The Problem for Business When Inventory Is No Problem

The Problem for Business When Inventory Is No Problem

(Bloomberg Businessweek) -- In an industrial economy, businesses build up inventories to meet expected demand. If sales disappoint even slightly, those inventories can balloon, leading companies to cut production and lay off workers, depressing overall demand. As economist Lloyd Metzler described this “inventory cycle” in a classic 1941 paper, “An economy in which business men attempt to recoup inventory losses will always undergo cyclical fluctuations.”

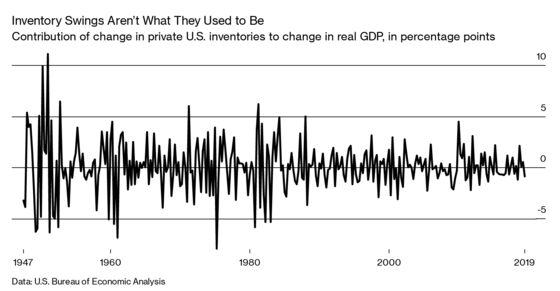

The U.S. economy has changed a lot since the 1940s. Goods represent a much smaller share of gross domestic product than they used to, and the services and virtual products that have taken their place generally have no inventories. Just-in-time manufacturing and better technology for tracking sales have also enabled manufacturers and retailers to get by with smaller stocks of goods on hand. In the process, inventory swings have become a much smaller factor in economic fluctuations.

This shift got a lot of attention in the early 2000s, when economists were trying to explain the “Great Moderation” of the business cycle. The sharpest economic downturn in seven decades put most such research on hold, but with the current expansion now the longest on record, it seems quite relevant again.

As inventory cycles and other ups and downs of an industrial economy have become less important, it now seemingly takes a financial-market meltdown—such as the stock market collapse of 2000-02 and the mortgage crisis of 2007-08—to send the economy into reverse. In the meantime, a smoother, steadier economy lulls investors into the very complacency that leads to crisis.

• Keep It Going

Unless a recession is declared retroactively (which seems unlikely), the current expansion is 121 months old as of the end of July.

• Out With the Old

The current expansion breaks the previous record of 120 months, a period of growth that stretched from the waning years of George H.W. Bush’s presidency to the beginning of George W.’s.

• Steady But Slow

U.S. economic growth is smoother but slower, averaging 2% a year since 2000 and 2.7% going back to 1980. From 1929 to 1980, it averaged 3.6%. Measures of entrepreneurship and productivity growth are down, too. Less volatile isn’t necessarily better.

• Shifting Priorities

In 1950 total inventory value equaled more than 5% of U.S. sales. In the second quarter of 2019 it was 2.3%, tied for the lowest ever. Services’ share of GDP, which averaged 44% in the 1940s and 42% in the 1950s, is now 62%.

Fox is a business columnist for Bloomberg Opinion.

To contact the editor responsible for this story: Jillian Goodman at jgoodman74@bloomberg.net, Howard Chua-Eoan

©2019 Bloomberg L.P.