Why the Marshall Islands Is Trying to Launch a Cryptocurrency

What Happened When the Marshall Islands Bet on Crypto

(Bloomberg Businessweek) -- David Paul looked nervous. He rested his hand over his mouth, fidgeted with his wedding ring, sometimes smiled and sometimes grimaced as the legislature for the Republic of the Marshall Islands debated a motion to oust his boss, President Hilda Heine, from power.

Paul, a top government minister, wore a purple tie and a ribbon on his pocket—the color signaling support for Heine. The tie and dark suit also marked the importance of the occasion in a country where shorts and Hawaiian shirts are standard business attire. One of Heine’s opponents the previous week called for a vote of no confidence. Among the complaints: The president had supported a plan to create the first legal tender cryptocurrency in the world—a digital token called the SOV, for “sovereign.”

If the vote of no confidence passed, most Marshallese expected the opposing senators to repeal the cryptocurrency law. “I knew it was close,” Paul says. “I knew going in it was close.” With one member absent in the 33-member Nitijela, Heine got exactly half the vote, with a tie going to the incumbent. She had eked out a victory. Paul says he never really doubted the outcome.

He might have had reason to worry. The Marshall Islands crypto project, which was largely Paul’s baby, seemed like a good idea until the international finance community responded by threatening to cut off the tiny Pacific island nation from the global banking system. When the Nitijela passed the law authorizing the SOV in February, a Bitcoin was trading for more than $10,000, and someone had just spent 10 times as much for a virtual pet kitten based on crypto technology. But by the time of the no-confidence vote, in mid-November, Bitcoin was worth $6,000, and all kinds of crypto assets were hurting.

The Marshalls’ experience in the boom and bust throws into relief problems the country faced long before it tried to go crypto: increased isolation from the financial world as bank after bank fled the islands and a desperate need for cash. But some Marshallese worry the SOV brings new problems with an uncertain payoff. “There should have been more due diligence,” says Senator Bruce Bilimon, who abstained from the vote to create the currency but was in favor of the vote of no confidence. For the company that helped pull the Marshall Islands into the plan, he says, “it’s good it’s taking risks. But is it worth taking risks for a country?”

Paul had just joined President Heine’s cabinet when he was asked in January to speak with two entrepreneurs who’d traveled more than 8,000 miles from Tel Aviv to meet with members of the government. He was a first-term senator from Kwajalein Atoll, where the U.S. has a missile defense facility, and Heine had appointed him “minister-in-assistance,” a broadly defined position that effectively made Paul her right-hand man. She asked him to hear the entrepreneurs’ pitch.

Paul says he’d never owned Bitcoin but followed it for years, and he seized on the project immediately. At the meeting he met Barak Ben-Ezer, then 39. Ben-Ezer was the founder of Neema, a company that uses digital currencies to provide financial services to unbanked populations in developing countries. He wanted the Marshall Islands to let Neema embark on an even more ambitious project.

Paul and the other Marshallese had never heard of Neema, but they said they ran a background check later. Ben-Ezer had studied computer science and economics at Columbia University. Neema had received seed funding from Y Combinator, a Silicon Valley incubator whose success stories included Airbnb Inc. and Dropbox Inc.

Paul thought the project could burnish the country’s reputation. “You always remember who was the first to step on the moon—that was Neil Armstrong,” he says. Likewise, the SOV could be remembered as the first national digital currency ever launched. But beyond Paul’s dream of making an international mark, Ben-Ezer’s idea had some specific practical appeal.

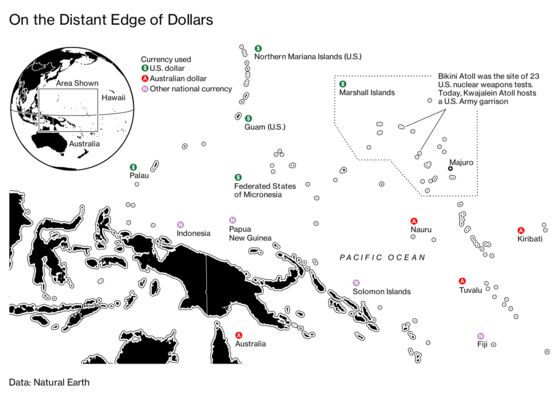

Formed by volcanoes that later sank back into the ocean, the Marshall Islands are thin slivers of land wrapped around shallow lagoons. The country, which became independent from the U.S. in 1986, has a population of about 53,000 spread over 24 inhabited atolls with a combined 70 square miles of land. That’s about the same as Washington, D.C.—if you cut that city’s population by 90 percent, broke it into pieces, and spread it over a swath of ocean larger than Alaska.

Majuro, the most populous atoll and the seat of government, has no addresses and one main street running its length. In some places, you can look straight down the road and see both the Pacific and the inner lagoon out of the corners of your eyes. Flooding is constant. Sometimes powerful tides or swells cause the lagoon to sweep across parts of the island and into the sea. The government sends out mass text messages to warn “inundation is very likely” when the weather service projects tides will be at their worst. A one-foot rise in sea levels, which some scientists predict could happen as soon as 2050, could put portions of the island permanently underwater. To deal with rising sea levels, the government hopes to raise the land on the islands higher, but that could cost billions of dollars. The Marshalls have an important strategic position for the U.S., and aid accounts for around half of the government’s revenue. But under current agreements, U.S. financial support ends in 2023.

At the time Ben-Ezer pitched the SOV, Neema said it could have the “initial monetary offering” ready to go in three months. Long term, he said, he thought that one day the SOV could become an international currency, and the Marshall Islands could become a link between the crypto world and the traditional financial world in the same way that Hong Kong and its dollar became important despite its size.

For the initial currency offering, the Marshalls would rely on speculators believing in that future, or at least believing that someone else would believe it long enough for the SOV’s value to rise. As the Marshallese considered the project, they read that the messaging startup Telegram had raised almost $1 billion from private investors by selling its own cryptocurrency. So the idea of being able to sell a new currency attached to an actual country didn’t seem like such a long shot.

The country would issue 24 million SOVs, of which the Marshall Islands would get half. Neema projected that the SOV could trade for $50 each. The country planned to sell half of its coins right away, which if the projection was correct, would raise $300 million. Of the nation’s share, 2.4 million SOVs would go straight to Marshallese citizens in payments over five years. Neema agreed to bear all the development costs itself, with the government putting up nothing but its reputation. The SOV would have one thing that Bitcoin and other virtual coins could never match: the backing of a government. (As the Nitijela debated the SOV law, Venezuela unveiled its own cryptocurrency, called the “petro.”)

If the cryptocurrency plan seemed like a get-rich-quick scheme, that was, to some extent, what the Marshall Islands needed. The problems “are right in front of us, and there is no real and tangible solution that we can see,” Heine says. She’s been traveling the world trying to persuade donors and development partners to contribute money, with mixed success. The regular currency of the Marshall Islands is the U.S. dollar, and it would continue to be used alongside the SOV no matter what happened with the launch, she says. “If it doesn’t work, I’m like, ‘Well, what do we have to lose?’ ”

Beyond the money, Paul and Ben-Ezer thought the currency could solve another imminent problem. The U.S. crackdown on money laundering has made it less profitable and more risky for international banks to work with tiny nations such as the Marshalls. The only bank with branches throughout the islands relies on First Hawaiian Bank, and its connections to BNP Paribas SA, to provide basic services such as international money transfers or cashing locals’ paychecks from the military base. First Hawaiian has said it plans to shut down that link but has agreed to a delay while the country looks for replacements. So far, it hasn’t found any.

With the new currency, Paul thought, the Marshallese wouldn’t be held hostage to banks to get money off and on the island. The government could go from begging for banks to come and stay to asking why it needed them at all.

Ben-Ezer recalls that after the bill passed, on March 1, he attended the country’s ceremonies for its remembrance day for nuclear testing victims. Beginning in 1946, the U.S. conducted 67 nuclear tests on Bikini Atoll and other islands. Residents have suffered from the effects of the fallout ever since. The speaker of the Nitijela, who supported the Marshalls’ crypto project, gave a moving speech, and at its conclusion told the crowd that the legislature had just passed a bill that would bring in millions of dollars to help those hurt by the tests. The law established the SOV as the national currency and outlined what would be done with the proceeds once it was launched. But it gave only a rough sketch of how the government would get that done. The speaker signed the bill into law right there on the podium.

It took a few days for the international banking community and the U.S. government to become fully aware of what had just happened. The law created a Legal Tender Committee, whose job included documenting the project’s potential risks. Chief Secretary Ben Graham, who’s coordinating the committee, says that after the law passed people started bombarding the government with questions and potential snags. What if the price of the SOV is so volatile that it makes it impossible to use in the real world? What if the local telecom system can’t handle it? What if it’s used for money laundering or terrorism financing?

The legislature in February gave the U.S. Embassy a heads-up that it was considering a cryptocurrency law, but passed the bill before getting a response. On April 11 the Marshall Islands got its first official notification, in a letter from the U.S. ambassador, that the U.S. wasn’t happy.

The letter said the U.S. was disappointed it wasn’t consulted before passage of the bill. It thought the cryptocurrency raised money laundering and terrorism financing concerns, could make the country’s economy unstable, and could even spook the last outside bank connected to the island into cutting ties sooner.

A couple weeks after the embassy letter, Paul and Finance Minister Brenson Wase traveled to Washington for the annual meeting of the International Monetary Fund and the World Bank. The U.S. Department of the Treasury asked them to stop by, and Wase says the walk down the Treasury’s long hallways to the meeting room was tense. Paul, Wase, and three other Marshallese on the trip sat across from 15 representatives from the U.S. government. Treasury Assistant Secretary for Terrorist Financing Marshall Billingslea kicked off the meeting. “He said, ‘I don’t like it. I will never support it,’ ” Wase recalls.

Paul says the group sparred for hours. The Marshallese said Treasury was jumping to a conclusion without even seeing the anti-money-laundering and “know your customer” protocols that Neema was developing. The design would require every holder of the SOV to register his identity, which they said would make the SOV unusable for money laundering and terrorism financing. At the end of the meeting, the Treasury officials agreed to meet again when development was further along, which Paul took as a sign there was an opening to get their approval. In an email to Bloomberg Businessweek, a Treasury spokesman wrote that the department has serious concerns with the project and that the Marshall Islands will decide for itself whether to proceed given the risks.

Marshall Islands officials had a similar meeting with First Hawaiian Bank, which said launching the SOV could lead the company to pull out of the country. A regularly scheduled visit from the IMF didn’t go much better. It issued a report recommending that the country abandon the project.

“The risk is much bigger than the benefit they expect,” says Joong Shik Kang, who led the IMF review. If the currency were implemented poorly, it might be the currency of choice for terrorists trying to move money outside the view of the U.S. government or for money launderers trying to evade taxes. For Kang, the project is a risk even if it works. If the SOV does trade at $50 apiece, does pushing $120 million into the economy—the equivalent of 60 percent of the country’s annual output—cause inflation on the islands? What happens to the economy if the SOV price crashes?

For Wase, Paul, and other officials desperate for a way to raise money, the arguments seemed hypocritical. The Marshall Islands needed hundreds of millions of dollars now. What brilliant ideas did their critics have for raising that money? “We told them, ‘OK, we will try, but you should do your part in trying to resolve this problem,’ ” Wase says of the country’s banking issues and need for funds. Otherwise, he said, it had no choice but to take a chance on projects like the SOV. Wase says that at October’s IMF meeting in Bali, other Pacific Island countries with scant funds and their own international banking problems told the IMF they wanted to follow the Marshall Islands’ lead.

International regulators, banks, and the U.S. Treasury Department didn’t succeed in getting the Marshall Islands to give up the project, but they did slow it down. Marshallese officials promised that once the critics saw the SOV’s anti-money-laundering controls, their fears about that would subside. Still, most government officials don’t think proceeding with the launch of the sovereign is worth it until the concerns are allayed.

Foreign Minister John Silk says losing the banking links would be devastating. The U.S. Army base on Kwajalein Atoll employs hundreds of locals. If the Bank of the Marshall Islands lost its relationship with First Hawaiian, the Marshallese workers wouldn’t be able to cash their paychecks, he says. “At the end of the day, when it comes to the choice between whether you want to continue the correspondent banking relationship or have a SOV, personally, I’d want the banking relationship,” Silk says.

The Sunday after the vote, Kalani Kaneko, who co-sponsored the legislation establishing the SOV, is on a boat in Majuro’s lagoon right off the island of Eneko, which is a short trip from downtown but feels remote. Since independence, Marshallese still serve in the U.S. military, and Kaneko spent 20 years with the Army before running for office in the Marshalls. His family swims in the azure water of the lagoon, which is dotted with ships that transport tuna to canneries across Asia.

As the boat powers around the lagoon, Kaneko gestures toward newly built seawalls. During severe tides, he says, the water comes right up to the rim. Homeowners beset with flooding lobby to get their own protection, but the government has enough funding only to build small lengths at a time, and even those aren’t high enough to deal with some storm swells. Kaneko points out lower areas of land likely to go underwater first as sea levels rise.

Neema and the Marshall Islands still have a long way to go with the SOV project. Few Marshallese are aware that they may soon be using a second currency. A waitress at a local coffee shop says she didn’t even know about the SOV until hearing it debated during that week’s vote. Cryptocurrencies rely on a web-connected economy, but a group of University of the South Pacific college students sharing a pizza laugh when asked if the internet is reliable. Power outages are frequent, and the students say the ATMs run out of cash all the time. Their parents use only the basic functions of cell phones, and on more remote atolls, Neema has determined it might issue a form of “crypto cash” that can be used in places with intermittent internet access. Ben-Ezer says the technology for the SOV will be ready by midyear.

Then it will be up to the Marshall Islands to pull the trigger. With more problems than money, it’s running low on options. “That’s why we need this to fly,” Kaneko says.

To contact the editor responsible for this story: Pat Regnier at pregnier3@bloomberg.net

©2018 Bloomberg L.P.