Record Chinese Defaults Only Add to Allure of Junk Bonds

Record Chinese Defaults Only Add to Allure of Junk Bonds

(Bloomberg) -- A record year of bond defaults in China is, counter-intuitively, great news for investors in the nation’s junk-rated debt.

China’s riskier bonds have enjoyed an unexpected rally as they outperformed peers with stronger credit ratings, in a sign that investors have become more at ease with bond failures, which were largely unheard of until a few years ago.

That’s good news for policy makers who want to foster an efficient capital market that can play a bigger role in China’s economy, reducing the burden on the stretched banking sector. A fast-expanding pool of souring assets and the arrival of a new generation of risk hunters also helps create a more diverse bond market where borrowers’ creditworthiness is better reflected in pricing.

“The increase of defaults and more effective market pricing has channeled more funding into high-yield bond investment,” said Liang Yu, a bond analyst at Shanghai Sliver Leaf Investment Co., a private fund management firm.

Hit by an economic slowdown and trade tensions, Chinese companies have defaulted on 130.7 billion yuan ($18.7 billion) of domestic bonds so far this year, surpassing 2018’s full-year record of 122 billion yuan. Dollar bonds aren’t immune either, with a major commodities trader earlier this month becoming the biggest dollar bond defaulter among the nation’s state-owned companies in two decades.

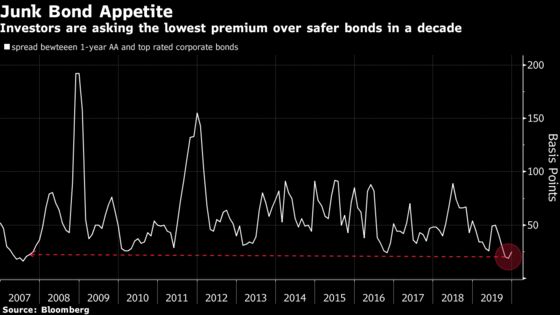

Still, average yields on one-year corporate bonds with a domestic rating of AA, the equivalent of junk bonds in China, rallied to 20 basis points above those on AAA-rated debt, the lowest level in more than a decade, according to Bloomberg-compiled data. Investors say they prefer riskier debt with a shorter maturity, which limits their exposure.

“Many institutions have started to test the waters in the fledging high-yield bond market, and it can hardly be ignored as the market size grows further,” Yu said.

China’s corporate bond market has a disproportionately brief history of defaults. The first onshore bond failure came in 2014 and the momentum didn’t gather pace until last year, when Beijing started allowing more defaults to instill stronger financial discipline as part of a broader war on debt.

Despite their quickening pace, defaults make up a sliver of the country’s $4.4 trillion corporate bond market. S&P Global Ratings said in a report last month that it expects China’s onshore default rate in 2019 to remain same as last year’s at 0.5%

Ming Ming, chief fixed-income analyst from Citic Securities said that defaults are having less impact on market sentiment as investors now have more experience in handling them.

China’s gross domestic product rose 6% in the third quarter from a year earlier, the slowest pace since the early 1990s but easing trade tensions with the U.S. is fueling expectations that the economy may recover, providing a boost to risky assets.

Top Picks

Top picks among risk lovers include lower rated bonds sold by local government financing vehicles and Chinese property companies, Ming Ming said.

Despite frequent trust loan failures, LGFVs have yet to suffer a bond default and they’ve benefited from Beijing’s efforts to prop up economic growth through infrastructure investments. Average yield on 1-year AA- rated LGFV bonds was at 4.57% on Tuesday, the lowest level since January 2017.

Chinese property bonds have attracted investors on hopes that a weak economy may force Beijing to eventually ease investment and financing curbs imposed on the sector.

Investors have found value in other sectors as well. One example is Kangmei Pharmaceutical Co., a drug maker at the center of one of China’s biggest accounting scandals. Investors who bought the company’s bonds at a price as low as 20 yuan in August at the height of its crisis saw their returns jump by four fold in a month, when Kangmei managed to deliver a full debt repayment.

“We believe that many onshore bonds have been oversold, meaning pricing is far below the true value of the securities, which will provide many investment opportunities,” said Brian Lou, a Shanghai-based portfolio manager at UBS Asset Management.

--With assistance from Jing Zhao and Molly Dai.

To contact Bloomberg News staff for this story: Tongjian Dong in Shanghai at tdong28@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Shen Hong

©2019 Bloomberg L.P.

With assistance from Bloomberg