China's Rising Defaults Bring More Safeguards to Yuan Bonds

China has been encouraging a market-driven approach to the pricing of risk in its bond market.

(Bloomberg) -- A record pace of defaults in China has triggered greater application of safeguards to local bonds, a silver lining for investors looking for some protection.

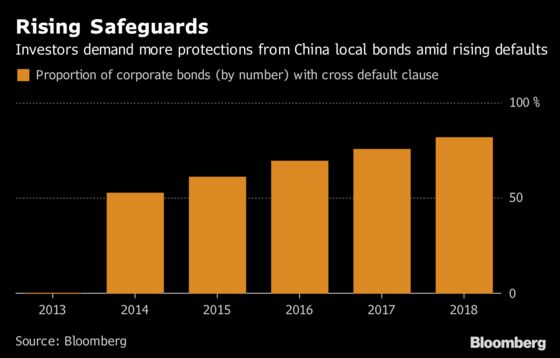

The ratio of domestic bonds with a cross-default covenant, which puts a borrower in default of other debt if it fails payment on one bond, has surged to 82 percent of all company notes sold this year. That’s up from almost zero five years ago. China has been encouraging a market-driven approach to the pricing of risk in its bond market -- the world’s third largest -- and inclusion of the provisions bring onshore practices closer to international ones.

“The proliferation of cross-default clauses is in line with investors’ increasing awareness of credit risk in recent years,” said James Hu, a senior portfolio manager at Income Partners Asset Management (HK) Ltd. “As the onshore bond market opens to foreign investors, the market practice becomes more internationalized and matured.”

Bonds sold offshore typically come with safeguards or covenants that protect investor interest by limiting the amount of debt a firm is allowed to borrow, potentially curbing losses. Over the past few years, more yuan corporate-bond issuers have added debt covenants, but it’s the cross-default clause that’s seen the highest adoption rate. About half of the local company bonds sold this year contain debt provisions, Bloomberg-compiled data show.

READ: China Onshore Corporate-Bond Defaults Reach 22.2 Billion Yuan

A recent example of such a clause being activated was the case of Wintime Energy Co. Its default on a 1.5 billion yuan ($225 million) bond on July 5 triggered cross-default on 13 of its bonds, totaling 9.9 billion yuan, according to a public filing. Last year, missed payments by companies such as Dalian Machinery Tools Group Corp. and Yiyang Group Holdings prompted defaults on their other debt.

Here are some perspectives on bond protections in China:

Ivan Chung, head of greater China credit research in Hong Kong at Moody’s Investors Service:

- The cross default clause puts bond investors on equal footing with other creditors in taking actions against issuers.

- The provision can also “aggravate the financial plight and bankruptcy risk of the defaulted issuers, as one default will trigger early repayment of all debt obligations with this clause”

- The contagion impact on related companies will be much larger through cross-default clause, including those that financially stronger and have little debt due in the short term

Cary Yeung, Hong Kong-based head of greater China debt at Pictet Asset Management:

- The increasing use of cross-default clauses will bring “more participation from foreign investors in the long run.”

Edmund Goh, Asia fixed-income investment manager at Aberdeen Standard Investments in Singapore:

- It’s particularly advantageous when the cross-default clauses are attached to onshore bonds issued by the corporate entity that holds the group’s core assets.

--With assistance from Yuling Yang.

To contact the reporter on this story: Lianting Tu in Hong Kong at ltu4@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Christopher Anstey

©2018 Bloomberg L.P.