Japan’s Post Office Is an Unlikely Global Bond Powerhouse

Japan’s Post Office Is an Unlikely Global Bond Powerhouse

(Bloomberg Businessweek) -- The long era of superlow interest rates has reshaped the financial world in some surprising ways. For example, who comes to mind when you think of major players in the global fixed-income market? There are the giant Pimco, BlackRock, and Vanguard funds, of course. But how about Japan’s post office?

Strictly speaking, we’re talking about Japan Post Bank Co., the banking unit of Japan Post Holdings Co., a publicly traded company majority-owned by the government. The postal bank held $577 billion worth of bonds outside its home market in March. That’s more than the investment-grade portfolio at Fidelity Investments or the fixed-income holdings at Britain’s Standard Life Aberdeen Plc. And it’s a big change from a decade ago, when the foreign bond portfolio at Japan Post Bank was negligible.

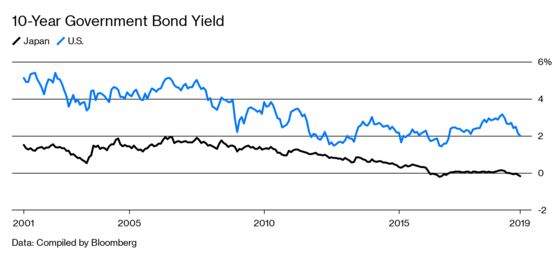

This new whale on the global bond market hasn’t arrived willingly. Low rates have effectively pushed Japan Post out of the country’s government bond market. Long-term yields in Japan are around 0%, far below even the exceptionally slim rates in the U.S. This has upended a business model at the postal bank that lasted for more than a century.

Japan’s postal system set up savings accounts in 1875, growing to become at one point the world’s largest deposit-taking institution. Largely barred from making loans like those of a normal commercial bank, the banking unit plowed those deposits into government bonds. And when yields were well north of 1%, that made for a boring, yet profitable, enterprise. The postal bank now has some $1.7 trillion of deposits, the savings of millions of Japanese households in big cities and remote villages, to invest. But Japan’s bond yields are too low to cover the cost of servicing the bank’s funds, a cost that S&P Global Ratings estimates at 0.57%.

“It’s a road to insolvency” for the postal bank to invest in Japanese government bonds now, says David Threadgold, a Keefe, Bruyette & Woods analyst in Tokyo who’s followed banks there for more than three decades. And with no other domestic asset class big enough to pour deposits into other than equities, which would require the bank to keep higher capital reserves, “they have to turn themselves into an overseas investment vehicle,” he says.

Many of the bank’s investments are boring enough: Instead of buying supersafe Japanese government bonds paying essentially nothing, it buys supersafe U.S. Treasuries yielding about 2%. That should be enough to leave it comfortably in the black. The main risk is currency fluctuation. Investors can hedge that risk, but the cost of doing so has climbed.

So the postal bank has been on the hunt for new kinds of assets. With some $539 billion of domestic government bonds still on the books and set to mature over time, and deposits continuing to grow, that’s no simple task. It aims to direct some funds to private equity and real estate. It’s also gone into credit investments, including U.S. collateralized loan obligations—which bundle together loans made to riskier companies. It isn’t the only Japanese savings institution diving into CLOs in search of better yield. Norinchukin Bank, a cooperative that invests the deposits of millions of Japanese farmers and fishermen, is too. Norinchukin bought $10 billion of CLOs in the U.S. and Europe in the last three months of 2018, accounting for almost half of the top-rated issuance for the period, according to estimates compiled by Bloomberg.

While observers are confident Japan Post doesn’t have major time bombs on its balance sheet, the record of Japanese investment overseas is replete with missteps. In March, Japan’s No. 3 bank, Mizuho Financial Group Inc., surprised investors by booking 150 billion yen ($1.4 billion) of losses on its foreign bond holdings. And Norinchukin posted a $6 billion loss during the financial crisis because of its purchases of toxic assets in the U.S. “You are asking if we are comfortable with this? I don’t think everything is fine. There are risks,” Japan Post Holdings Chief Executive Officer Masatsugu Nagato said about the need to invest abroad at a June press briefing. He also said: “We are very careful, but foreign bond investment will increase.”

Japan’s financial regulators say they are keeping an eye on lenders’ investments in CLOs and other loans, so the postal bank’s freedom to pile into particularly risky assets may be limited. Even so, another risk is on the horizon: What if U.S. Treasury yields fall? “The scary thing really is that they are all depending on the U.S. market,” Michael Makdad, a Morningstar Inc. analyst in Tokyo, says of Japan Post Bank and its peers.

Ten-year Treasury yields have tumbled by more than a percentage point over the past nine months, as investors have bought up government debt expecting central banks to become even more dovish as economic growth slows. With the Federal Reserve forecast to lower interest rates, some bond strategists see yields going well below 2%. The euro region hardly offers a better option, with much of the area’s debt trading with negative yields. “If you turn the rest of the world into Japan, then there’s no escape,” Threadgold says.

One option could be to wind down the balance sheet and make the postal bank smaller. But Japan Post is sometimes the only provider of financial services in areas where the population is shrinking. And the banking unit subsidizes the postal business. The idea of turning customers away or discouraging deposits by adding fees is difficult for any national policymaker to embrace. Japan Post Bank is “a national brand,” says Rie Nishihara, a senior analyst at JPMorgan Chase & Co. in Tokyo. “They face a more challenging yield cycle and credit challenges, and that’s very difficult while also supporting 24,000 branches” across the postal system, she says. So the fortunes of this mammoth institution may rely on the U.S. avoiding the same low-rates-forever dynamic that has driven the bank overseas. —With Russell Ward and Taiga Uranaka

To contact the editor responsible for this story: Pat Regnier at pregnier3@bloomberg.net

©2019 Bloomberg L.P.