The Fed Is Paying 0.00%. Such a Deal! Depositors Are Flocking

The Fed Is Paying 0.00%. Such a Deal! Depositors Are Flocking

(Bloomberg Businessweek) -- You would think the Federal Reserve would have a hard time attracting funds by offering an interest rate of 0.00%, and for a long time that was true. After all, why earn nothing on your money when there’s Bitcoin and AMC Entertainment Holdings Inc. and lumber and houses in Boise? Many days last year and early this year there were no takers.

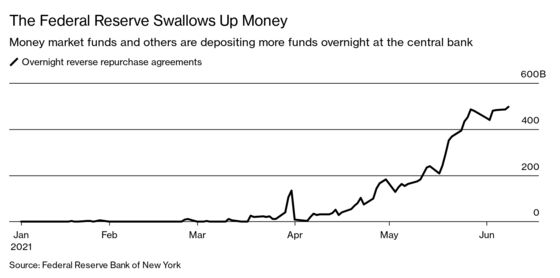

Starting in April, though, no interest started looking interesting to certain investors with too much cash on their hands. The amount of money they placed at the Fed overnight at 0.00% grew from nothing to single-digit millions to billions and, as of June 8, $497.4 billion. That’s the most ever.

Banks and money market mutual funds are unhappy with the situation and they’re pressing the Federal Reserve to do something about it. Others say there’s no rush to tinker. The Fed facility that’s taking in all that money is “doing what it’s designed to do,” Credit Suisse Group AG analyst Zoltan Pozsar wrote in a client note on June 4.

Meanwhile, the numbers are likely to get even bigger, the Bank Policy Institute, a research and advocacy group, said on June 8. “We could see take-up nearing $1 trillion at the end of the second quarter of 2021, driven by the seasonal spikes,” wrote Francisco Covas, its head of research.

The quick explanation for this is that there’s a lot of money sloshing around the financial system, and for regulatory reasons banks don’t want to take it in as deposits. So money market mutual funds are absorbing the money. Each night they place some of their assets with the Fed and earn nothing, which is bad for their profitability. As for the Fed, the reason it even offers the facility is that otherwise the forces of supply and demand might push the federal funds rate below zero, which it has vowed not to let happen.

The longer explanation gets at why this is suddenly happening now. As the Bank Policy Institute explains, the key reason is a rule change regarding bank capital requirements that took effect on April 1. It has to do with a clunky requirement called the supplementary leverage ratio, which is intended to prevent banks from taking on too much debt to acquire assets. The fear, of course, is that the assets will lose value and make the banks insolvent. The supplementary ratio, in its clunky way, treats all assets as equally risky, even though of course they aren’t: Treasury bonds and reserves at the Fed are extremely safe.

When the Covid-19 crisis hit last year, regulators waived the rule, temporarily excluding banks’ holdings of Treasury bonds and reserves from the supplementary leverage ratio calculation. But the waiver ended on March 31 of this year, so banks once again have an incentive not to take in a lot of funds (such as deposits) to acquire a lot of assets (such as Treasuries and reserves). A related rule that’s getting the biggest banks to push away deposits is the capital surcharge for global systemically important banks.

The Fed itself is increasing the pressure on the system by continuing to buy $120 billion a month of Treasuries and mortgage-backed securities to push down long-term interest rates. The money the Fed pays out, instead of going into bank deposits, is winding up in money market mutual funds, and then circulating into the Fed’s deposit facility, which consists of overnight reverse repurchase agreements.

One problem with this situation is that the Fed is taking over what used to be a mostly private function. If money market funds get used to keeping a lot of their money at the Fed instead of investing in, say, the commercial paper of private companies, they may switch even more money to the Fed in some future crisis, depriving the private sector of needed funds. This isn’t just a theoretical concern—companies lost access to funding in the global financial crisis of 2007-09.

The Bank Policy Institute quotes from a 2015 Fed staff working paper:

“Most importantly, a permanently expanded role for the Federal Reserve in short-term funding markets could reshape the financial industry in ways that may be difficult to anticipate and that may prove to be undesirable. For example, a permanent or long-lasting facility that causes very significant crowding out of short-term financing could lead to atrophying of the private infrastructure that supports these markets. Partially in response to some of these concerns, the FOMC has made clear that an ON RRP facility is not intended to be permanent.”

Except now the overnight reverse repurchase facility seemingly is permanent, or at least long-lasting—and large.

©2021 Bloomberg L.P.