Shrinking Valuations Cast Shadow Over Smaller Chinese Bank IPOs

Shrinking Valuations Cast Shadow Over Smaller Chinese Bank IPOs

(Bloomberg) -- As China’s crackdown on shadow banking shrinks smaller banks’ valuations relative to larger peers, the outlook is dimming for the country’s regional lenders queuing up to list their shares.

Small bank shares have been slipping relative to China’s lending giants like Industrial & Commercial Bank of China Ltd. and Agricultural Bank of China Ltd. due to their deeper involvement in the shadow banking sector. That points to lower pricing prospects for the 18 or so rural and city commercial banks currently planning to sell new shares when compared with their 16 small bank peers which have listed since 2016.

“China’s banking landscape is increasingly tilted -- the strong get stronger, and the weak get weaker,” said Liao Chenkai, a Shanghai-based analyst at Capital Securities Co. “Small banks are the most hurt by the deleveraging campaign which has squeezed their margins and weakened their capital strength.”

Terry Sun, an analyst at RHB Securities Hong Kong Ltd., argues that China’s small banks are still overvalued, even after recent price declines, given the accelerating pace of the shadow banking crackdown on the mainland. Even after recent share price declines, for example, Guangzhou Rural Commercial Bank Co. and Zhongyuan Bank Co. are trading in Hong Kong at about 0.9 times their book value, near the level of ICBC and other large banks with a better profit outlook.

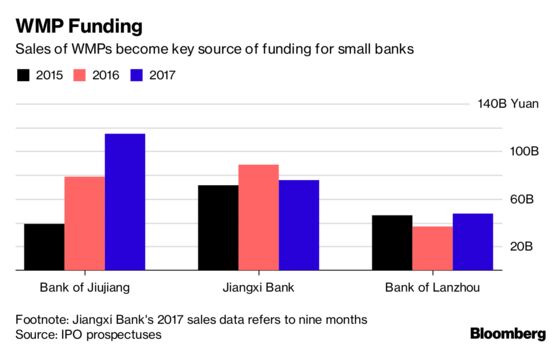

The deleveraging campaign which got underway in April last year has pushed up the small banks’ borrowing costs, weakened their profit growth and increased solvency risks. Many are vulnerable to the strict new regulations on the country’s 100 trillion yuan ($15.7 trillion) of asset management products, being phased in by the end of 2020. The rules include a ban on guaranteeing AMP returns, which is likely to shut off a key funding source for small banks.

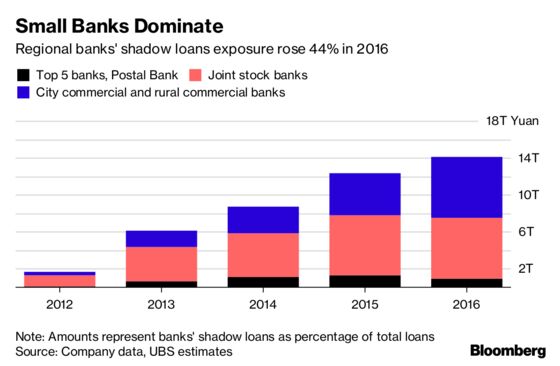

And the institutions have also relied on shadow banking to grow their assets. Jiangxi Bank Co. and Bank of Jiujiang Co., which have filed applications for initial public offerings in Hong Kong, had investment classified receivables -- mostly shadow loans -- amounting to about a quarter of total assets, according to their filings. At ICBC the proportion is only 1 percent.

Shares in the five biggest Chinese banks -- which control more than a third of China’s $40 trillion in banking assets -- got another boost this year from strong first quarter earnings, as economic recovery has improved their net interest margins and asset quality. Because of their greater reliance on shadow lending, the small banks have missed out.

“There are two re-rating drivers for China’s banking industry: NIM recovery and asset-quality improvement,” said Marco Yau, a senior analyst at CEB International Investment Corp. “Both of these have nothing to do with the small banks.”

As bad loan ratios at the big banks have come down, the small banks are moving in the opposite direction. City commercial banks’ bad loan ratios climbed to 1.53 percent at the end of March from 1.52 percent three months earlier, while the ratios at rural banks rose to 3.26 percent from 3.16 percent, according to regulatory data.

The shares of the six smaller Chinese banks which have listed in Hong Kong since the beginning of 2016 have dropped about 9 percent so far this year, compared with a 11 percent gain for China’s big five lenders, and a 3.8 percent rise in the benchmark Hang Seng Index.

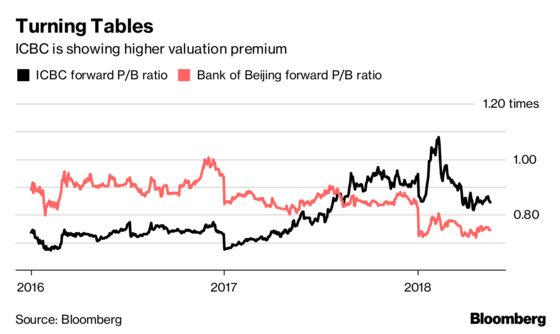

Price-to-book ratios are also moving in different directions. Bank of Beijing Co. lost its valuation premium to ICBC’s A-shares in August, with the larger bank currently trading at over 0.8 times forecast book value.

Bank of Zhengzhou Co. trades at 3.9 times earnings per share in Hong Kong, down about 38 percent from the peak since its 2015 listing, while ICBC’s P/E ratio of 6.8 times is more than 60 percent above its record low in 2016.

“Investors will remain lukewarm to the shares and upcoming IPOs of small lenders,” said Liao. “We haven’t seen any light at the end of the tunnel.”

To contact Bloomberg News staff for this story: Alfred Liu in Hong Kong at aliu226@bloomberg.net;Jun Luo in Shanghai at jluo6@bloomberg.net

To contact the editors responsible for this story: Marcus Wright at mwright115@bloomberg.net, Charlie Zhu

©2018 Bloomberg L.P.

With assistance from Editorial Board