Global Markets Are Shaking Off China’s Flashback to 2015

Investors are having flashbacks to 2015-16 amid fears over China’s industrial complex amidst global trade war.

(Bloomberg) -- It’s going to take more than a dose of yuan weakness and softer metal prices to wreak havoc on global markets this time around.

Investors are having flashbacks to 2015-16 amid fears over China’s industrial complex while the nation gets dragged into a trade war. But markets are unlikely to be revisited by the deflationary monster of years past.

From a solid U.S. manufacturing trajectory to a resilient credit cycle, here’s why.

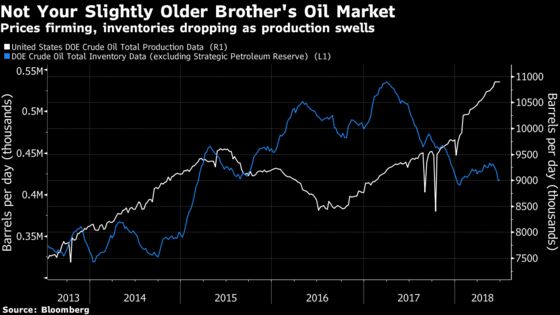

Oil’s Well That Ends Well

For one, crude prices are on a tear compared to three years ago, juicing commodity-linked assets and sending benign signals about the global growth cycle.

In 2015, producers reticent to address a supply glut kept crude depressed. Today, the shoe is on the other foot, with stockpile drawdowns and rising prices despite ever-increasing domestic production.

Firm oil prices are here to stay, according to Bank of America Corp., which projects the market will remain in structural deficit for most of the next six quarters.

In turn, oil’s rise is buoying junk bonds, an asset class dubbed the canary in the coal mine for the U.S. business cycle. The iShares iBoxx High Yield Corporate Bond ETF is in the green this year -- in 2015, it gave back 5 percent.

The “chances of a credit cycle playing out are lower today than immediately after the meltdown in energy/commodities/EM and going into Brexit uncertainty in the middle of 2016,” BofA strategists wrote in a note.

And the resilience in high-yield credit is broad-based: premiums have tightened across a slew of sectors so far this year, in contrast to spiking spreads in 2015.

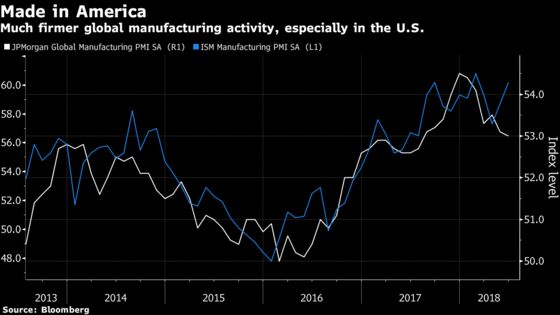

While global growth may have come off the boil, manufacturing sectors around the world -- particularly the U.S. -- are on a much firmer footing. Monthly purchasing managers’ indexes point to a solid expansion in factory activity, while in early 2016, the global gauge bottomed at 50, implying stagnation.

Meanwhile, the bar for China to export disinflation via currency depreciation has also been raised, according to Neil Dutta, head of U.S. economics at Renaissance Macro Research.

“In the second half of 2015, core PCE inflation ran just 1.3 percent annualized,” he said. “It is north of 2 percent on a six month basis now, which implies there is some room to deal with the deflationary consequences of a strengthening in the U.S. dollar.”

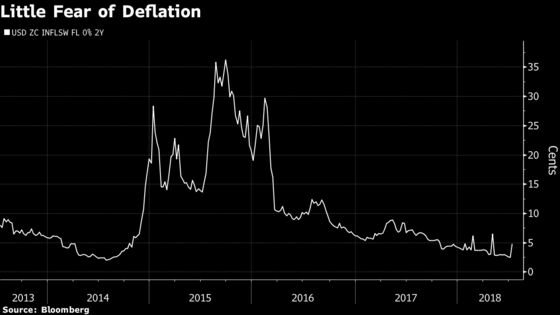

And investors are sanguine.

The low cost of options that pay out should the Consumer Price Index average an annual rise of less than zero over the next two years shows just how different the domestic backdrop is compared to 2015.

Stemming the Outflows

The Made in China risk shouldn’t be overstated, either.

In early 2016, fears over the country’s financial stability took center stage amid accelerating outflows and rampant expectations for continued currency depreciation while corporates scrambled to cover mismatches between their assets and liabilities. That same dynamic has yet to rear its head.

“The real capital outflows are manageable as the RMB depreciation expectation remains largely stable,” said Macquarie strategist Teresa Lam in a note. “This should ease the market‘s worry that the weakness of RMB was triggered by significant portfolio outflows.”

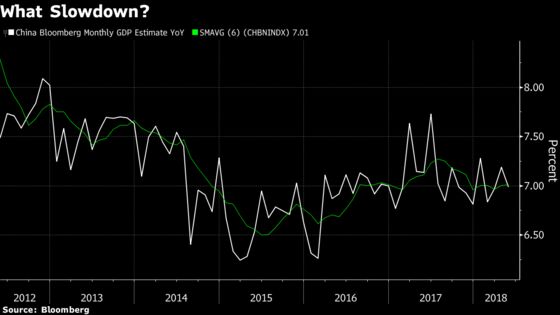

In addition, investors have reason to downplay tentative signs of a cooling in Chinese growth, chalking it up to seasonal factors and delays on big-ticket purchases ahead of cuts to levies on imported vehicles.

The six-month moving average of Bloomberg’s estimate for annual expansion sits at 7 percent in May -- a half a percentage point better than it was ahead of the August 2015 shock devaluation of the yuan.

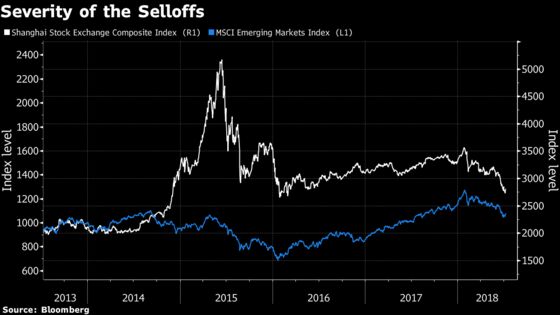

For a true repeat of 2015, the carnage in Chinese and emerging market equities will need to intensify.

Back then, the Shanghai Composite ultimately fell 50 percent from peak to intermediate trough. Roughly five and a half months removed from its recent high, the index is down 21 percent. Likewise, the MSCI Emerging Market Index has suffered a less-punitive drawdown.

America First

The U.S. equity resilience is even more striking.

The S&P 500 Index is 2.8 percent away from its all-time high, and up almost 5 percent since the dollar began to rise against the yuan in mid-April. In August 2015, the benchmark U.S. stock gauge abruptly fell 10 percent as markets reacted to China’s currency surprise.

The earnings trend is helping to fortify investors’ resolve that American companies are better able to withstand exogenous shocks compared with three years ago.

Still, in case you need reminding: one potentially massive risk absent in 2015 threatens to shake the firmament of global markets.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Sid Verma, Cecile Gutscher

©2018 Bloomberg L.P.