A Wildfire-Predicting Startup Tries to Help Insurers Cope With Climate Change

A Wildfire-Predicting Startup Tries to Help Insurers Cope With Climate Change

(Bloomberg Businessweek) -- Climate change is making California’s fire seasons more severe, but the conditions that lead to any single fire remain consistent: dry weather, overgrown brush, wind speed, and wind direction. Private companies and public agencies are racing to develop technology to monitor these conditions, in the hopes of understanding how wildfires spread—and predicting them before they happen.

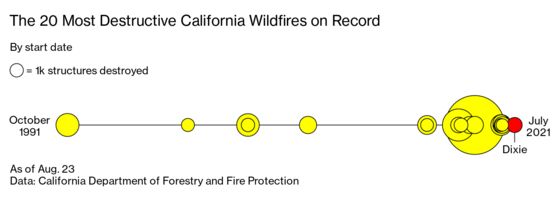

As a bigger proportion of the country’s most populous state burns, the stakes of getting those predictions right goes up, too. Six of the seven largest fires in California’s history have occurred since August of last year, and extreme drought throughout the American West has experts concerned that this year’s season is shaping up to be particularly bad. Human lives are on the line. So are billions of dollars.

There’s demand for wildfire forecasting from both the public sector and commercial interests. As of now much of the innovation is coming from technology companies looking to serve insurers grappling with increasingly costly and erratic blazes—a trend that could determine not only how predictive software is used but how it’s designed. These dynamics are on display with Kettle, a startup that’s created a predictive system by using artificial intelligence to help it design reinsurance policies that protect insurance companies against wildfire risk. Andrew Engler, who has spent years in the insurance industry, first as a sales lead at Allstate and then a vice president at Argo Group, and Nathaniel Manning, former chief executive officer of the humanitarian communication crowdsourcing app Ushahidi, founded Kettle in 2020.

Reinsurers have traditionally used a technique called stochastic modeling, which analyzes historical data to determine the likelihood of random events. That doesn’t work when the changing climate system behaves in ways that humans have not yet seen, Engler says.

“If the way you price risk is you go, ‘OK, how many times has a wildfire hit Los Angeles in the past 500 years? Well, it’s happened twice, so we’ll peg all of our pricing this year at a 1-in-250 chance that Los Angeles will burn,’ you’re going to be wildly wrong, because the next 15 years are going to look nothing like the past 500,” he says. “So understanding that, there’s a major opportunity here.”

Kettle is looking to analyze enormous amounts of geospatial imagery to find emerging patterns. It pulls in data from satellites and weather data maps to predict the areas in California most at risk for wildfire.

Many insurers have responded to a trend of record-breaking fire seasons by raising rates or refusing to cover some areas. The problem has gotten bad enough that California’s insurance commissioner has issued moratoriums on canceling or refusing to renew insurance in some ZIP codes hit by a fire emergency for one year after the area burns.

Engler’s thesis is that many areas that insurers avoid are safer than they seem. Last year, the third-worst year in California’s fire history, almost 11,500 properties were destroyed, and 4.5 million acres burned. Although devastating, he says, that was only a fraction of the 14 million homes in the state, and 4% of the land. “When we see the response from an industry being, ‘The state’s uninsurable,’ that’s completely incorrect,” he says.

The predictive tech is tied to a novel business model for reinsurance. Typically, insurers work with multiple reinsurance companies to cover their entire portfolio. Kettle models the risk of an insurer’s entire portfolio, then offers to sell fire-specific policies that cover a fraction of those homes in the areas where Kettle’s model has the most certainty about burn patterns. It says 26 carriers have asked it to model their risk.

The company recently used historical data to see how well its model would have performed during the 2020 fire season. It examined the 14 largest wildfires in California that year and found that 11 of them occurred in areas Kettle’s software labeled as top 10% most likely areas to experience wildfire in 2020; all 14 fires were in the top 20%.

Kettle has attracted outside investors into its underwriting programs, but it also plans to put up its own money when it begins writing policies next year. The company argues that holding some risk aligns it with its clients’ interests better than if it sold only software subscriptions.

There’s a big difference between knowing which areas are likely to burn and which actually will burn over any discrete time period, says Andre Coleman, a senior research scientist at Pacific Northwest National Laboratory. Even the most fire-prone areas need a spark, and no software is good enough to anticipate which stretch of highway will get the fateful cigarette thrown out a car window, or the location and timing of the overly exuberant gender reveal party. “If you take the fire risk data as it’s published by others, and you overlay where fires are actually happening, there’s not a really strong correlation,” Coleman says.

Coleman agrees with Engler that climate change is complicating conventional predictive techniques. Fires are regularly forging new paths. The Dixie Fire, an active blaze that’s already the second-largest in California’s history, became the first to traverse the Sierra Nevada from the foothills to the eastern valley. Coleman’s team is developing tools to increase situational awareness for people on the ground in the thick of a blaze.

The company’s models account for long-term uncertainty by simulating millions of theoretical scenarios. “You can’t predict every single gust of wind—every single, you know, plant leaf and what moisture density it is,” Engler says. But there are “emergent patterns that we see in these larger conflagrations with everything going wrong that you can start to hone into, and those are the areas that we’re going to find to be most dangerous over time.”

Other entities with interests in California’s wildfires have their own spins on predictive technology. State Farm Insurance, MetLife Inc., and other insurance companies use software from startups such as Cape Analytics LLC and Zesty.AI that also use AI and decades of satellite imagery to understand microlevel risk factors. This level of detail could allow them to examine features of individual homes—like scruffy vegetation in the combustible zone within 10 feet of a house—and price policies more in line with their risk. The U.S. Forest Service is incorporating AI models into its wildfire-fighting strategy, piloting RADR-Fire, a product that uses infrared technology and satellite imagery to help firefighters track fires through smoke and haze.

Having the kind of sophisticated rendering of risk that Kettle is developing could also help firefighters and local officials create shorter-term evacuation plans, determine where to build fire breaks, and better allocate resources. Engler and Manning say they envision sharing their findings with utility companies, firefighters, and the Forest Service. But for now they’re solely focused on insurers, a decision that influences the shape of their product. For instance, Kettle uses its new predictions only twice a year because that’s how often reinsurers sell new policies, even though it gathers new data constantly.

An insurance company’s definition of risk—and therefore the inputs and methodology of its predictions—can also differ from that of public actors, says Sean Triplett, a tools and technology team lead for the Forest Service. Kettle’s confidence intervals are based on what monetary risk they’re comfortable taking on, whereas the Forest Service is “worried about the whole ecosystem,” he says. “We’re worried about the whole community, we’re worried about the other values at risk—the power lines, the water quality, everything that goes into that.”

Others argue that the priority should be discouraging risky development, not finding ways to reclassify areas so insurers will cover them. “We need stricter constraints for building permits and [for] developers to respect them,” writes Dominique Bachelet, an associate professor at Oregon State University, in an email.

Manning says he’s not against disincentivizing development in fire-prone areas but says that the broad-swath hesitance of insurers is also harmful. He doesn’t accept the implication that insurance is somehow a less worthy application than emergency response. “This insurance solution is just beautiful, but it has such a bad rap,” he says. After a disaster there’s grave suffering and international attention, he argues, but the adversity continues after the acute crisis wanes. “After everyone leaves—the news, and the first responders—it’s basically this long tail of just the local community and the insurance companies, for years.”

Read more: Night-Flying Helicopters Provide Rare Advantage in Wildfire Wars

©2021 Bloomberg L.P.