The $457 Billion Reason for China to Cut Reserve Ratio Again

PBOC may cut Reserve Requirement Ratio to hand lenders liquidity so they can pay back the debt.

(Bloomberg) -- The case for the People’s Bank of China to cut the amount of cash lenders are required to hold is getting stronger.

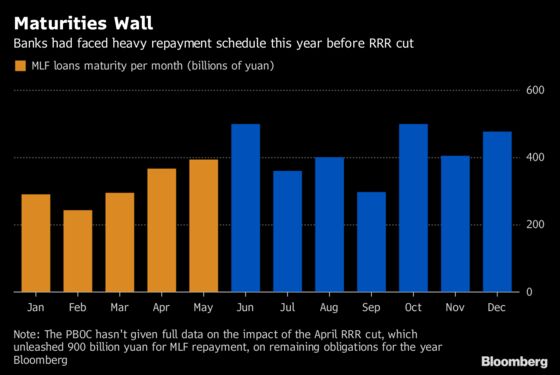

Chinese banks racked up 2.93 trillion yuan ($457 billion) in medium-term loans extended by the PBOC scheduled for repayment during the rest of 2018. That has prompted some analysts to raise bets the PBOC may soon repeat a tactic used in April: cutting the Reserve Requirement Ratio to hand lenders liquidity so they can pay back the debt.

Even though the one-percentage-point cut in April has already eased part of that repayment burden, more than 80 percent of the original MLF funds are still outstanding -- and other pressures make the matter urgent. Lenders also need to hoard cash for upcoming quarterly regulatory checks, pay back the 2.3 trillion yuan of short-term interbank debt that Bloomberg calculations show is due in June, and put aside cash for the tax season in July.

Such a move would help mitigate concerns of a cash crunch, which could disrupt China’s financial markets and even trigger systemic risks. In effect, a reduction would also boost banks’ ability to lend to smaller and private companies, which have seen a string of defaults of late as an official deleveraging drive squeezes out shadow financing.

At 16 percent for most banks, China has an unusually high RRR -- stemming from the need to mop up years of capital inflows -- and can therefore release funds to the system by reducing it without endangering financial stability.

Time Ripe

"The time will be ripe for China to cut RRR again in July," said Ding Shuang, chief China economist at Standard Chartered Plc in Hong Kong, who cited the tax repayment as a strong factor. "The policy makers need to ease banks’ pressures and also encourage them to extend loans to small and medium-sized firms."

The PBOC will lower the RRR by as much as two percentage points in addition to the previous reduction by end-2018 to swap out maturing MLFs, UBS AG economists led by Ning Zhang wrote in a note this month. There is a big chance that the next cut would come in June or July, when onshore liquidity tightens for seasonal factors, said Qin Han, chief bond analyst at Guotai Junan Securities Co. in Shanghai.

State-run media also backed up the argument for an imminent cut. The banking sector will see “a hole” in liquidity over the next two months, according to a front-page commentary in China Securities Journal this week.

Some traders are already buying bonds on bets the PBOC may cut the RRR in the near future, StanChart’s Ding said. China’s government bonds have rallied since mid-May, with the benchmark 10-year yield sliding 9 basis points from a peak this month to 3.63 percent on Thursday. The sovereign notes had their best week in more than three years when the PBOC acted in April.

Favorable Tool

An RRR cut is more favorable than rolling over MLF loans, as the extra funding can go to smaller banks, which are more likely to lend to cash-strapped private firms, said Tommy Xie, an economist at Oversea-Chinese Banking Corp. in Singapore. MLF financing is only extended to bigger lenders, he said.

PBOC Governor Yi Gang was the latest official to voice the need to support smaller borrowers, saying in a meeting Tuesday that China will "use all sorts of monetary tools in a flexible way" to make it easier and cheaper for such firms to get funding. For Dariusz Kowalczyk, senior emerging-market strategist at Credit Agricole SA, Yi’s remarks suggest the odds of an RRR cut in the coming weeks are on the rise.

To be sure, it’s unclear when the debt that banks used the funding released from the previous RRR cut to repay was originally planned to mature, so liquidity pressures can be smaller if the loans turn out to have been due in next few months. Also, weakness in the yuan, which sank to the lowest level in four months, could complicate officials’ decision as looser monetary conditions will likely result in further depreciation in the currency and trigger capital outflows.

"The policy makers’ primary considerations now are fund flows and liquidity conditions," said OCBC’s Xie. "Considering the yuan could stabilize soon and cash supply could tighten again, the window for an RRR cut is opening in the third quarter."

--With assistance from Yuling Yang and Xize Kang.

To contact Bloomberg News staff for this story: Tian Chen in Hong Kong at tchen259@bloomberg.net;Yinan Zhao in Beijing at yzhao300@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net;Richard Frost at rfrost4@bloomberg.net

©2018 Bloomberg L.P.

With assistance from Editorial Board