Markets Were Already Braced for Chaos—and Then Came the Diagnosis

Markets Were Already Braced for Chaos — and Then Came the Diagnosis

(Bloomberg Businessweek) -- The news that President Donald Trump and his wife, Melania, have contracted Covid-19 brings a dizzying array of possibilities for the nation—and the financial markets.

It’s the type of uncertainty-inducing event that can act like a gut punch. But in this case, many stock investors were already in a defensive crouch. In options and futures, demand for hedges to protect against sudden bouts of volatility has been strong. Traders say that’s in case Trump refuses to accept a loss in November, a prospect he reinforced in Tuesday night’s debate.

While those hedges may have softened the impact of the news, and stocks recouped much of their early losses on Friday, they still signal a high level of anxiety about what could shape up to be a constitutional crisis between Election Day and Inauguration Day. “The Covid-19 election is a unicorn,” says Michael Arone, chief investment strategist for the U.S. SPDR exchange-traded fund business at State Street Global Advisors. “The range of outcomes has gotten a lot wider,” and the odds of low probability events whipsawing the markets has grown, he says.

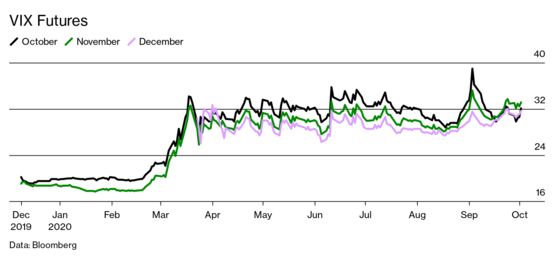

That anxiety is most easily observable in VIX futures, a way to bet on volatility. They tend to serve as a sort of insurance policy against losses in the S&P 500. Hedging activity against outsize swings near the election has been visible all year in these contracts. While that’s not too unusual, it’s clear that as November approaches, concern is elevated for the entire period from the Nov. 3 election to the inauguration in January.

Normally, prices of VIX contracts rise as they cover dates further into the future. When plotted on a graph, this produces a gently rising curve. There’s a simple logic to explain why: If you’re buying insurance on your house, you would expect to pay more for a policy that covers you for six months than for one that covers you for only one month.

Yet these aren’t normal times. Now, the VIX curve has been signaling something else: Investors are increasingly skittish about the 2 ½ months from the election to inauguration, so they’re paying up protect themselves during that period. November futures, designed to protect against expected volatility through late December, are the most expensive.

Dig a little deeper into the numbers, and you see even more signs of worry. The VIX and its futures are based on option contracts on the S&P 500 that investors use to bet on the direction of the index in the following month. Their value is expressed in what’s known as implied volatility, or the size of expected price swings that trading in the options is reflecting. Put options that protect against a 10% drop in the S&P 500 over the next three months traded with an implied volatility of 32.2 as of Sept. 30. That’s relatively high. It compares with a reading of about 20 at around the same time before the prior two elections, and approaches the 35 seen in 2008, when the election was overshadowed by the global financial crisis.

“I’ve been describing these things as well-known risks,” State Street’s Arone says of the threat of a contested election. “Nonetheless, I think that the market will continue to have these kind of bouts of volatility.” He sees continued demand for haven assets such as Treasuries, gold, and the yen until the outcome is settled.

For many investors, though, Trump’s diagnosis was a bit of game changer, one way or another. Hedge fund EIA Alpha Partners LLC, for example, unwound some trades made to protect against market swings due to a contested election, according to the firm’s chief macro strategist Naufal Sanaullah. “The one-two punch of debate, plus Covid diagnosis, makes that risk lower,” he says, pointing to the fundraising boost the Democrats got following Tuesday’s debate.

Many analysts also believe it could finally prod Congress to agree on an additional stimulus package. Still others say it could also renew concerns about the virus that could hamper reopenings and further damage the economy.

“This makes the chance of a second wave look more credible,” says Yousef Abbasi, global market strategist at StoneX. “If you go with that argument, how could you not see the need for more stimulus?”

How Trump’s illness sways the election is also something of a wild card. While it’s possible it could induce sympathy from some voters, many believe the election will be a sort of referendum on how well he handled the pandemic. Contracting the disease himself doesn’t exactly bolster his argument that he did a great job leading a nation, with nearly 210,000 deaths and counting.

That line of thinking boils many investment decisions down the question of who would be better for the stock market: the tax-cutting, regulation-shredding Trump or Joe Biden, who wants to raise the corporate tax rate to 28%, from 21%, and has been more cautious about reopening the economy while the pandemic still rages?

To James McDonald, chief executive officer of Hercules Investments, the prospect of higher taxes and other elements of Biden’s platform may cause institutional investors to start moving out of riskier assets and hedging against more volatility.

Others, such as EIA Alpha’s Sanaullah, believe a Biden win and a Democratic sweep of both houses of Congress would be the most bullish outcome because it would produce the largest stimulus bill.

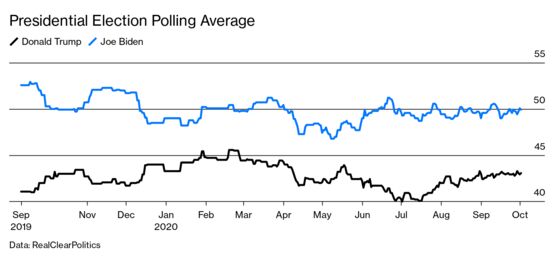

With Biden leading most polls, the market may continue to price in a more resounding victory by the Democrat, which would lessen the chance of a contested election and, by extension, the risk of further market eruptions, according to Christopher Smart, global chief strategist and head of the Barings Institute. “Having said that, we are in truly uncharted territory,” he says. “And if a week is a lifetime in politics, we have at least five lifetimes between now and Election Day.”

Read next: Will Trump’s Illness Slow the Economy’s Rebound?

©2020 Bloomberg L.P.