China Copper Partner for Barrick Gold Makes Sense, Thornton Says

Barrick Says China Partner for Copper ‘Makes All Kinds of Sense’

(Bloomberg) -- John Thornton is taking a page from the late Peter Munk’s playbook in recognizing the value of copper in Barrick Gold Corp.’s portfolio. But, he made clear to the gold miner’s employees this week, he also intends to avoid the founder’s mistakes.

The world’s largest gold miner almost destroyed itself with a top-of-the-cycle foray into copper in 2011. Executive Chairman Thornton is considering copper-growth options once again, but this time with Chinese partners.

“The question for us on copper is, ‘Can you take the copper assets, combine them with another party, or even two parties and build a first-tier global copper company over time?’ ” Thornton told employees Wednesday. “Now in answering that question, the likelihood that your partner in that endeavor will be Chinese is very high.”

Under Munk’s leadership, Barrick acquired Equinox Minerals Ltd. at the height of the commodity super cycle. The acquisition ballooned its debt to $15.8 billion by 2013. The stock is still down more than 70 percent from its 2010 peak.

“The acquisition of Equinox might have been if not the worst, one of the five worst acquisitions in history,” Thornton said at the internal meeting, a transcript of which was posted on the company’s website. And yet, forming a copper company out of Barrick’s assets, might make sense -- especially with Chinese partnership -- given copper is valuable and often found alongside gold, he said.

Barrick owns half of the Zaldivar copper mine in Chile and Jabal Sayid copper asset in Saudi Arabia, as well as Lumwana in Zambia. Its Chinese partnerships include joint ventures with Shandong Gold Mining Co. and Zijin Mining Group Co.

In a wide-ranging discussion, Thornton outlined his broader long-term strategy for Barrick to employees who, under a sweeping share-ownership plan, are also investors.

The plan includes increasing its portfolio of so-called tier 1 assets over time, and gradually shedding anything that’s not tier 1 or deemed to be “strategic.” The former Goldman Sachs Group Inc. executive defined tier 1 assets as mines that can produce at least 500,000 ounces of gold a year, have a mine life of more than 10 years, and are in the best half of the cost curve.

Tier 1 Gold

“It turns out that there are only 10 to 15 in the world. Now Barrick happens to have, let’s say, four of them. No other company has more than two,” Thornton told employees. “Obviously, if you have six it’s better, if you have eight it’s better, if you have 10 it’s better.”

Roughly half of the world’s tier-one assets are in “challenging” jurisdictions, meaning the Toronto-based company must be able to operate successfully anywhere. “It’s not an option simply to say ‘we’re only going to be in Nevada,’” although that might make sense at a “particular point in time.”

Assets that currently don’t meet tier 1 criteria are: Lagunas Norte in Peru, Canada’s Hemlo, a 47.5 percent share of the Porgera mine in Papua New Guinea, a 50 percent stake in Kalgoorlie in Australia, and Golden Sunlight in Montana, Barrick spokesman Andy Lloyd said by phone after Thornton’s comments were released.

When to Sell

The difficult question, Thornton said, is determining when to sell. In the case of Hemlo, for example, the asset is interesting right now because it’s Canadian and the company has tax losses in the country that it can use. But for it, and other non-tier 1 assets, “the likelihood of us continuing to own those over time is zero. We may own them for a period of time, for a variety of different reasons.”

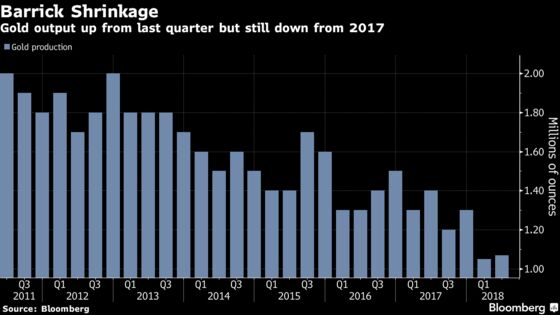

Barrick’s stock surged in late 2015 and early 2016 as the company sold non-core assets and slashed debt, but has since lost more than half its value. It’s the worst performer on the Bloomberg Global Senior Gold Valuation Peers index in the past month with a 19 percent slump, and the second worst in the past year. Much of the concern in markets is around the miner’s stagnant production pipeline.

Thornton has made no apologies for a focus on generating strong free-cash flow over growth for growth’s sake. Instead, the company has sought to reassure markets with guidance showing output will be stable above 4 million ounces until at least 2027, and has highlighted prospects for internal production.

Rich Mines

The company will be as disciplined in making acquisitions as it was divesting assets, Thornton said, and that means it will not be buying Detour Gold Corp. Barrick was recently said to be the undisclosed gold miner cited by Paulson & Co. as interested in potentially buying Detour. It doesn’t meet the three criteria to be a tier 1 mine, Thornton said, “so guess what the answer is as to whether we are going to buy it. The answer is no.”

Within its current portfolio, only Goldstrike, Cortez and Pueblo Viejo would currently qualify as tier 1, while majority-owned Turquoise Ridge would be considered an emerging tier 1 asset, Lloyd said. All of those mines are in Nevada except for Pueblo Viejo, which is in the Dominican Republic.

Joint Ventures

Argentina’s Veladero is a strategic asset that is close to being tier 1, Thornton said. Thornton has previously said investment in various technologies, including cyanide-free leaching, may speed development of the El Indio belt, where Veladero is located and which includes the Lama deposit in Argentina. Shandong is Barrick’s partner at Veladero; it’s currently looking at Lama to see if Veladero can be extended into a larger mine nearby, Thornton said.

Thornton stopped short of naming a successor to Barrick’s president, Kelvin Dushnisky, who will leave to helm AngloGold Ashanti Ltd. next month. But he stressed the company will be in good hands under three key executives: Chief Financial Officer Catherine Raw, Chief Investment Officer Mark Hill and Senior Vice President operational and technical excellence Greg Walker, who also holds the responsibilities of chief operating officer.

For the time being, the company plans to reinvest rather than buy back expensive debt, he said. Until the portfolio is generating more cash, Thornton said his “fantasy” of increasing the dividend annually will remain on hold.

To contact the reporter on this story: Danielle Bochove in Toronto at dbochove1@bloomberg.net

To contact the editors responsible for this story: James Attwood at jattwood3@bloomberg.net, Steven Frank

©2018 Bloomberg L.P.