Top U.S. B-School Students Pile on Debt to Earn MBAs

Top U.S. B-School Students Pile on Debt to Earn MBAs

(Bloomberg Businessweek) -- For aspiring executives, the truism that’s held constant for a generation probably has been that there’s no faster way to advance up the corporate ladder than to go back to school and get an MBA. For many, it’s also been the quickest way to pile up a mountain of debt.

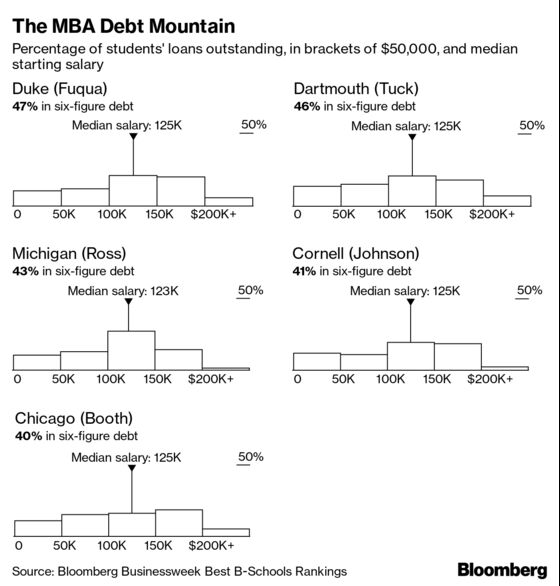

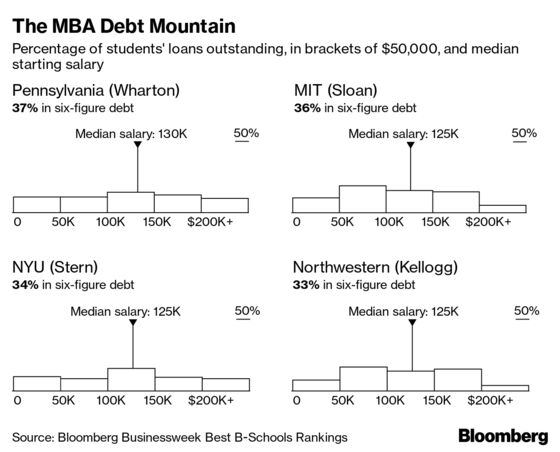

New data from a Bloomberg Businessweek survey of more than 10,000 MBA graduates from the class of 2018 at 126 schools around the world suggest that nearly half the students at some of the best business schools are borrowing at least $100,000 to finance their master’s degree in business administration.

At least 40% of survey respondents who got MBAs at Duke University’s Fuqua School of Business, Tuck School of Business at Dartmouth College, University of Michigan’s Ross School of Business, SC Johnson Graduate School of Management at Cornell University, and University of Chicago Booth School of Business reported incurring six-figure debt loads for their programs, data show.

About a third of recent MBA graduates at nine additional top schools said they had borrowed at least $100,000, including alumni of such schools as MIT Sloan School of Management, Wharton School at the University of Pennsylvania, NYU Stern School of Business, and Kellogg School of Management at Northwestern University.

The survey results shed new light on the amount of debt that aspiring executives and entrepreneurs take on to jump-start their careers with a credential prized by the nation’s leading financial institutions, consultancies, and corporations. Long considered one of the most expensive graduate degrees, MBAs have tended to be pursued by prospective students because the payoff in higher pay and wider career opportunities convinced them that the degree was worth it.

At the 26 schools where at least 20% of survey respondents reported borrowing six-figure sums to finance their MBAs, median starting pay ranged from $80,000 to $140,000, according to data from Bloomberg Businessweek’s Best B-Schools Rankings.

“I don’t view it as a burden,” says Mike Sanchez, a 32-year-old Citigroup Inc. investment banker who graduated last year from Booth with about $110,000 in student debt. “Long term, the ROI [return on investment] is still pretty good.” Last year, the median starting salary among Booth graduates was $130,000, the school says. (The Best B-Schools Rankings cites the prior year’s salary of $125,000 because the more recent figure wasn’t available at the time of publication.)

The findings show that a credential typically sought by early- and mid-career professionals with white-collar jobs has joined the ranks of other higher-education programs that have led American workers to take on ever-greater debt in pursuit of decent-paying careers. In the U.S., outstanding student debt has more than doubled in recent years, to $1.6 trillion, Federal Reserve data show.

The survey data puts into stark relief just how much of a return some students need to justify their debt-financed investment.

Across the 126 schools whose students responded to Bloomberg Businessweek’s survey, about one in five (18%) reported borrowing six-figure sums to finance their MBAs. About 17% said they borrowed from $50,000 to $100,000, while 22% reported less than $50,000 in debt. Some 44% of respondents said they graduated with an MBA without having had to borrow to pay for it.

The survey shows that recent MBAs from U.S. schools, which are mostly two-year programs, tended to report higher debt levels than their peers from schools outside the U.S., where students generally graduate faster.

“Earning an MBA is a significant investment—of both time and money—and we know many of our students make financial sacrifices to pursue the degree,” says Russ Morgan, senior associate dean at Duke’s Fuqua school. The school, Morgan says, has increased the amount of money it makes available for scholarships.

The focus on student debt comes as policymakers, economists, bankers, and politicians sound the alarm on what’s becoming an increasing risk to U.S. economic growth. Student loans are the only consumer debt segment that’s experienced continuous growth since the Great Recession, and recent research suggests that skyrocketing debt levels are preventing young Americans from purchasing homes, a key driver of economic growth and household wealth creation. “We’re seeing more and more evidence of that as student debt grows,” Federal Reserve Chairman Jerome Powell told Congress in February.

The GI Bill and other grants enabled Sanchez, a former Navy nuclear engineer who spent years on a submarine before enrolling at Booth, to borrow considerably less than did the 24% of Booth grads who said they had taken out at least $150,000 in loans for their MBAs.

But his roughly $110,000 in student debt is a large enough tab that it prompted Sanchez to debate how much of his pay should go toward repaying his loans vs. toward a future down payment on a house, he says.

“I think considerably about the value and the financial returns of a Tuck education,” says Matthew Slaughter, dean of Dartmouth’s Tuck school, where last year’s median starting salary for graduates was $130,000. “First-year compensation for Tuck graduates is indeed strong and continues to climb, but we also care about long-term outcomes and the human gains of a Tuck education.”

Steve Alexis, 31, a supply chain manager at Google who graduated from Howard University School of Business with about $40,000 in student loans, says he has “no regrets whatsoever” about the amount of debt he incurred to pay for his MBA. He worked in sales before enrolling at Howard, and “to elevate from non-management to where I’m in charge of some operations, it was worth the investment,” he says.

Rankings data show that median salary among recent Howard MBA grads is $100,000.

At Michigan’s Ross school, where 43% of survey respondents said they had borrowed at least $100,000 to finance their MBAs, the 2018 median salary came out to $125,000, suggesting that recent grads are making enough money to comfortably pay down their debts. “We are proud of the return on investment that Ross students see, both in their starting salaries after graduation and the long-term value they receive from the MBA throughout their careers,” says Brad Killaly, an associate dean.

Alexis, who received scholarships that helped defray his cost of attending Howard, said he would have pursued an MBA even if it had caused him to graduate with double the amount of debt. Sanchez says he would’ve done so, too—though only from a top school. Six-figure debt for an MBA from a middling program wouldn’t be worth it, Sanchez says.

To contact the editor responsible for this story: Caleb Solomon at csolomon13@bloomberg.net

©2019 Bloomberg L.P.