China Faces Problem in Getting Its Banks to Lend More Money

The People’s Bank of China is tackling a problem in persuading banks to lend the money they have.

(Bloomberg) -- The People’s Bank of China is tackling a problem it rarely had to worry about until recently -- persuading banks to lend the money they have.

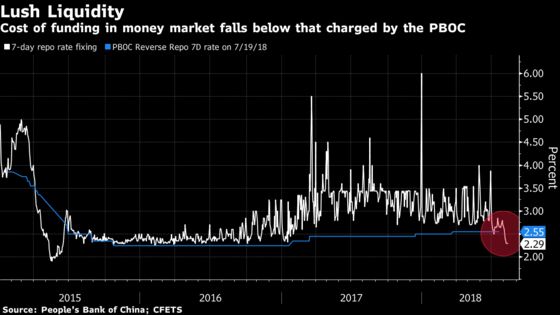

Thanks to the central bank turning on the liquidity taps, the cost for banks to borrow from one another is now lower than the cost to borrow from the PBOC, but a large chunk of those funds is sitting idle. That money isn’t feeding into the wider economy, especially not to cash-strapped smaller firms, as lenders are unwilling to make loans or buy risky bonds.

With China in a worsening trade war with the U.S. and also trying to control already large debts, ensuring funds get to needy companies is vital to sustain growth. Since the start of August, the central bank has begun softening rules to encourage lending, and a top-level meeting chaired by Vice Premier Liu He called for more efforts in “unclogging” the transmission mechanism, underlining the government’s sense of urgency.

Their efforts have had some initial success -- China’s new yuan loans rose more than expected to 1.45 trillion yuan ($210 billion) in July, according to preliminary data released by the Banking and Insurance Regulatory Commission over the weekend. Still, that only covers the credit extended by banks, and doesn’t include financing from the equity and bond markets or the shadow banking sector.

Whether liquidity offered by the central bank can be utilized depends on the “willingness and capacity” of both the supply and demand sides, the PBOC said in its quarterly report last week. Joint action from monetary, fiscal and regulatory authorities is needed to ensure better transmission, it said.

“Banks still don’t have enough confidence -- they’re still concerned about the rising credit risks amid a slower China economy, a return of the deleveraging campaign and the worsening trade war,” said David Qu, a Shanghai-based economist at Australia & New Zealand Banking Group Ltd.

Subdued Demand

While transmission wasn’t much of an issue when banks were working at full speed to turn base money into loans, the demand for and supply of loans is more subdued now.

“Declining risk appetite in markets, as well as inactive officials and people at financial institutions, impacts heavily on medium- and small-sized companies and private firms,” said Ma Jun, a central-bank adviser. The key to avoiding a dramatic shift in risk appetite and improving transmission is for the government’s policies to curb debt to be done at a controlled pace, Ma said, adding that this is “delicate, technical work.”

Non-banking funding channels aren’t a better source of money. Yields for low-rated bonds, usually sold by smaller companies, were at the highest since late 2014, and only recovered after the PBOC signal that they could be used for loan collateral.

China’s commercial banks sharply cut their holdings of corporate bonds in July in response to a heavy supply of local government paper, according to data from Chinabond and Shanghai Clearing House. That’s despite the central bank’s recent easing measures encouraging lenders to buy more company notes.

Equity Decline

Equity markets are also down, limiting the ability of companies to raise funds there. The Shanghai Composite Index dropped this month to the lowest since February 2016, and another stock gauge of small- and mid-sized companies tumbled to the lowest level in nearly four years.

Regulatory requirements and policy uncertainty for the future make financial institutions hesitant to offer credit, according to Lu Ting, chief China economist at Nomura International Ltd. in Hong Kong. He suggests policy makers better clarify the recent change in stance to dispel banks’ concerns over any future blowback from what they’re asked to do now.

Further monetary easing wouldn’t likely have any effect in lifting the economy, ANZ’s Qu said, suggesting instead that China turns to more targeted fiscal policies to improve risk appetite.

“With transmission remaining clogged, the urgency of another reserve-ratio cut any time soon drops as it won’t have much effect,” said Ding Shuang, chief economist for Greater China and North Asia at Standard Chartered Bank Ltd. in Hong Kong. “It’s likely to take a year until demand eventually recovers in the economy.”

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net;Tian Chen in Hong Kong at tchen259@bloomberg.net;Emma Dai in Hong Kong at edai8@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, James Mayger, Chris Bourke

©2018 Bloomberg L.P.

With assistance from Editorial Board