PG&E Shows Utility Stocks Aren’t Boring Anymore

PG&E Shows Utility Stocks Aren’t Boring Anymore

(Bloomberg Businessweek) -- It wasn’t so long ago that investors saw utilities as safe, boring, and modestly profitable. With dependable revenue from monthly electric bills and regular dividends, they were a favorite among penny-saving retirees and portfolio managers wanting to hedge against volatility in the broader market.

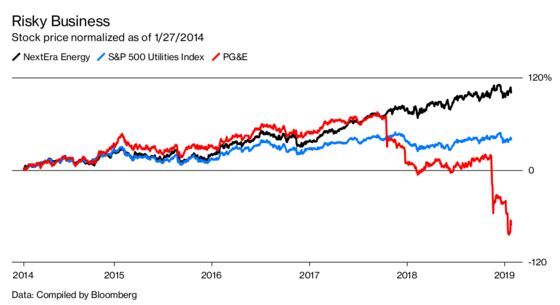

That was then. Things first began to change with the deregulation of the 1990s, but global warming and rooftop solar panels have also been steadily chipping away at the notion that the sector is a safe haven. And now there’s PG&E Corp. California’s largest utility owner plans to file for Chapter 11 as early as Jan. 29 in the face of as much as $30 billion in potential liabilities from wildfires that killed more than 100 people in 2017 and 2018.

“It has absolutely become more complicated to invest in utilities,” says Jan Vrins, head of the energy practice at Navigant Consulting Inc. “The energy transformation is accelerating.” For a start, utilities are having to figure out how to navigate the rise of renewable energy sources. Utilities that invested heavily in giant nuclear and coal plants have found themselves saddled with mounting costs from generating facilities that are struggling to compete against cheap natural gas and wind and solar farms that have seen costs plunge. A wrong bet by a utility can be its undoing. Scana Corp., South Carolina’s largest utility, spent nine years working to expand a nuclear plant before pulling the plug in 2017, when projected costs ballooned to more than $20 billion. Its shares plummeted, and it was acquired by Dominion Energy Inc. this year.

And utilities that embraced solar and wind energy early have benefited, says Jay Rhame, chief executive officer at Reaves Asset Management, which has $2.8 billion under management. Look no further than NextEra Energy Inc., the largest U.S. provider of renewable energy. Its shares have doubled in value since 2014. “A lot of utilities are now trying to get into renewables after seeing NextEra’s success,” says Rhame.

The traditional utility business model is also facing competition from some of its own customers, who are generating their own power by putting solar panels on their roofs. Total U.S. residential power installed is forecast to reach 20 gigawatts next year, according to Bloomberg NEF, more than triple the amount at the end of 2015. (For comparison, a typical nuclear reactor has about 1 gigawatt of capacity.) That, along with energy-efficiency improvements and smarter homes, has sapped many utilities of a traditional source of growth: delivering more power.

Global warming is literally changing the landscape for utilities, with hotter summers making wildfires more common. And in states such as California, where strict liability laws mean power companies can be held responsible for fire damages, that means much more financial risk. PG&E has explicitly blamed its downfall on climate change after the state’s bone-dry hillsides were ravaged by fires in 2017 and 2018. Investigators have cited the company’s equipment as the ignition source of 17 blazes in 2017, though it was cleared last week in that year’s most deadly blaze. PG&E equipment remains under investigation for the 2018 Camp Fire, which killed 86 people.

Still, there’s a climate upside for some utilities. A warmer-than-normal summer last year led to increased air conditioner use, boosting earnings at companies that include Duke Energy Corp., FirstEnergy Corp., and American Electric Power Co. Stronger, more destructive hurricanes have led some power providers to increase spending on transmission lines and grid-hardening technology. Regulators give them a guaranteed return on such investments. It’s a back-to-basics strategy that many investors applaud.

“Infrastructure investment is the key theme here,’’ says Tim Winter, associate portfolio manager for the Gabelli Utilities Fund. “Utilities in general, they are as safe if not safer than they’ve ever been.” Low natural gas prices have helped keep fuel costs down, allowing utilities to avoid hitting customers with big rate increases. Winter sees the sector posting average annual earnings growth of 5 percent to 6 percent through 2021, compared with the 3 percent to 4 percent utilities have typically earned in the past.

The safest utility investments are those that own only own poles and wires, not power plants, says Michael Weinstein, a utility analyst at Credit Suisse Group AG. In the 1990s, regulators in some states made generating power and delivering it to customers into separate businesses. Companies that had long enjoyed monopolies now had to compete for revenue. Many utilities got burned in the process, making them seem risky for traditional investors. Weinstein says companies that have stuck to running the power grids still benefit from predictable returns. “A lot of investors want the pure-play utility,” he says. “The less complicated the better.”

To contact the editor responsible for this story: Joe Ryan at jryan173@bloomberg.net, Will WadePat Regnier

©2019 Bloomberg L.P.