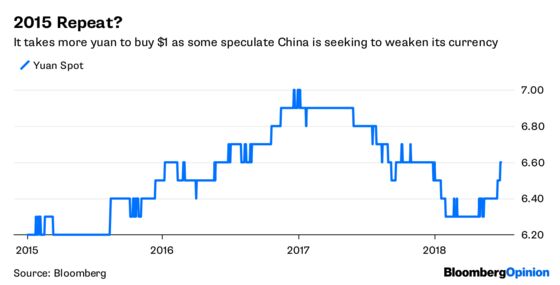

(Bloomberg Opinion) -- What's going on in China's markets? Two theories have emerged to explain the big drop in the country's currency, the yuan, in recent weeks. The straightforward interpretation is that it’s a sign markets don't believe China can win a trade war with the U.S. Another explanation is that China has decided to use the yuan as a policy tool, allowing it to depreciate to cushion exporters against any U.S. tariffs.

Whatever side you come down on, it's hard not to be just a little anxious about what this means for financial markets. China's surprise decision in August 2015 to undertake a small devaluation of the tightly controlled yuan sparked a global sell-off in stocks that lasted for six months and pushed the MSCI All-Country World Index down by 16 percent. If China is, in fact, using the yuan as a weapon in its trade dispute with the U.S., it’s playing a dangerous game as the currency's drop could easily spark a mass exodus of capital out of the country that it can't easily stem. Be that as it may, the theory that China has weaponized the yuan is possible, or at least — as Credit Suisse's foreign-exchange strategists described it — plausible. The strategists at Brown Brothers Harriman say that rather than representing a referendum on China's position in the trade dispute, the drop in the yuan "is more consistent with a short-term squeeze rather than a structural shift" given that implied volatility over the short term is higher than it is over the long term. Also, the spread between one-month and 12-month yuan non-deliverables isn’t suggesting a bearish outlook.

Notably, the recent bout of yuan weakness follows a prolonged period of gains that perhaps made it too strong. "I see this more as a right-sizing of what arguably was an overshoot," Robin Brooks, the chief economist at the Institute of International Finance and the former chief currency strategist at Goldman Sachs group Inc., tweeted on Wednesday. Based on real effective exchange rates, Brooks figures that the yuan "is pretty much the only major currency that has risen" this year against the dollar, adding that the currencies of Taiwan, South Korea, Singapore and Thailand have all fallen.

BANK SELL-OFF ADDS TO JITTERS

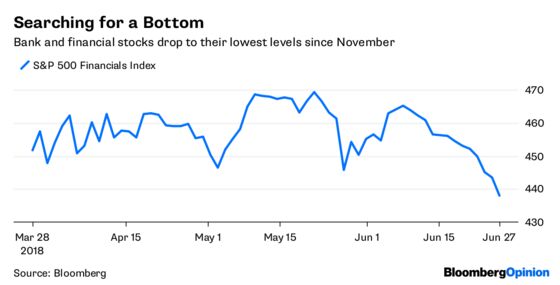

There's plenty to keep investors on edge these days. If they weren't talking about China's markets, then they were likely talking about bank and financial stocks. The widely-followed $30 billion Financial Select Sector SPDR Fund has fallen for a record 13 straight days, dropping 6.13 percent. The thinking is that a trade war will slow the economy and cause the yield curve — or difference between short- and long-term bond yields — to shrink. That's key because financial institutions make their money by borrowing at low, short-term rates and lending at higher, long-term rates. As that difference narrows, so do bank net interest margins, and right now the yield curve is the flattest since 2007. It's not only U.S. bank shares that are suffering: It's a global phenomenon. So, it's not hard to understand why investors see financials as the canary in the global economic coalmine. The good news is that banks are likely to be able to weather any downturn much better than the last recession and financial crisis. Federal Reserve data show that banks have surplus liquidity, which is basically their deposits minus the loans they have made, of $2.84 trillion, up from less than $200 billion in 2008. Also, a gauge of where traders expect bank borrowing costs will be in the months ahead, the so-called FRA/OIS spread, stands at about 35 basis points, down from the high this year of 55 basis points in March.

BONDS STAGE A COMEBACK

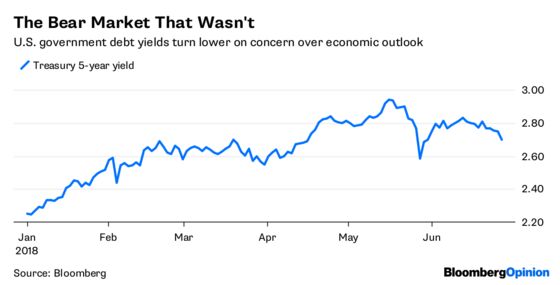

All these jitters over China and bank stocks are proving beneficial to Treasuries. U.S. five-year notes rallied for a third consecutive day as the government's monthly auction of $36 billion of similar-maturity debt drew the most demand since August. Investors bid for 2.55 times the amount offered, up from 2.52 times at last month's sale. The rally puts the government bond market in a position to post its first back-to-back monthly gains since last July and August, based on the Bloomberg Barclays U.S. Treasury Index. For all the talk at the start of the year about a nasty bear market in bonds looming on the horizon, 2018 is shaping up as rather benign. That could be because breakeven rates on five-year Treasuries, or what traders expect the rate of inflation to be over the life of the securities, have stopped moving higher. They were at 2.70 percent on Wednesday, down from the high this year of 2.94 percent in mid-May. And while some real-time measures of the economy suggest gross domestic product may be expanding at about a 4 percent annualized rate this quarter, the consensus is for a slowdown in the second half of 2018 and into 2019, due in part to concern that the Trump administration's protectionist policies may cause companies to become more conservative in their business planning. Orders placed with factories for business equipment cooled unexpectedly in May after an upwardly revised April jump that was the largest this year, Commerce Department figures showed Wednesday.

OIL PRICES TAKE FLIGHT

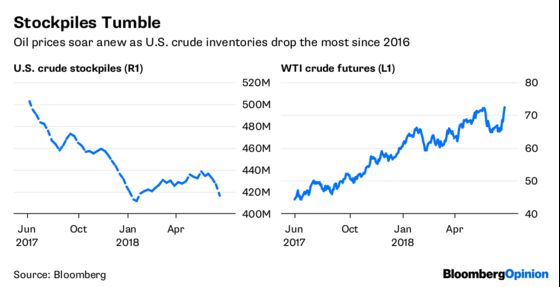

Last week, Trump criticized the Organization of Petroleum Exporting Countries for inflating the cost of oil. “Hope OPEC will increase output substantially,” Trump said on Twitter after a meeting between OPEC and its allies ended Friday. “Need to keep prices down!” Maybe he should have saved his criticism for U.S. producers. Oil prices surged as much as 3.4 percent in New York Wednesday to the highest since 2014 after the Energy Information Administration said U.S. crude stockpiles tumbled by the most since September 2016. Domestic crude inventories declined by 9.89 million barrels last week, according to Bloomberg News's Jessica Summers. West Texas Intermediate crude for August delivery climbed $2.42 to $72.99 at one point on the New York Mercantile Exchange. The price of a gallon of regular-grade gasoline in the U.S averages $2.848, up from 2.254 a year ago, according to the Automobile Association of America. Oil prices already were elevated as the Trump administration sought to dissuade purchases of oil from Iran, OPEC’s third-largest crude producer. The efforts to isolate and hobble the Islamic Republic overshadowed Saudi Arabia’s plan to lift oil output to a record within weeks. OPEC agreed on a “nominal” production increase of 1 million barrels a day, Saudi Energy Minister Khalid Al-Falih told reporters in Vienna on Friday. In reality, several ministers said the accord will add a smaller amount to the market — about 700,000 barrels a day — because a number of countries are unable to raise their output.

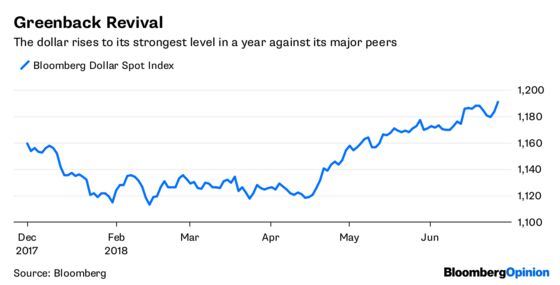

TRUMP IS DEVELOPING A DOLLAR PROBLEM

The Bloomberg Dollar Spot Index was poised for one of its biggest gains of the year on Wednesday, rising as much as 0.7 percent. That put the gauge on track to close at its highest level since early last July. A strong dollar is coming at an inopportune time for the Trump administration, which is threatening reciprocal tariffs on many of its trading partners if they don't agree to new trade deals. The rising dollar only makes U.S. goods more expensive to foreign purchasers, while making foreign goods less expensive for U.S. buyers. But rather than a reflection of investor confidence in the U.S., the foreign-exchange strategists at Bank of America Merrill Lynch figure the dollar's appreciation since mid-April is due more to weaker economic data outside the U.S., especially the euro zone, which have weighed on both developed- and emerging-market currencies. Starting in April, Citigroup Inc. indexes show that the global economic data was largely falling short of forecasts, after exceeding estimates in the prior eight months. Some strategists figure that the dollar has topped, and will weaken in the second half of the year. "There are signs the dollar rally is running out of steam,” Van Luu, the head of currency and fixed-income strategy at Russell Investments, wrote in a research note. The greenback is now “expensive” and “overvalued,” based on purchasing power parity versus the euro, yen and British pound, according to Luu.

TEA LEAVES

Italy has delivered more than its share of jitters to global markets after forming a government that’s skeptical of the nation’s need to still be part of the euro zone, and which has pledged to boost spending. As a result, Italy's equities have underperformed as the yields on its bonds have shot higher, almost doubling at one point. Now, a big test of investor confidence will take place Thursday, when Italy auctions 3.5 billion euros ($4.1 billion) to 4.5 billion euros of five- and 10-year notes. One thing Italy will have going for it is the relatively small sizes of the auctions, according to Bloomberg News's John Ainger. “A strong 10-year auction would be a positive development for Italy in the short term,” Antoine Bouvet, a rates strategist at Mizuho International Plc, told Bloomberg News. ING Groep NV strategist Martin van Vliet added that the bond dealers handling the auctions will likely ensure that demand is high.

DON'T MISS

Why Russia and Turkey Are Such Gold Bugs: Leonid Bershidsky

Cryptocurrency Universe Expands Far Beyond Bitcoin: Aaron Brown

Trump Lights a Fire Under Oil the Saudis Can't Douse: Julian Lee

Banks Are Wrong Villains for Liquidity Fear: Brian Chappatta

Investors, Not Banks, Could Spark the Next Crisis: Satyajit Das

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.