China Banks' Waning Demand Hints at More Bond Defaults Ahead

China Banks' Waning Demand Hints at More Bond Defaults Ahead

(Bloomberg) -- China’s banks, scrambling to adjust to the government’s deleveraging campaign, are likely to add to pressures on the corporate bond market as they shed more of their massive note holdings and de-risk their balance sheets.

Further payment problems are likely in a market that has already seen at least 14 corporate bond defaults this year, according to Logan Wright, Hong Kong-based director at research firm Rhodium Group LLC. As well as cutting their own holdings, Chinese banks have pulled back from lending to other firms that use the funds to buy bonds, exacerbating the pressure on the market.

"You have seen banks redeeming funds placed with non-bank financial institutions that have reduced the pool of funds available for corporate bond investment overall," said Wright, who has covered China since 2006. He said the additional bond defaults are especially likely among those property developers and local-government financing vehicles which have relied on shadow banking vehicles for their funding.

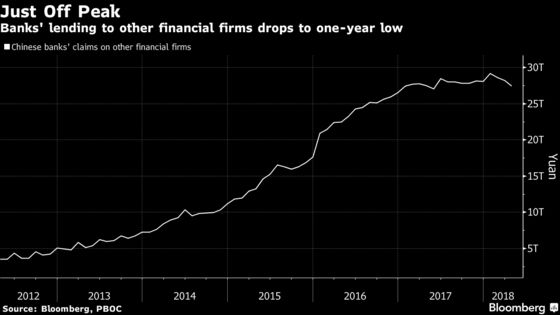

Strains have already spread from high-yield trust products to corporate bonds this year as China’s campaign against its $10 trillion shadow banking industry has choked off refinancing for the weaker borrowers. Banks’ lending to other financial firms, a common route for funds and securities brokers to add leverage for corporate bond investments, declined for three straight months, or a total of 1.7 trillion yuan ($265 billion), since January.

The shadow banking campaign and tighter credit conditions are also forcing banks to buy fewer corporate bonds, said Jason Bedford, a Hong Kong-based analyst at UBS Group AG. That is eroding a key prop for the bond market.

“Unlike the U.S., where the majority of buyers of bonds are mutual funds, individuals and investment companies, in China, the key holders of bonds are bank on-and off-balance sheet positions,” said Bedford.

China’s four largest banks held about 4.1 trillion of bonds issued by companies and other financial institutions at the end of 2017, nearly 20 percent below 5.1 trillion yuan a year earlier, according to their annual reports. All Chinese banks held about 12 trillion yuan of corporate bonds on or off their balances sheets, some 70 percent of outstanding issuance, according to Citic Securities.

Chinese companies must repay a total of 2.7 trillion yuan of bonds in the onshore and offshore market in the second half of this year, and together with another 3.3 trillion yuan of trust products set to mature in the second half, the problems may get worse. More than eight high-yield trust products have delayed payments so far this year.

PBOC Move

The central bank moved on Friday to address some of the funding problems of smaller Chinese firms, announcing plans to add lower-rated corporate bonds into the collateral pool for its medium-term lending operations. The change will make it easier for smaller banks to apply for central bank funding and increases incentives for small company lending, according to Guosen Securities Co.

Banking shares rose on Monday with Industrial & Commercial Bank of China Ltd. gaining as much as 1.5 percent in Hong Kong, while China Merchants Bank Co. jumped 2.2 percent.

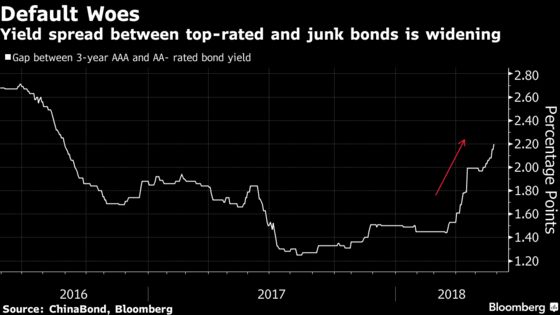

In an indication of the recent pressures on weaker firms, the yield premium of three-year AA- rated bonds over similar-maturity AAA notes has widened 72 basis points since March to 225 basis points, the highest level since August 2016, according to Chinabond data.

"It’s obvious that we’ve seen a huge contraction in overall credit availability and that’s going to leave some companies more vulnerable to refinancing needs," Wright said.

--With assistance from Judy Chen.

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Alfred Liu in Hong Kong at aliu226@bloomberg.net

To contact the editors responsible for this story: Marcus Wright at mwright115@bloomberg.net, Neha D'silva

©2018 Bloomberg L.P.

With assistance from Editorial Board