Bank of China Readies First Perpetual Amid Capital Pressure

Bank of China Readies First Perpetual Amid Capital Pressure

(Bloomberg) -- Bank of China Ltd. is set to offer the first perpetual bonds from a Chinese lender on Friday, a landmark deal that will pave the way for similar fundraising from financial institutions.

The bank is looking to issue as much as 40 billion yuan ($5.9 billion) of perpetual bonds to replenish additional tier 1 capital, it said in a filing. China’s financial regulators last year called for more innovative capital instruments to expand funding channels for banks in order for them to boost support to the real economy.

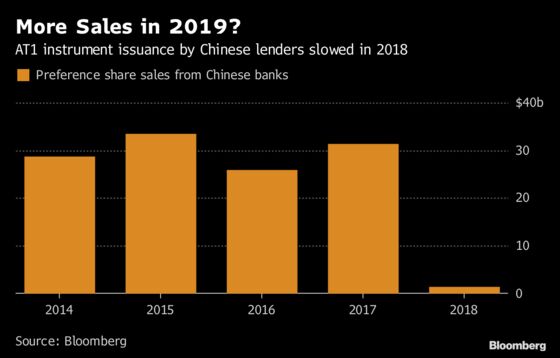

Chinese banks need stronger capital buffers as they are compelled to move off-balance-sheet lending onto their books and face more soured loans in a slowing economy. Lenders have so far replenished their additional tier 1 capital via issuing preference shares, which can be converted to equity when the issuer is under stress. Perpetual debt is a new way to boost that capital and more banks are gearing up to sell the securities.

"Chinese banks have been encouraged by regulators to diversify and expand their capital structure via issuing new instruments," said Nicholas Zhu, Beijing-based senior analyst with Moody’s Investors Service. He expects more issuance from the sector as financial institutions are under pressure to recognize shadow lending as formal loans.

Besides big state-owned lenders, the smaller ones are also keen to explore this new instrument. Harbin Bank Co. and Shengjing Bank Co. have announced their plans to raise up to 15 billion yuan and 9 billion yuan, respectively, from selling perpetual bonds, according to public filings.

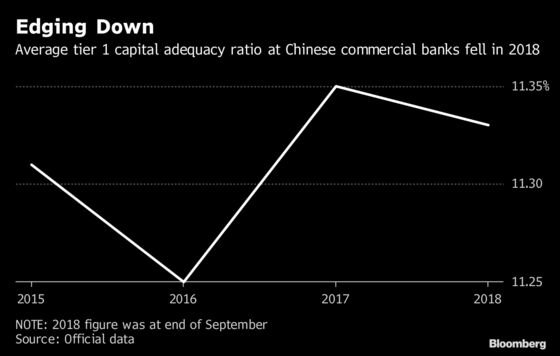

That’s because capital adequacy ratio for the sector has been falling, albeit slightly. At the end of September, Chinese commercial banks’ average tier 1 capital adequacy ratio was at 11.33 percent, down from 11.35 percent at end-2017, according to official data. While those numbers are still above the minimum regulatory requirement, analysts say Chinese banks in general lacked capital.

Coupons of Chinese banks’ perpetual bonds are likely to be in the range of 4 percent to 6 percent, which “does not look very attractive to Chinese investors,” Zhang Jiqiang, an analyst with Huatai Securities, wrote in a report. Asset managers, insurance firms and fund managers are likely to be the main investors for such securities, he said in the report.

Here is a look at the key characteristics of Bank of China’s perpetual bonds, according to its bond prospectus.

- Indicative pricing range of 4.50 percent to 4.80 percent, people familiar with the matter said last week

- No coupon step-up with coupon reset every five years

- Trigger Events: If the issuer’s core tier 1 capital adequacy ratio falls to 5.125 percent or below, it has the right to write off all or part of the aggregate amount of the securities. Or the earlier of the following events:

- The China Banking and Insurance Regulatory Commission having decided that the issuer would become non-viable without a write-off

- The relevant authorities having decided that a public sector injection of capital or equivalent support is necessary, without which the issuer would become non-viable

Here is a table illustrating the differences between preference shares and Bank of China’s perpetual bonds.

| Perpetual Bonds | Preference Shares | |

|---|---|---|

| Issuers: | Listed and unlisted banks | Listed banks |

| Venues: | China’s interbank bond market | Stock exchanges |

| Write-off or Conversion: | Write-off | Share conversion |

| Regulators: | CBIRC, PBOC | CBIRC, CSRC |

To contact Bloomberg News staff for this story: Ina Zhou in Hong Kong at hzhou179@bloomberg.net;Xize Kang in Beijing at xkang7@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Lianting Tu

©2019 Bloomberg L.P.

With assistance from Bloomberg