Some Investors Actually Make Money on Negative-Yielding Debt

Some Investors Actually Make Money on Negative-Yielding Debt

(Bloomberg Businessweek) -- Money managers at BNY Mellon and Pacific Investment Management Co. have snapped up Japanese bonds. Both companies have made the country the second-largest geographic allocation in some of their biggest international fixed-income funds. Ordinarily that wouldn’t seem remarkable, but right now many of Japan’s government bonds have a negative yield—it actually costs money to hold them to maturity.

BNY Mellon and Pimco aren’t alone. Investors from outside Japan more than doubled purchases of the nation’s debt in July. What’s the logic? It turns out that buying Japanese bonds can pay better than holding U.S. Treasuries, as long as you happen to be a dollar-based investor and hedge your exposure to currency swings.

The currency effect turns the –0.25% yield on 10-year Japanese government bond into the equivalent of 2.22% in dollars, which is more than similarly dated Treasuries currently pay. “The returns are actually pretty good and competitive,” says Brendan Murphy, of BNY Mellon. About 17% of the $3.2 billion BNY Mellon Global Fixed Income Fund he co-manages is allocated to Japan’s bond market.

This bond market alchemy is a product of foreign exchange rates. When a U.S. fund buys a yen-denominated bond, it may choose to hedge the currency risk by entering enter into a forward contract that allows it to sell yen at a fixed price a few months later. The key to profitability for the U.S. fund is that now the yen will buy back more dollars on the back end of the transaction. The difference in exchange rates—between the value of yen now and the agreed price a few months from now—works out to an annualized return of about 2.5%, more than making up for the negative yield on the bond.

This might sound like a free lunch, but it makes economic sense. If one country offers a higher interest rate than another, and money is constantly moving around the world to find the best returns, forward currency markets end up adjusting to more or less equalize the difference. With U.S. Treasuries standing out as safe assets that still pay a positive yield, dollars are in demand around the world, and U.S. investors are in effect getting paid a bonus for parting with them to buy other assets.

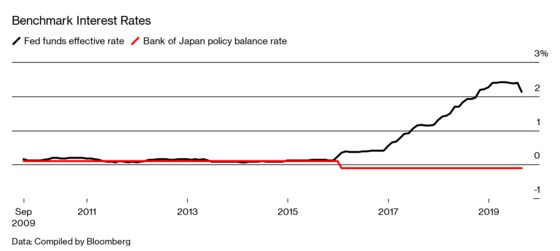

Thanks to a steady stream of Federal Reserve rate hikes since 2015, U.S. short-term interest rates are far higher than in almost every other developed market, even after the U.S. central bank cut rates in July to a range of 2% to 2.25%. By contrast, the Bank of Japan’s key rate stands at –0.1%. Both banks have policy meetings next week, with traders anticipating that the Fed will cut again, and speculation brewing that the BOJ will ramp up stimulus as well.

The extra yield that U.S. investors pick up from currency hedging would erode if the two nations’ interest rates converged. But while traders are pricing in about 1 percentage point of Fed easing over the next 12 months, Murphy doesn’t think the central bank will cut that aggressively.

Pimco money manager Sachin Gupta is of a similar mind. Gupta, based in Newport Beach, Calif., expects the Fed to lower rates again this year, but he thinks policymakers may be reluctant to preemptively cut again if the economy stays reasonably strong. So he’s comfortable keeping almost 15% of the $12.2 billion U.S. dollar-hedged International Bond Fund in Japanese bonds. The allocation is in line with the fund's benchmark. “You’re taking on the risk of the government of Japan,” says Gupta, who added longer-dated Japanese bonds earlier this year. “We think for a Group of Seven country with one of the largest economies in the world, that kind of risk in your own currency is de minimis.”

The hedging arbitrage isn’t limited to Japan. Gupta also owns low-yielding government debt from nations such as Spain, where hedging from euros into dollars produces a 2.72% annualized return. Murphy, of BNY Mellon, holds Spanish and Belgian debt.

Even bond managers who aren’t especially bullish on Japanese bonds see the appeal of the currency play. The $6.6 billion T. Rowe Price International Bond Fund allocated less to Japan than its benchmark index does, but it’s been parking money in the nation’s short-maturity government bills. “The very short end is an alternative to holding U.S. cash,” says fund manager Kenneth Orchard. “You do pick up yield holding Japanese T-bills instead of holding U.S. government T-bills, and that’s purely from the FX swap component.” After protecting against currency swings, a three-month Japanese bill yields 2.29%. That compares with –0.12% unhedged, and 1.95% for a similarly dated U.S. bill.

In Murphy’s view, removing the currency risk allows him to diversify out of the U.S. bond market and pick up yield without wading into riskier assets. That will be important going forward, he says, as shifting Fed policy and ever-escalating trade tensions between the U.S. and China point to a turbulent stretch ahead in Treasuries. —With Cameron Crise

To contact the editor responsible for this story: Pat Regnier at pregnier3@bloomberg.net, Mark Tannenbaum

©2019 Bloomberg L.P.