China Bond Defaults Looking Less Scary. Why That Won’t Last

China Bond Defaults Are Looking Less Scary. Why That Won’t Last

(Bloomberg) --

The respite from defaults in China’s onshore bond market isn’t seen lasting as risks to the country’s economy grow.

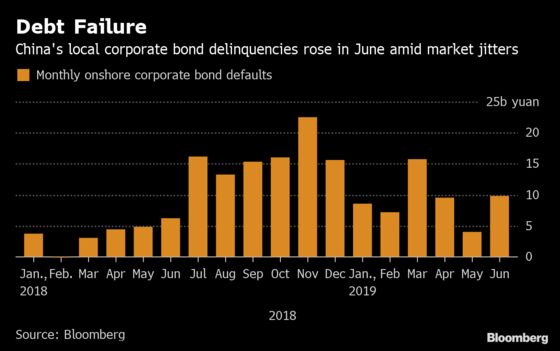

While the number of defaults in China’s $13 trillion bond market slid for a second straight quarter, down from a record high last year, June saw a resurgence as borrowing costs rose and liquidity tightened. Analysts and investors expect debt failures to rise in the months ahead, in tandem with slowing economic growth.

New bond defaults dipped to this year’s low in May amid China’s targeted support measures to shield the economy from a U.S. trade war. But, the number of both defaulted bonds and new defaulters rebounded the following month, coinciding with weak manufacturing data, indicating that the economic recovery in the first half has lost steam.

“We’ll see an uptick in default rates but from a low base,” said Alaa Bushehri, head of emerging markets corporate debt at BNP Paribas Asset Management. “We don’t expect a name which is doing fundamentally well to suddenly surprise us with poor fundamentals. We expect whatever is weak to be the weak links and trends of deterioration to continue to deteriorate.”

The tally of first-time defaulters climbed to five in June from one in May, according to data compiled by Bloomberg.

No Surprises

Defaults are seen picking up over the rest of the year, albeit at a gradual pace, said Harvey Bradley, a fixed income portfolio manager at Insight Investment, an affiliate of BNY Mellon Investment Management.

“This increase is likely to be driven by funding cost pressures, a weaker domestic economy and slightly more risk averse investors,” he said. “We would continue to expect default rates in the onshore Chinese bond market to creep up in the second half of the year - but nothing too concerning.”

READ: At Least 56 Chinese Companies Face Debt Repayment Pressure

China has a relatively short history of bond defaults and only saw the first local note failure in 2014. While delinquencies have climbed since then, they’re still not at levels seen in developed markets such as the U.S.

Liquidity jitters

Liquidity levels after the surprise takeover of Baoshang Bank Co. are still fueling some funding disquiet among some smaller banks and non-bank financial institutions, despite an injection of fiscal and monetary relief from Chinese authorities.

"After the Baoshang takeover, investors have more reservations about implicit government support and have become more risk averse," said Ivan Chung, head of greater China credit research and analysis at Moody’s Investors Service. This would put pressure on weaker issuers looking to refinance debt, he said.

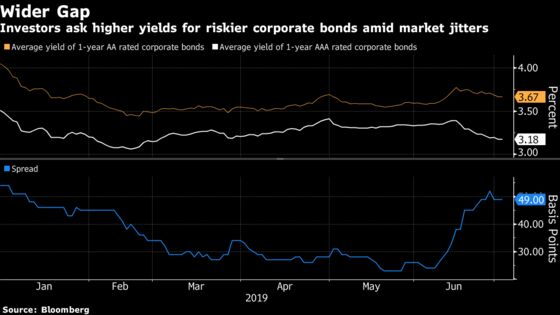

A Bloomberg survey conducted this month showed most of the 36 fixed-income analysts and investors believe the spread between lower-rated corporate bonds and risk-free yield will fluctuate slightly, or get wider in the third quarter.

“We see tight liquidity for the non-bank loan situation -- hence we are very cautious on private companies, the smaller SMEs and their ability to refinance their bonds,” says Tiansi Wang, a senior credit analyst for fixed income at Robeco. “They will face challenges because there’s less liquidity available to them and it’s at a much higher cost,” she said, identifying liquidity as “the big driver” of increased defaults in the second half.

To contact Bloomberg News staff for this story: Rebecca Choong Wilkins in Hong Kong at rchoongwilki@bloomberg.net;Tongjian Dong in Shanghai at tdong28@bloomberg.net;Molly Dai in Singapore at bdai13@bloomberg.net;Xize Kang in Beijing at xkang7@bloomberg.net;Ling Zeng in Shanghai at lzeng30@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Chan Tien Hin, Lianting Tu

©2019 Bloomberg L.P.

With assistance from Bloomberg