Masayoshi Son, SoftBank, and the $100 Billion Blitz on Sand Hill Road

Son says he’ll raise a new $100 billion fund every few years. Silicon Valley’s disruptors are struggling to keep up.

(Bloomberg Businessweek) -- Two years ago, Masayoshi Son, chief executive officer of SoftBank, sat in a Gulfstream jet high above the Arabian Gulf, en route to meet with potential investors in a new fund that would invest in technology startups. He was going through his presentation with Rajeev Misra, a key lieutenant, when something stopped him.

One of the slides included the proposed size of the fund: $30 billion. The figure would make the Vision Fund, as Son had named it, about four times the size of the largest venture capital fund ever created and bigger than any private equity fund in history.

Son stared at the number for a moment. Then he deleted the three and replaced it with a one and another zero. “Life’s too short to think small,” he told a stunned Misra.

When Son came to the $100 billion slide in his presentation a few hours later, the prospective investors—executives from a state-owned fund in the Middle East—laughed. Son didn’t, continuing his presentation as if nothing had happened. “He didn’t miss a beat,” recalls Misra, now the fund’s CEO.

SoftBank’s Vision Fund would gather almost $100 billion, including $45 billion from Saudi Arabia’s Public Investment Fund, as well as capital from Apple Inc., the government of Abu Dhabi, and others. “One hundred was a simpler number,” Son says during a September interview at the Tokyo headquarters of SoftBank Group Corp., a sprawling conglomerate that includes an enormous Japanese mobile phone carrier (also called SoftBank), a leading chipmaker (Arm Holdings Plc), and a majority stake in Sprint Corp., the U.S. wireless carrier.

As an investor, Son has been prescient. He was one of the earliest backers of Yahoo! and then teamed up with the dot-com-era darling to launch Yahoo! Japan, a property that wound up being much more valuable than its parent. In 2000 he put about $20 million into Alibaba Group Holding Inc. That stake is now worth roughly $120 billion.

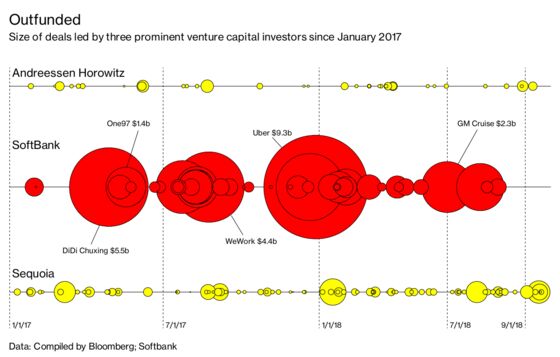

But the Vision Fund is something new: An all-out blitz on the heart of Silicon Valley venture capital, Sand Hill Road. In less than a year since the fund first began making investments, it has already committed $65 billion to acquire big stakes in Uber, WeWork, Slack, and GM Cruise. Son tells Bloomberg Businessweek that he plans to raise a new $100 billion fund every two or three years and will spend around $50 billion a year. For perspective, in 2016, the entire U.S. venture capital industry invested $75.3 billion, according to the National Venture Capital Association.

Son’s audaciously large bets have astonished and confused Silicon Valley, where even the most respected venture capitalists have found themselves outmaneuvered by a relative newcomer. The standard VC playbook involves making small, speculative investments in early-stage startups and adding funds in follow-on rounds as those startups grow. SoftBank’s strategy has been to put enormous sums—its smallest deals are $100 million or so, its biggest are in the billions—into the most successful tech startups in a given category. If the local VCs are freaked out by this, the startups seem to love it. SoftBank has given them the equivalent of an all-you-can-eat buffet of foreign investment dollars. “You think they can’t eat anymore,” says Jules Maltz, a partner with IVP, a Sand Hill Road firm. The entrepreneurs “cram it in, put it in their pockets, take doggy bags, whatever.”

The tech industry has seen deep-pocketed outsiders before, but SoftBank is operating at a scale never attempted. That’s driven valuations up, making it difficult for traditional firms to put together enough capital to get into the hottest deals. SoftBank, according to a partner at a major Silicon Valley firm, is “a big stack bully,” a poker term referring to a player with a pile of chips so huge that competitors are afraid to get in the game.

The situation has sent firms scrambling to adapt. Sequoia Capital is raising funds worth $12 billion to stay competitive when bidding on big, late-stage deals. That’s up from about $1.7 billion during a similar period five years ago. Sequoia’s longtime rival, Kleiner Perkins Caufield & Byers, has gone in the other direction, announcing in mid-September that it was breaking up. Four partners, including one of the firm’s stars, Mary Meeker, are leaving Kleiner to start a firm focusing on big bets. The remaining partners will concentrate on earlier, smaller deals. Kleiner’s Ted Schlein has attributed the split in part to a massive amount of capital being invested in startups. He didn’t mention SoftBank by name, but there was little doubt which big stack bully he had in mind.

To most people outside the venture capital industry, Son’s reputation stems less from his big thinking and more from his big spending. In late 2012, shortly after SoftBank announced plans to buy a majority stake in Sprint, Son paid $117.5 million for an enormous Italianate mansion in Woodside, Calif. At the time, it was the most expensive home purchase in U.S. history.

Son says he bought the estate because he doesn’t like hotels and needed a comfortable place to stay when he comes to Silicon Valley. And then, as if to prove that a man with a $117.5 million crash pad can still be a man of the people, he tugs at his gray wool sweater. “I always wear Uniqlo,” he says, referring to the low-cost retailer whose founder sits on SoftBank’s board. Then he lifts his pants leg to show off a stitched brown loafer. “This is a $50 shoe,” he says. Next he pulls at his shirt collar. “This is also Uniqlo. It’s fantastic!”

Son’s upbringing was, in fact, modest. He grew up on the southern Japanese island of Kyushu and was bullied as a child, because his family had come from Korea. Son’s father supported the family through an endless series of ventures that included selling bootleg liquor, raising pigs, and running pachinko parlors. The family adopted a Japanese surname, Yasumoto—a common decision in a country where foreigners face discrimination—but when Son returned to Japan after studying economics at the University of California at Berkeley, he started using his Korean name. “He didn’t want to hide from who he was,” says Hong Lu, Son’s first business partner.

Son founded SoftBank in 1981 as a distributor of PC software. That led to investments in Ziff Davis LLC, the computer trade publisher, and Comdex, the now-defunct trade show in Las Vegas. In 1995, Son wrote a $2 million check during his first meeting with Yahoo co-founder Jerry Yang. He came back a month later offering a $100 million investment, far more than Yang was willing to accept at first. The shock-and-awe offer would become Son’s go-to move.

By 2000, Son had made hundreds of investments and had briefly become the world’s richest man. But then the dot-com bubble burst, and SoftBank lost 93 percent of its market value. A widely reported but apocryphal story says that Son lost $70 billion from his net worth in a single day. In reality it took a little over a year. (He’s now worth $18 billion, according to a Bloomberg analysis.)

Son never stopped making deals. Lu says that Son seemed to be fighting for his life and spent most nights in his office during his post-dot-com scramble. “I thought he was going insane,” Lu says. “He would have meetings at midnight, 3 a.m.” In 2006, Son struck a deal to buy Vodafone Japan and then landed an exclusive deal to distribute the iPhone, which turned around the struggling carrier.

By 2010, Son seemed to be settling into middle age as an opportunistic dealmaker. But he surprised investors that year with a two-hour speech at a shareholders meeting that attempted to articulate a plan for the next 300 years. The rambling 133-slide presentation was chock-full of stock photos and touched on everything from the role of technology in fixing human suffering to why companies fail. Son finally wrapped up by saying he was creating a “strategic synergy group”—an extended family of companies, in which SoftBank would buy stakes of from 20 percent to 40 percent. The companies would have a common mission: “Information revolution—happiness for everyone,” as he put it. Opinion was divided on whether the presentation was an inspiring display of Son’s brilliance, or an amusing demonstration of his kookiness.

The Vision Fund is now run by nine managing partners—five at the fund’s Silicon Valley outpost, two in Japan, and two in London. Son says he personally trained these “hunters” on how to find the best investments and plans to increase the number of dealmakers to 300 over the next few years.

Managing partners filter potential investment ideas and hold a weekly call to discuss progress. Once the prospects are vetted, they go to the investment committee, which is made up of Son, Misra, and a third SoftBank executive, Saleh Romeih. In June, Son said he’d spent 97 percent of his time on SoftBank operations. In his interview with Businessweek, he says that figure is down to 3 percent, with the vast majority of his time spent on dealmaking.

Despite a reputation for throwing money around, Son isn’t an easy mark, his partners say. “If it was a rubber stamp, that would be a lot easier,” says managing partner Jeff Housenbold, former CEO of Shutterfly. “You have to get through the intellectual rigor of convincing him that this is a deal we should do.”

Decisions can take months. When SoftBank began exploring an investment in Uber Technologies Inc. in 2017, the ride-hailing startup was in a state of turmoil, having been the subject of allegations of sexual harassment and other assorted ethical failings. The board had stripped the by-then notorious Travis Kalanick of his CEO duties, and an early investor was suing to kick him off Uber’s board.

Son and Misra faced resistance from Uber, as well as from businesses in their portfolio, which include ride-sharing companies Didi Chuxing in China, Ola Cabs in India, and Grab in Singapore. “We had to persuade people in a big way,” says Misra, who was a senior executive at Deutsche Bank AG and UBS Group AG before joining SoftBank in 2014. He argued that it made more sense to have Uber “in the family rather than not.” SoftBank ultimately invested $7.7 billion in Uber, its biggest single bet to date. The stake is now worth around $11 billion.

Has the SoftBank CEO personally ever taken an Uber? “Yeah,” Son says. “We ordered with my assistant in a European country. I forget which. London, maybe. It was a fantastic service.”

In describing the vision behind the Vision Fund, Son sometimes uses the term gun-senryaku, a Japanese expression that describes the way a flock of birds flies together. His hope, he says, is that portfolio companies will help one another and head off copycats. In Southeast Asia, for instance, SoftBank has encouraged Grab to form joint ventures with a handful of portfolio companies to help those startups break into the region. Grab CEO Anthony Tan is in charge of the effort. Son says similar partnerships are in the works around the world. “You don’t want to go into every little country and try to fight,” Son says, addressing prospective competitors. “You should go there and partner with Grab and the Vision Fund will invest.”

Another portfolio company, Plenty Inc., an indoor farming startup, has been in discussions on a possible collaboration with Katerra Inc., a startup also backed by the Vision Fund that’s working with new technologies to make building construction more efficient, according to Matt Barnard, Plenty’s CEO. Meanwhile, Vision Fund-backed Mapbox has joined with Arm, SoftBank’s U.K.-based chip company, to bring its machine learning software to the billions of devices that use Arm chips, including smartphones and cars.

Entrepreneurs who have taken money from Son cite numerous examples of SoftBank providing help with international expansion. SoftBank’s giant checks also force other VCs to think carefully before funding startups that intend to compete with companies in its portfolio. “We’re seeing more and more cases where the No. 1 company in a particular market is not just a little bit bigger, but actually orders of magnitude bigger, and the Vision Fund is investing in those companies specifically,” says Stewart Butterfield, CEO of Slack Technologies Inc. Butterfield’s company raised $250 million in a round led by the Vision Fund at the end of last year at a valuation of more than $5 billion. Slack, like so many Vision Fund companies, is much larger than its closest competitors. “This is not like established industries—say, automotive—where you had three to four large players, all more or less of similar size and competing at the same level,” Butterfield says.

SoftBank’s success in pushing fast-growing startups into a dominant position gives Son an advantage when negotiating for a stake in a company. He hasn’t been shy in pressing that advantage. In 2015, online lending startup Social Finance Inc. was looking to raise a few hundred million dollars, but Son wanted to invest more. According to SoFi co-founder Mike Cagney, Son told him that he was going to invest $1 billion in online lending—whether that capital went to SoFi or its competitors was up to Cagney. The entrepreneur opted to take the deal.

Son dismisses complaints from VCs that these tactics are overly aggressive. “They can say whatever they want,” he says. He adds that he has respect for the traditional venture capital business. “I just want to do it my way.”

Hardball tactics aside, others have raised questions about whether SoftBank’s megadeals will be profitable for Son or his backers in the long run. The Vision Fund’s war chest includes about $40 billion in debt, an unusually risky structure for a venture capital firm. Investors have contributed a mix of capital in the form of equity and debt at a 7 percent interest rate. This reduces risk to investors, but it means that SoftBank, which contributed $28 billion in equity, is taking on more risk.

To show a 20 percent internal rate of return on its own capital—which would be a solid return for a VC—SoftBank would need to produce lots of startups with a $10 billion market capitalization and at least two with market caps of over $100 billion, according to research published by EquityZen Inc., a platform for trading stock in privately held companies. That’s a tall order, but Son says delivering high returns should be no problem. He claims that since 2000 his investments—including Yahoo, Alibaba, Vodafone Japan, and the gaming company Supercell Oy—have returned 44 percent annually. For now, investors have bought into his pitch. In late September, SoftBank shares hit their highest level since March 2000, the start of the dot-com crash.

There’s also the question of succession. At one time, Son’s heir apparent was former Google executive Nikesh Arora, but he left two years ago, in part because he worried Son wasn’t going to leave anytime soon. At the time, Son announced that he planned to stay on as CEO of SoftBank for 5 to 10 more years. He compares succession to a relay race, adding that he hopes to turn over the baton to someone who can handle his pace.

“The best batoning is that the guy is running without slowing down, maybe even accelerating at the end,” he says. “And the new guy: rocket start.”

So who’s the new guy? “I don’t know,” says Son. “I will identify within the next eight years.” —With Pavel Alpeyev

To contact the editor responsible for this story: Max Chafkin at mchafkin@bloomberg.net

©2018 Bloomberg L.P.