China's Junk-Rated Bond Issuers Are Finding a Haven in Loans

China's Junk-Rated Bond Issuers Are Finding a Haven in Loans

(Bloomberg) -- With the Federal Reserve driving up dollar borrowing costs and China’s deleveraging campaign stoking fears of default among fixed-income investors, Chinese debtors are increasingly turning to the loan market for funding.

Chinese companies have some $76 billion of dollar bonds to repay in the coming year, and face the both higher yields and a weaker exchange rate, thanks in part to U.S.-China trade tensions that brought an end to five straight quarters of gains for the yuan. High-yield issuers are especially vulnerable, with authorities recently looking at cracking down on a loophole that let them sell dollar debt with less than one-year maturity without pre-approval.

Credit Agricole Corporate & Investment Bank expects more issuers with so-called crossover ratings, or those with credit ratings split between investment grade and junk, to tap the syndicated loan market, due to rising interest rates and the lengthy process of getting the regulatory approvals for bond sales.

"Liquidity from syndicated loans would favor cross-over or lower-investment-grade credits, while high-yield issuers who come with 364-day bonds are not mainly target client for syndicated loan markets," said Lei Fang, Hong Kong-based managing director of Asia Pacific debt origination and advisory at Credit Agricole.

With Chinese dollar-bond yields now around the highest since February 2015, according to an ICE BofAML index, high-yield Chinese property developers are among those lining up for loans:

- China Jinmao Holdings Group Ltd. which was absent from the loan market for three years, recently raised HK$8 billion ($1 billion).

- Greentown China Holdings Ltd. tapped the loan market twice this month to raise a total of $1.4 billion after a year’s absence.

- Powerlong Real Estate Holdings Ltd., this week raised a 3.5 year loan at a margin of 340 basis points over Libor, which is about 60 basis points tighter than what it paid for a shorter-tenor loan in 2016. It was also lower than the the 6.95 percent coupon it pays for a three-year bond sold in April.

- China Aoyuan Property Group and CIFI Holdings were other Chinese property developers who raised cheaper loans recently.

It’s not just the property developers who are cashing in. China Jinjiang Environment Holding Co., a waste-management company, raised a $216 million three-year loan last month which pays an all-in cost of as much as 473 basis points. The company sold a similar-sized bond last year at a coupon of 6 percent.

“There are a lot of borrowers who might have gone to the bond market three or six months ago that will be looking much more seriously at the loan market in the second half,” said John Corrin, global head of loan syndications at Australia and New Zealand Banking Group in Hong Kong.

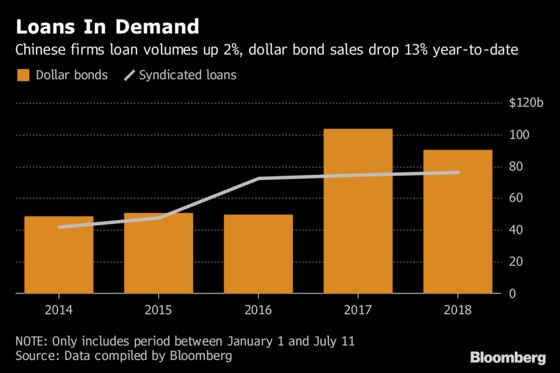

Syndicated-loan volumes from Chinese borrowers are on the rise, while U.S. dollar bond sales from junk-rated issuers are 13 percent lower than the same period last year, Bloomberg-compiled data show. Forty percent of the banks operating in Asia Pacific surveyed by Bloomberg News last month predicted interest margins and fees on syndicated loans to fall in the second half of the year.

“Bond investors tend to be more risk-averse on the back of defaults in the credit market,” said Lewis Wong, the Hong Kong-based head of North Asia, APAC Financing Group at Credit Suisse Group AG. Not all boats will get a lifeline, however. “Liquidity from banks is typically more stable for corporate borrowers who have established long-term relationships with lenders,” Wong said.

To contact the reporters on this story: Annie Lee in Hong Kong at olee42@bloomberg.net;Carol Zhong in Hong Kong at yzhong71@bloomberg.net;Mariko Ishikawa in Sydney at mishikawa9@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, ;Andrew Monahan at amonahan@bloomberg.net, Christopher Anstey

©2018 Bloomberg L.P.