Biden May Get the Weaker Dollar That Eluded Trump’s Presidency

Biden May Get the Weaker Dollar That Eluded Trump’s Presidency

(Bloomberg Businessweek) -- A weaker dollar and the boost that it could provide to U.S. exporters and manufacturers has long been part of President Donald Trump’s prescription to make America great again. But it could be his opponent, Joe Biden, who gets a less mighty greenback and its spoils.

Long before the novel coronavirus pandemic upended the global economy, the alleged unfairness of U.S. trading relationships with the rest of the world was a cornerstone of Trump’s rhetoric and actions. Accusations of currency manipulation have been as much a mainstay of his policy as tariffs on items ranging from solar panels to washing machines. And grievances about the strength of the dollar—often part of attacks against China, Europe, and even the U.S.’s own Federal Reserve—have been a staple of the president’s Twitter feed.

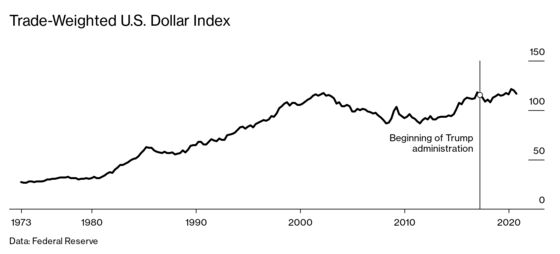

The Fed’s trade-weighted measure of the U.S. currency, which goes back to the 1970s, shows the dollar has on average been stronger since Trump’s election than under his predecessors—and about 18% higher than during the eight years following Barack Obama’s initial win. “Trump said he wanted a weaker dollar, but what he did meant it got stronger,” says Ned Rumpeltin, a currency strategist at Toronto-Dominion Bank.

A big part of the equation was the relative economic strength of the U.S. over recent years and what that’s meant for monetary policy and investor returns. Following the crisis of 2008, the economy’s expansion under Obama and Trump, which was the longest on record and took unemployment to a half-century low, was stronger than recoveries in other major industrialized nations. Unlike its peers in Europe and Japan, the U.S. central bank managed, albeit briefly, to lift interest rates away from zero, providing an appealing premium for investors that helped buoy the dollar.

The Trump administration’s policies also played a role in several distinct ways in pumping up the greenback. Its tax and regulatory changes helped attract investor money into the U.S. by giving a boost to corporate profitability. At the same time, the market instability caused by the president’s trade war with China fueled demand for the dollar, which has long been viewed as a safe-haven currency. And while swelling budget deficits under Trump might weaken the dollar, investors have appeared willing to overlook the mounting pile of debt.

“Trump was seen as business-friendly and pro-growth—less taxes, lower regulations—and that’s good for the dollar,” says Jack McIntyre, a money manager at Brandywine Global Investment Management. “But probably more important was the U.S. rate structure relative to the rest of the world.”

The dollar’s unprecedented strength has proven a boon for U.S. consumers and companies that buy products overseas, but for manufacturers competing with international rivals at home and abroad, it’s driven up costs and stymied growth. Now there are some signs that the tide is turning.

The dollar remains close to its average under Trump, but it’s fallen more than 8% from its peak earlier this year and is forecast to weaken further. The premium that U.S. Treasuries provide over comparable debt from major economies such as Germany has shrunk as the Fed has retreated from its foray into higher interest rates. U.S. policymakers intend to keep rates near zero for years to come to encourage people and businesses to spend their way out of a recession, a stance that typically weighs on a nation’s currency. The pain caused by the pandemic may prompt even more monetary easing.

The median estimate in a Bloomberg survey of currency strategists is for Intercontinental Exchange Inc.’s widely watched dollar index—a gauge that tracks the greenback against its biggest industrialized peers like the euro and the yen—to fall by almost 3% from now to the end of 2021.

A Biden presidency, especially if combined with a “blue wave” that gives Democrats control of Congress, has the potential to speed the U.S. currency’s slide. The party has drafted a coronavirus relief package that would increase the government’s already substantial borrowing by trillions of dollars.

As the issuer of the world’s foremost reserve currency, the U.S. has unique advantages. There will always be a certain level of demand for greenbacks, and the country is unlikely to ever default. Nevertheless, any perception that U.S. debt is spiraling out of control could fuel concerns about the valuation of the dollar.

Abdelak Adjriou, a money manager at American Century Investments, says that with U.S. debt rising, the dollar will weaken over the long term no matter who wins. Under Biden, that depreciation could “happen very quickly,” he says, because the Democrat may try to reduce the deficit with tax hikes.

A fiscal stimulus package could also provide a one-two punch to the greenback. If it encourages investors to channel cash back into riskier assets, it could sap some of the demand for dollars that comes from haven investors.

The U.S.’s relationship with China will be key to sustaining any decline in the dollar. The phase-one agreement the two countries concluded in January has led to detente in Trump’s trade war with Beijing. But peace is far from secure, especially with the U.S. president looking to lay blame for the Covid-19 pandemic at the feet of Xi Jinping’s government. Biden’s “Made in All of America” plan suggests he won’t go easy on China. It contemplates tax penalties for companies shifting to factories overseas, as well as “Buy American” provisions for government purchasing. Yet he’s viewed by many as less confrontational than Trump and more open to working with other nations. That combination, along with the expectations of a big bump up in fiscal stimulus, as well as possible increases in taxes and regulation in a Biden administration, may help put a dent in the mighty greenback.

Hanging over all of this is the lesson of 2016, when markets’ unexpectedly upbeat reaction to Trump’s victory left many on Wall Street red-faced. While the consensus wisdom is that a Biden White House and a Democratic Congress equals a weaker dollar, any economic recovery they preside over could attract money to the U.S., supporting the currency. On the flip side, a Trump win and a divided legislature might well extend the current stalemate over fiscal stimulus, cementing the need for ultralow interest rates that weigh on the currency. And then there’s the big unknown: the risk of a contested election. Months of uncertainty would likely fuel demand for the greenback as a haven.

Read next: Trump’s America First Policies Have Not Stopped Factories From Offshoring

©2020 Bloomberg L.P.