China Battles Against Hot Money With Swift Yuan Intervention

China Battles Against Hot Money With Swift Yuan Intervention

(Bloomberg) -- Already fighting economic fires on a number of fronts, China is rushing to clamp down on speculation in its strengthening currency before it gets out of control.

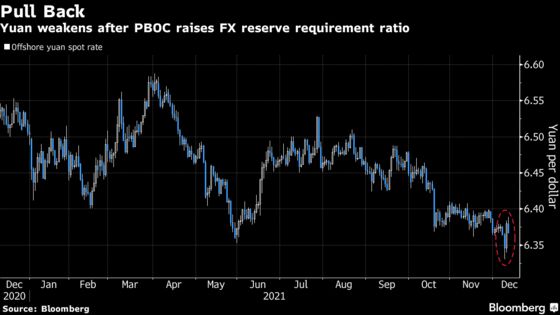

In the midst of managing a property slowdown and two of the country’s largest-ever corporate debt restructurings, the last thing Beijing needs is a rapidly appreciating yuan. China’s central bank attempted to ward that off this week, first forcing banks to hold more foreign currencies in reserve, then setting the daily reference rate far weaker than estimates. It may need to do more.

The country’s pivot toward easier policy this month has sent hot money flowing into stocks and government bonds, helping push the yuan to the strongest in more than three years. Overseas investors bought $3.4 billion of yuan-denominated stocks on Thursday alone, just shy of an all-time high, while foreigners hold a record $375 billion in government bonds.

China has long been paranoid about the risks posed by capital flows, especially after a messy currency devaluation in 2015, which is why authorities maintain strict controls on money entering and leaving the country. Rapid inflows raise the risk of asset bubbles, which could burst should the money start pouring out. Regulators in November warned financial institutions against making one-way bets on the yuan.

“Some of the flows will be hot money,” Hao Hong, chief strategist at Bocom International Holdings Co., told Bloomberg Television on Friday. “We have seen this movie in 2007 and also once again in 2015. It’s a double-edged sword -- once the hot money leaves the country the financial markets can get destabilized.”

High Base

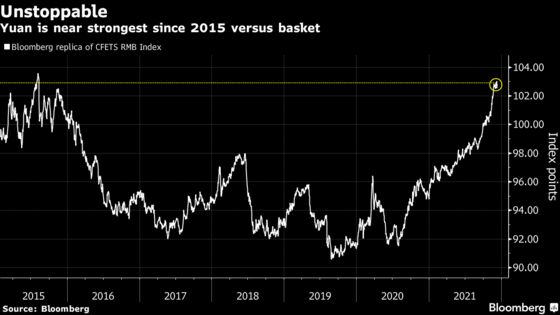

While the pace of gains hasn’t been particularly fast in recent weeks, the yuan was already at a high base. It has strengthened against every major peer this year and is near the strongest since 2015 against a basket of trading partner currencies.

China’s economic growth in recent months has slowed to rates not seen since 1990 (excluding the pandemic year) because of curbs on property financing, sluggish consumption and comparison with the strong recovery last year. Global demand for Chinese goods has partly helped offset that, with exports growing faster than expected in November to a record. But economists forecast just 3.1% economic growth in the current quarter.

Easing Stance

That has prompted China to adopt a more accommodative stance after a year dominated by deleveraging and a regulatory crackdown. Analysts expect policy makers will shift their focus to supporting growth at a key meeting aimed at setting the economic agenda, which may take place in the coming days. There’s growing speculation the benchmark rate for bank loans will be lowered this month for the first time since April 2020.

That means monetary policy in the world’s two largest economies will diverge again next year as the Federal Reserve withdraws stimulus. Trading that decoupling is emerging as one of the top ideas for macro strategists next year, with many turning bullish on Chinese assets as a result, raising the likelihood of capital inflows.

For President Xi Jinping’s government, 2022 is also a year of high political significance as the Communist Party convenes to decide the nation’s leaders for the next five years. A Politburo meeting earlier this week used the phrase “stability is the top priority” for the first time, according to Macquarie Group Ltd. analysts led by Larry Hu.

Currency Management

While China wasn’t named a currency manipulator by the U.S. last week, that doesn’t mean the yuan is free from Beijing’s control. After allowing the currency to surge in 2020 as China’s resilience to the coronavirus pandemic burnished the nation’s appeal to investors, the central bank appeared to anchor the yuan to the dollar at the start of this year.

But the currency’s strength in the second half of the year has been even more impressive, when judged against a resurgent dollar that itself has gained against all but one major peer.

The PBOC has a history of pulling on the currency’s levers in both directions in a “managed float” system. The so-called fixing -- long seen as a policy signal on the Chinese exchange rate -- has for five straight days been set at levels weaker than average estimates in Bloomberg surveys.

“The PBOC is sending a clear sign it’s uncomfortable with the recent surge of the yuan,” said Tao Chuan, chief macro analyst at Dongwu Securities. “Foreign inflows into yuan assets have accelerated recently, which has the potential to bring unwanted asset price volatility. The PBOC’s policies may help cool down foreign equity inflows, which can be risky if the flow reverses.”

©2021 Bloomberg L.P.