Fed Cut Raises Timing Question for China if PBOC Follows Suit

Economists expect the People’s Bank of China to ease inter-bank borrowing costs by the end of this quarter.

(Bloomberg) -- Economists expect the People’s Bank of China to ease inter-bank borrowing costs by the end of this quarter, a step that would put it in the slipstream of the U.S. Federal Reserve’s first rate cut in more than a decade.

The question for investors is: when could China move?

The central bank may lower the inter-bank policy rate -- the price it charges for the 7-day reverse repurchase agreements in the open market -- by 5 basis points by the end of September, according to a Bloomberg survey on July 15-23. Economists don’t expect any change in the economy-wide 1-year lending rate this year, ahead of a reform that will likely see its abolition.

However, the exact timing of the market-facing move is uncertain: the Fed’s first rate cut in a decade could be a chance to follow suit, but not necessarily straight away, according to economists.

While policy makers are under pressure to stabilize growth in the second half of 2019, and a cut to policy rates is very likely in the third quarter, it’s “difficult to tell” the exact timing, said Peiqian Liu, Asia strategist at Natwest Markets Plc in Singapore. “Policy makers may want to wait for more economic data, and take time to make better sense of the domestic economy before making a decision,” she said.

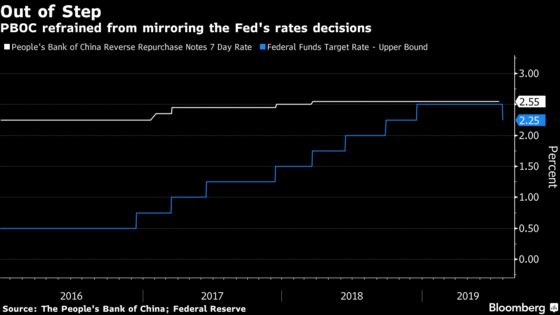

U.S. policy makers Wednesday lowered the target range for their benchmark rate by 25 basis points, in a move intended to “insure against downside risks.” When the PBOC has mirrored Fed moves previously, the decision has showed up in the daily open-market operation notice just after 9:00 a.m.

For now, China’s top leadership has signaled they’re reluctant to roll out major monetary measures, instead focusing on reform measures and targeted stimulus measures like corporate tax cuts. The PBOC hasn’t mirrored a Fed move since early 2018, when the growth trajectory of the world’s two largest economies started to diverge.

The PBOC also hasn’t adjusted its benchmark one-year lending rate -- a more powerful tool that governs rates across the entire economy -- since 2015. A reform of the interest rate system is underway which could also help lower the cost of borrowing and improve the effectiveness of easing measures in a risk-averse environment.

In spite of the strengthening easing cycle globally, the PBOC may now find it less necessary to tweak its market interest rates, as domestic cash supply remains ample. The nation’s key money market rate slumped to the lowest level in more than four years in early July before rebounding on seasonal factors.

The open-market rate can also only be adjusted when a liquidity operation is conducted. For example on Wednesday, the central bank skipped the operation, saying liquidity was “reasonably ample,” and thus removed any chance of a rates adjustment.

Still, lowering the inter-bank borrowing costs could be seen as necessary, otherwise appreciation pressure on the yuan will increase, as the yield premium Chinese bonds have over their U.S. counterparts will widen. The lack of any PBOC cuts may also shake traders’ expectations for policy easing, leading to an increase in money-market rates.

“While the PBOC won’t likely follow the Fed immediately, it may still cut policy rates by the end of this quarter, in a move to ease appreciation pressures on the yuan amid a weakening dollar,” said Xing Zhaopeng, a markets economist at ANZ Bank China Co. in Shanghai.

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net;Tian Chen in Hong Kong at tchen259@bloomberg.net;Claire Che in Beijing at yche16@bloomberg.net;Cynthia Li in Hong Kong at cli205@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, James Mayger

©2019 Bloomberg L.P.

With assistance from Bloomberg