Rethinking Currency: Finding a Better Way to Run an Economy

Rethinking Currency: Finding a Better Way to Run an Economy

(Bloomberg Businessweek) -- Money is just so problematic, even apart from its being the root of all evil. It can disappear suddenly: A 2-year-old boy in Utah just put $1,060 of cash through a shredder while his parents weren’t looking. It doesn’t earn its keep: Apple Inc.’s returns are being dragged down by the low yield on $244 billion in cash and marketable securities that it can’t figure out how to spend. And it can seriously malfunction, as it did in last decade’s global financial crisis.

The good news is that money is getting better. Advances in information technology are making possible new kinds of it, notably cryptocurrencies. Meanwhile, the financial crisis has spurred a search for more reliable grades of grease and oil to lubricate the global economic engine. “Computational advances coupled with extraordinary monetary policies have created the perfect petri dish for cryptos and other new forms of money to grow,” says Lawrence Goodman, president of the Center for Financial Stability Inc. in New York.

There are two kinds of money. Government money consists of paper bills and coins plus the reserves that banks have at their nation’s central bank (the Federal Reserve, the Bank of Japan, etc.). In contrast, private money is the stuff that banks and other financial institutions generate when they make loans. This hybrid public-private system works well until there’s a financial crisis, when people suddenly lose faith in private money and the government has to step in—as the Fed did in 2008-09, when it created an alphabet soup of programs to fill in for a banking sector that simply wasn’t providing credit. Some experts want to end this occasionally unstable system by cutting back to only private money; others favor only public money.

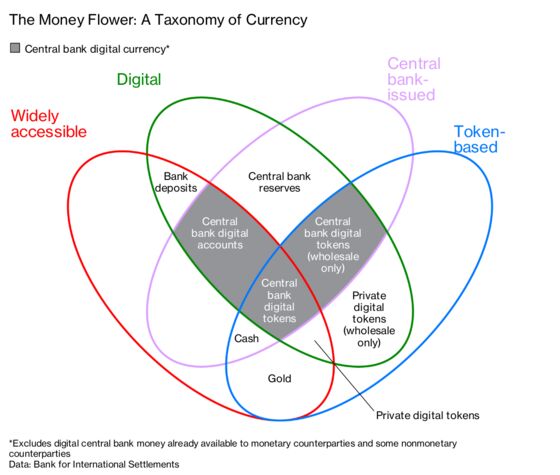

In the graphic that accompanies this article, cash occupies one small corner of the Venn diagram. Cash is in the “widely accessible” oval and the “central bank-issued” oval. It’s also in the “token-based” oval, along with Bitcoin. Token-based means that if you lose your token (the paper bill, or the password in the case of Bitcoin), you lose the money. Your precocious 2-year-old could shred your cash. Or you could be James Howells, the Welsh IT worker who accidentally discarded the hard drive that had his Bitcoin passwords on it. Those lost passwords were worth more than $100 million at one point, but the city council won’t let him dig for the drive in the local landfill.

Bank deposits occupy another corner of the money flower. They’re digital and widely accessible, but they aren’t token-based, and—this is a crucial distinction—the central bank doesn’t issue them. In fact, most money that exists in the U.S. and other advanced economies is privately issued. When a bank makes a loan to a business and credits its checking account with the amount, the sum becomes new money—instantly spendable. Banks can lend out more money than they have in deposits. And the business owner can turn the private money into public money by going to an ATM and withdrawing cash, which is a liability of the Federal Reserve.

A growing share of private money is created outside the banking system entirely, through vehicles such as money-market mutual funds, which invest in the short-term debt of companies on behalf of people who want to earn more on their spare cash than they get from banks on checking accounts. Repo lending is another huge source of private money: Owners of Treasury bonds get short-term loans by temporarily selling the bonds while agreeing to repurchase them soon for a slightly higher price.

Private money would get a big boost from the long-predicted death of cash, which is the only kind of government-issued money that ordinary people can use to make payments. In Sweden, where cash accounts for only 13 percent of payments in stores, the central Sveriges Riksbank is concerned that the extinction of cash would leave private banks in control of “accessibility, technological developments, and pricing of the available payment methods,” as Governor Stefan Ingves wrote in the June issue of the International Monetary Fund’s Finance & Development magazine. “Today, cash has a natural place as the only legal tender,” Ingves wrote. “But in a cashless society, what would legal tender mean?”

Is it possible to have a world with only private money? That’s the vision of some cryptocurrency fans. They hark back to Friedrich Hayek, the Austrian-born economist who in 1984 said, “I don’t believe we shall ever have a good money again before we take the thing out of the hands of government.” For the time being, though, crypto is far too volatile. Bitcoin has lost 65 percent of its value since December.

The opposite approach is to bolster the role of public money. One controversial idea is to let ordinary people effectively deposit money directly at the Federal Reserve, as only commercial banks are permitted to do now. (Imagine a drive-thru ATM window at Fed headquarters.) James McAndrews, who was director of research at the Federal Reserve Bank of New York, is suing his former employer for permission to create an institution called the Narrow Bank, which would do little more than take in deposits from large investors, stash the money at the Fed, and pay the depositors the rate that deposits at the Fed earn, with a bit shaved off the top to make the enterprise profitable. On the money flower, McAndrews’s concept appears in the left gray diamond: digital, central bank-issued, not token-based, and more widely accessible than ordinary central bank reserves.

One concern about giving ordinary people access to Fed deposits is that if it caught on, it would starve commercial banks of deposits, especially in a financial crisis, when depositors seek the safest harbor. That could lead to a world in which all money is government-issued money.

Some nations are already experimenting with what’s sometimes called “reserves for all” and other times called central bank digital currency, or CBDC. Flailing Venezuela is pushing a currency it calls the petro and claims it’s linked to the country’s oil production. A survey by the website Cointelegraph, says Dubai, Iran, Singapore, and Uruguay are experimenting with CBDC; China, the U.K., and other countries are researching the idea; and Ecuador (after a brief trial), Germany, Japan, and Switzerland have rejected it.

Increasing the role of government money might sound like a lefty idea. Indeed, Joseph Stiglitz, the liberal Nobel laureate economist at Columbia, says it would enable the government to limit the ups and downs of the business cycle and even direct credit to certain sectors. But some libertarians and conservatives like the concept for very different reasons. John Cochrane, a conservative libertarian economist at the Hoover Institution, says it would end recurrent financial crises, in which people run away from bank deposits. He envisions digital, government-issued cash that would earn interest. That would solve a problem identified by the conservative icon Milton Friedman, who said people don’t keep enough cash available for emergencies because, unlike their other assets, it doesn’t earn anything. “Our government should take over its natural monopoly position in supplying interest-paying money,” Cochrane wrote in a chapter of a 2014 book, Across the Great Divide.

One person’s money is always another person’s debt. That’s even true of dollar bills: Now that they’re no longer backed by gold or silver, they’re just IOUs that the U.S. government issues. The private money in your checking account is an IOU from your bank. If the IOUs that you hold aren’t reliable, then your money won’t buy anything. The implication is that the key to making money better is “making sure that people who are making promises are doing so with the intention and ability of fulfilling those promises,” says Perry Mehrling, an economist at Boston University’s Pardee School of Global Studies who teaches an online course about money.

All this ferment is a sign that people are taking money and its future seriously. Many economists once viewed money as neutral and unimportant, a mere “veil” over the underlying transactions—so a farmer doesn’t have to use wheat to buy an airplane ticket or pay for haircuts with asparagus. Then came the financial crisis, precipitated by an abrupt loss of faith in assets that had been considered safe enough to be treated as money. “Human history can be written in terms of the search for and production of safe assets,” Yale economist Gary Gorton wrote in 2016. That history is still being written.

To contact the editor responsible for this story: Eric Gelman at egelman3@bloomberg.net, Howard Chua-Eoan

©2018 Bloomberg L.P.