With 75% of Emerging-Market Index, Asia Hit by Others’ Woes

Asia is bearing the burden of turmoil far from its shores.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- Asia is bearing the burden of turmoil far from its shores, thanks in part to benchmark indexes that leave the world’s fastest-growing region particularly exposed when investors opt to dump emerging markets as a class.

Its growth and market development mean Asia in some sense has become a victim of its success, dominating the broader emerging-asset universe, especially when it comes to equities. Deepening financial linkages between China and the rest of the world are also elevating the role of the world’s No. 2 economy.

“You can throw fundamentals out the window right now,” said Hayden Briscoe, head of fixed income for Asia-Pacific at UBS Asset Management in Hong Kong. Emerging markets have been trading as a bloc in recent weeks, irrespective of whether they have current account surpluses or deficits, he said. A “tipping point” is being reached where sell-offs abroad are now hitting Asia, he said.

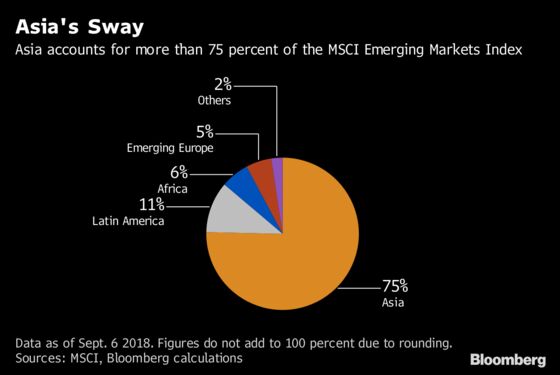

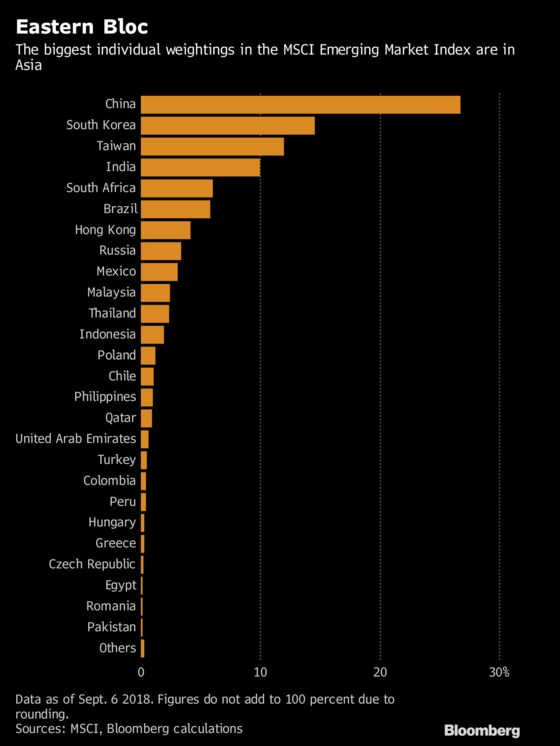

China, South Korea, Taiwan and India account for four of the five biggest weightings in MSCI Inc.’s Emerging Markets Index. Companies based in Asia account for around 75 percent of that gauge, and just shy of 70 percent of the equivalent FTSE benchmark, according to data compiled by Bloomberg. Both indexes are down a little more than 12 percent this year.

Bond Market

In fixed income, Asia doesn’t have quite the same presence as in stocks. The region accounts for just over 34 percent of the Bloomberg Barclays Emerging Market U.S. Dollar Aggregate Index, compared with a little below 30 percent for Latin America. Even so, Briscoe said at a briefing in Hong Kong Thursday that “we’re worried that equity markets are going to influence currencies, which will then impact credit securities as well.”

While the sell-off of emerging assets eased somewhat Thursday, prospects for further U.S. Federal Reserve policy tightening threaten to keep the pressure on. The MSCI Asia Pacific Index closed at its lowest in a year Tuesday, and is heading for its biggest weekly drop since March.

A slide in Chinese technology shares has played a big part in walloping Asian and emerging benchmarks both. But to the extent that investors spooked by troubles in Argentina and Turkey are indeed dumping Asia as a knock-on effect, it fits with a weakness tied to globally diversified portfolios some two decades ago.

Economists Guillermo Calvo and Enrique Mendoza warned about the volatility of capital flows stemming from globalization of securities markets making herd behavior more likely. Writing during the Asian financial crisis in 1998, their paper suggested investors had diminishing incentives for investigative research into individual markets, and faced potential reputational costs of performance diverging from benchmarks. Put simply: why wait to sell in a panic?

Asian equities were significantly outperforming emerging stocks more broadly from the start of the slide back in January until mid-June. Relative performance has worsened since China began overseeing exchange-rate depreciation as its trade war with the U.S. escalated. That removed what had been something of an anchor for other Asian currencies.

“Once the RMB started devaluing from mid-June through early August, where we interpreted RMB devaluation as an attempt by China to offset the initial round of U.S. tariffs,” Asian currencies stopped outperforming the rest of the emerging foreign-exchange complex, said Robin Brooks, chief economist at the Institute for International Finance. RMB stands for the renminbi, the official name for the Chinese currency.

China has had a role in other ways as well, with an increasing presence of its domestic stocks in MSCI’s emerging-market index. Some 236 such shares were added this year in a two-step process that was completed on Friday.

--With assistance from Sebastian Boyd and Eric Lam.

To contact the reporters on this story: Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net;Enda Curran in Hong Kong at ecurran8@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Ravil Shirodkar

©2018 Bloomberg L.P.