When the Big Get Bigger, Active Stockpickers Feel Even More Pain

When the Big Get Bigger, Active Stockpickers Feel Even More Pain

(Bloomberg Businessweek) -- In a crisis, large companies can have an edge. As the pandemic has forced the shuttering of local stores and restaurants, grounded consumers streamed Tiger King on Netflix, stocked up on groceries and supplies with Amazon, and gathered together on Zoom. Hardly any company is immune from the economic shutdown, but big business has more resources to weather the pandemic and, in some cases, may be able to gain market share.

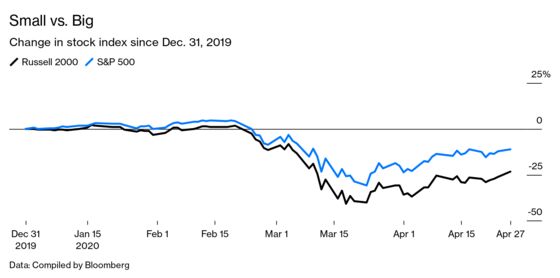

On Wall Street, that’s exacerbating a divergence between small and large companies that’s been frustrating stockpickers for some time. The Russell 2000, a benchmark for small companies, has lagged the big-name S&P 500 index badly over the past two years. This year, the small stocks, with a median market valuation of about $525 million, have lost 23%; the S&P less than half of that. The Nasdaq 100, which tracks the largest tech stocks, is up about 1%. The S&P 500’s companies now make up 82% of the entire U.S. stock market’s value, a percentage that’s been steadily rising this century.

None of that is good news for active fund managers—especially the quantitative investors who create trading rules from computer models. As the big get bigger, a passive index fund that tracks a market-value index such as the S&P 500 gets to surf that wave. Even a portfolio that buys all the S&P stocks but holds them in equal proportion—instead of concentrating in the very largest names as the index does—is trailing the benchmark so far this year, with a decline of around 18%.

The long-term evidence is already stacked against active funds in general: Fewer than a quarter of them have beaten their passive rivals over the last decade, according to Morningstar. During the recent bear market, only about 42% did so.

Quant managers, meanwhile, are naturally pulled toward buying smaller companies. Instead of analyzing a handful of companies in depth to assemble a portfolio, quants sort through data to come up with a few reliable trading signals and apply them across thousands of securities. Since most companies are mid-sized or small, quants can end up underweighted in the blue-chip companies that have lately been thumping the rest of the market.

Los Angeles Capital Management, a money manager that uses quantitative tools, has studied the factors that guide its investing decisions—such as a company’s forecast cash flow growth or momentum in its stock price—and found that applying them reaped higher gains with large companies than with small ones. In other words, the trading models haven’t been working as well with the very stocks quants are more likely to buy. “A lot of the factor efficacy is just in those largest names, whereas historically we used to think the factors apply across the market,” says co-director of research Edward Rackham.

The underperformance of small companies shakes up one of the oldest quantitative investment strategies in the books. A classic study by finance professors Eugene Fama and Kenneth French showed that stocks’ returns could be explained via a variety of factors, including a size effect: Bet on small stocks and against large ones, and you’ll come out ahead. But in the first three months of 2020, that strategy posted its worst period since at least 2002, extending a six-year decline, a Dow Jones index shows.

Michael Hunstad, head of quantitative strategies at Northern Trust Asset Management, says the size factor isn’t dead. Rather, it just has a very long cycle, meaning that it tends to go into and out of favor for years at a time. And not all quantitatively driven strategies are suffering. For example, a hypothetical momentum portfolio—one that buys the past year’s winners—has outperformed through the 2020 sell-off.

Quants would refrain from making any qualitative predictions, but it’s easy to see the pandemic continuing to entrench some advantages of being large. The bashing of Big Tech now looks as dated as a handshake, and Silicon Valley’s giants may be able to expand their clout. Large companies can also find it easier to access credit and solve supply chain problems.

Even so, Gavin Smith, a fund manager at asset management company QMA, says the gap between big and small has become so stretched that small caps should see a recovery. Likewise, Hunstad reckons the mega caps’ ascendancy might not last much longer, given the sky-high expectations now priced into their valuations. That could give quants a break. If a handful of giant companies “have massively inflated growth expectations, and we’re heading into a recession, those are going to be the names to fall the hardest,” Hunstad says.

Read more: Smart CEOs Are Playing Dumb in the Age of Coronavirus

©2020 Bloomberg L.P.