The Big Student Debt Questions That Biden Will Have to Answer

The Big Student Debt Questions That Biden Will Have to Answer

(Bloomberg Businessweek) -- Just a few years ago, writing off large chunks of the U.S.’s $1.7 trillion in student debt seemed like a fringe idea. In a few weeks’ time, it could be government policy.

Joe Biden ran on a promise of forgiving at least $10,000 in student debt per borrower. As president-elect he’s getting bombarded from all directions with advice on how to scale up that plan—or back away from it.

In Biden’s Democratic Party, many want him to cancel a bigger portion of the loans via executive order right after taking office this month. They say it’s a way to aid the economic recovery without getting bogged down in congressional wrangling. Biden told journalists just before Christmas that he’s unlikely to go that far.

Critics of debt forgiveness at liberal think tanks as well as some congressional Republicans want him to abandon the idea altogether. They say channeling resources to college grads who are already better off than most Americans is unfair and ineffective as stimulus, because it won’t trigger a jump in consumer spending.

What follows is a roundup of some of the main arguments—and the numbers attached to them—in a debate that’s set to heat up in the coming weeks.

How We Got Here

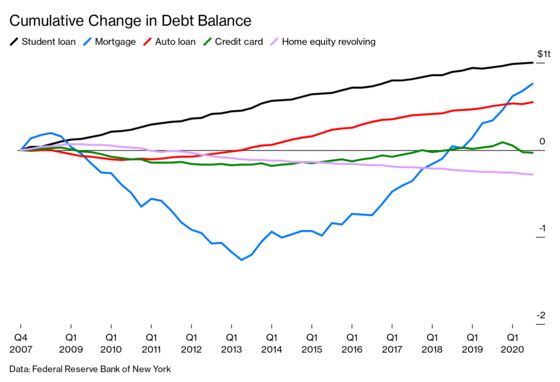

Since the financial crisis, U.S. households have added more student debt than any other kind—almost $1 trillion compared with $760 billion in mortgage loans. Some 43 million Americans owed money for their college education (or a family member’s) as of 2019, when the typical monthly payment was $200 to $300.

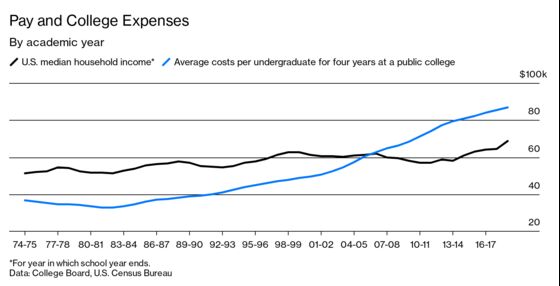

Borrowing has risen in tandem with college costs, which have outpaced incomes for a generation, and accelerated after the 2008 crash—partly because state governments cut funding for higher education and public colleges covered the shortfall by charging their students more. There’s also been a decades-long expansion of higher education that has drawn in students from lower-income families more likely to depend on loans. And unpaid debts can snowball, because even in an era of ultralow interest rates, student loans are pretty expensive. Interest rates have ranged from 4.5% to 8% in recent years, with graduate students and parents who borrowed on their kids’ behalf generally paying more.

For years now, delinquencies and defaults on student debt have been running much higher than for those on other types of loans. That’s in large part because, even amid the longest expansion in U.S. history, the economy hasn’t been creating enough of the well-paid jobs that all these graduates had counted on. High dropout rates, especially at for-profit colleges, are also a factor. In 2019 only about 40% of borrowers were current on their payments.

Those numbers underpin one of the key arguments for writing off the debt. “You’re not getting it paid off now, and you probably never will,” says Scott Fullwiler, an economics professor at the University of Missouri at Kansas City and co-author of a landmark 2018 study on loan forgiveness. “So what’s the bigger bang for your buck—cancel it now or just let it keep going?”

The Covid Freeze

Borrowers got a break in 2020. The pandemic rescue plan Congress approved in March put repayments on hold and stopped interest from accruing. The freeze—which applies to all loans owned by the federal government, or more than 90% of the total—expires at the end of January.

That’s the state of play that will confront the Biden administration on Day 1, and it practically guarantees some kind of early action on student debt. Otherwise, the restart of loan payments will act as a drag on the economy just when Democrats are promising a boost.

Action doesn’t necessarily mean mass debt forgiveness. Biden could just renew the payment freeze. President Trump did that by executive order in August, so it won’t trigger a dispute over presidential powers. But if Biden tries to use the same instrument to cancel student debt, bypassing a Congress where he may not have a Senate majority, some analysts foresee legal challenges. Democratic leaders including Senators Chuck Schumer of New York and Elizabeth Warren of Massachusetts see no obstacle to writedowns via executive order and are urging Biden to go well beyond his election promise and forgive $50,000 per borrower right after he’s inaugurated.

The Bill

Biden’s $10,000 plan would wipe out about $370 billion in loans, a figure that rises to almost $1 trillion in the more generous Schumer-Warren version, according to the Urban Institute. Because the large majority of the debt is owed to the U.S. Treasury, which has already issued bonds to cover it, writing off the loans won’t trigger a sudden jump in the national debt. Instead the cost will show up in the budget each year because the government would forgo revenue from loan repayments—worth about $80 billion, or 0.4% of gross domestic product, in 2018. So essentially forgiveness would function like a tax cut.

The Benefits

Tax cuts are stimulative. They also raise questions of fairness and effectiveness: Who benefits, and how much does the economy gain overall?

Critics say debt forgiveness helps college graduates at a time when low-paid service workers, mostly without degrees, have been hit hardest by the pandemic. It would sow more division in a country where education levels are one of the clearest fault lines. And they say it’s unfair to student borrowers who paid what they owed. Left-leaning think tanks like the Brookings Institution and the Urban Institute have argued this point strongly. Broad debt write-offs “will exacerbate the long-term trend of economic inequality between those who have gone to college or graduate school and those who have not,” wrote economists Sandy Baum and Adam Looney in a piece published on Brookings’ website in October.

Also, some argue that debt forgiveness won’t do much for the economy right now because the extra cash it frees up will be spread over years, will flow disproportionately to wealthier households less likely to spend it, and may incur tax liabilities that cancel out the stimulus effect.

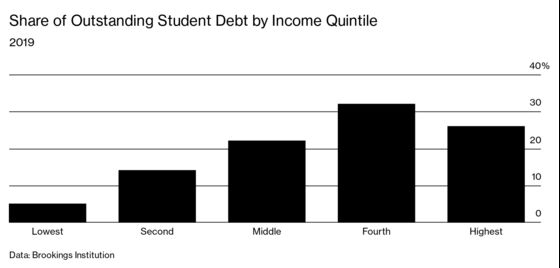

Advocates agree that wealthier families tend to have larger student debt totals, so they might get a greater break in simple dollar terms from forgiveness. But, they say, student debt is even more of a burden for lower-income families, so relief would benefit them more even if the value of loans forgiven is less.

There are other ways to slice the distributional question. Black borrowers, for example, typically have bigger loans and have found it especially hard to make headway repaying them. They’re more than twice as likely as White counterparts to be in deferral, according to a JPMorgan Chase & Co. report, so cancellation can help narrow racial wealth gaps.

The Bigger Picture

Student debt forgiveness can’t solve the root problem that college is unaffordable for many families, which is why everyone who’s proposed the policy has linked it to other measures that would lower costs for future students. Biden wants to make tuition at public universities free for families earning less than $125,000 a year. That would require steering legislation through a divided Congress.

Proponents of debt cancellation also say the attempt to calculate dollar-for-dollar returns on the policy misses the importance of shoring up household balance sheets, the same mistake Democrats made after the housing crash, when foreclosures threw millions of Americans out of their homes and unpayable mortgage debts were allowed to linger, sapping the recovery’s strength. Sometimes, they say, wiping the slate clean is best for growth.

“Sure, many people can probably do well enough, and constrain themselves, and manage to pay off their debt,” says UMKC’s Fullwiler. “But do we want an economy where that’s what people have to do?”

©2021 Bloomberg L.P.