China Considers Banning Short-Term Dollar Bond Sales

Selling bonds that mature in 364 days has become a popular tactic among Chinese real estate players.

(Bloomberg) -- China is slowing approvals for offshore bonds and considering whether to ban short-dated issuance in dollars, according to people familiar with the matter, moves that would reduce financing options for the debt-laden developers that sit at the center of the nation’s economy.

The National Development & Reform Commission is weighing a ban on the sale of dollar bonds with tenors of less than one year, said the people, who asked not to be named because they’re not authorized to speak publicly. The regulator is already restricting offshore issuance quotas for Chinese companies, people said.

The new measures threaten to further constrain cash-strapped property developers even as concerns about China’s financial risks ripple across markets. And it’s not just funding problems that are plaguing the industry: this week, the housing ministry escalated a crackdown on property speculation, while the nation’s policy banks tightened approvals on new lending for shanty-town redevelopment projects.

Selling bonds that mature in 364 days had become a popular financing tactic because it didn’t require pre-approval from the NDRC. The regulator has publicly signaled that it’s wary of the offshore issuance boom, saying in a Wednesday statement that developers are only allowed to use proceeds to refinance existing debt, that some companies are borrowing amounts that are out of proportion with their profits, and that many don’t have foreign-currency revenues to protect themselves against the yuan’s slide.

“I find this an understandable move, however issuers will unlikely be happy," said Scott Bennett, Hong Kong-based executive director of fixed income at Oppenheimer Investment Asia Ltd. “It could be negative in the short-term for weaker Chinese property developers as this removes one source of refinancing and may potentially lead to defaults."

The NDRC, which regulates foreign debt sales by companies, didn’t immediately respond to a faxed message seeking comment. Calls went unanswered.

In the regulator’s Wednesday statement, it said that the use of proceeds from builders’ overseas bond sales must be limited to just refinancing, instead of investing in domestic property projects and replenishing working capital. “Some of the issuers have low profits, which don’t match the amount of foreign debt they are raising,” the NDRC said, referring to developers and to local government financing vehicles.

“Weaker developers may get hit more due to the restrictions from the regulators, but this is how the bond market should be,” said Anne Zhang, executive director for fixed income, currencies and commodities at JPMorgan Private Bank in Asia. She expects that some may need to tap the collateralized loan market, or sell assets to repay their debt.

Stocks, Bonds

While the move will be good for the market over a longer term because it’ll filter out riskier issuers, “turmoil awaits" as companies with near-term debt maturities scramble to make ends meet, CITIC CLSA Securities analysts wrote in a note.

Real estate stocks and bonds were under pressure Thursday.

Most Chinese property dollar bonds fell, with China Evergrande Group and Logan Property Holdings leading the losses, according to ICE BofAML index. In the past two years, Chinese developers have sold about $10 billion of dollar notes that mature in less than a year, Bloomberg-compiled data show.

An index of shares in 22 Chinese developers has tumbled 12.5 percent since Monday as investors have grown increasingly nervous about the outlook for the sector. The gauge fell for a fourth straight day on Thursday, with Longfor Properties Co. and Shimao Property Holdings Ltd. the biggest decliners, sinking 4.73 percent and 4.75 percent respectively on Thursday.

The NDRC is trying to control offshore issuance by weaker and less competitive developers who may be over-relying on offshore capital markets, said Christopher Yip, an analyst at S&P Global Ratings in Hong Kong.

Yuan Risks

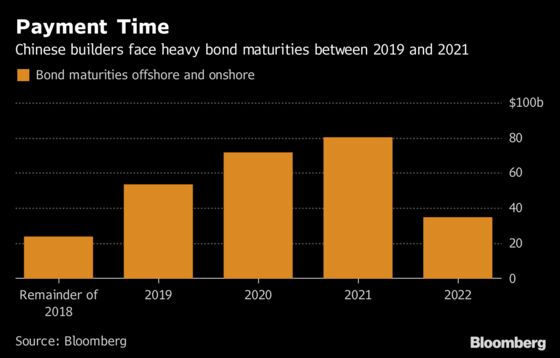

Chinese builders, faced with bond payments of $77.4 billion in the domestic and overseas markets through 2019, have been reeling from tightened liquidity at home induced by a clampdown on shadow financing. That’s prompted them to sell debt in the offshore market, with dollar bond sales reaching a record $27.5 billion this year.

While the NDRC’s latest moves would limit their use of that offshore funding venue, they could also shield issuers from an increase in debt-servicing costs if the yuan keeps falling. China’s currency is down more than 3 percent against the greenback in the past two weeks.

The latest developments are positive for the medium term stability of the industry, according to Charles Macgregor, head of Asia markets at Lucror Analytics in Singapore. "We do not see this as a likely stimulus for defaults – that is not in the interests of the NDRC," he said.

“My view would be that that is just to limit the currency risks that exist. We’ve seen many periods of history that it’s dangerous to borrow too much in a foreign currency because not only do you have interest rate costs but also FX risks,” said Nicholas Wall, London-based fixed income portfolio manager at Old Mutual Global Investors in Hong Kong. Dollar appreciation “could increase risks for sectors that are tremendously important for China and Chinese growth,” he said.

--With assistance from Yuling Yang and Emma Dong.

To contact Bloomberg News staff for this story: Carrie Hong in Hong Kong at chong61@bloomberg.net;Lianting Tu in Hong Kong at ltu4@bloomberg.net;Steven Yang in Beijing at kyang74@bloomberg.net;Narae Kim in Hong Kong at nkim132@bloomberg.net;Annie Lee in Hong Kong at olee42@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Chan Tien Hin, Sarah McDonald

©2018 Bloomberg L.P.

With assistance from Editorial Board