan ($7.1 billion) from the financial system as previously issued reverse repurchase contracts came due. Officials will provide a hint on whether they are willing to keep borrowing costs low as another 540 billion yuan of short-term funds mature over the rest of the week.

“Sovereign notes could drop more toward the confirmation of a trade deal in November,” said Stephen Chiu, an Asian currency and rates strategist at Bloomberg Intelligence. The debt will look attractive when the yield is close to 3.4%, he said, adding the rate could fall to 3.2%-3.3% by year-end. “I don’t think the risk-on mood could last. It’s too early to call it a happy ending of the trade war.”

The yield on China’s 10-year government bonds rose 6 basis points to 3.3% as of 4:50 p.m. in Shanghai. The cost has jumped 29 basis points since hitting a nearly three-year low in early September, making the notes some of the worst-performing in Asia.

The yuan’s 12-month interest-rate swaps climbed to 2.84%, the highest since May, suggesting traders are pricing in tighter liquidity.

To contact the reporters on this story: Tian Chen in Hong Kong at tchen259@bloomberg.net;Claire Che in Beijing at yche16@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, David Watkins, Philip Glamann

©2019 Bloomberg L.P.